Accountants probably remember that once the balance gave up once a quarter. Now take it to the FTS only at the end of the year. In the article, we will tell what time it is to take the shape of the balance, how to fill out the partitions of the reporting form.

Who gives shape number 1

Balance must take all companies. Small enterprises have the right to hand over annual accounting statements on simplified forms (PP. "A" of paragraph 6 of the Order of the Ministry of Finance of Russia dated 02.07.2010 No. 66N).

Many accountants call the balance of form No. 1, but actually the balance is the form of OKUD No. 071000.

Download Accounting Blanc (Form 1)

Where to pass and what time

The first thing annual balance must be submitted to the FTS.

Be sure to one copy of the balance accounting reporting It is necessary to send to the territorial authority of statistics (Art. 18 Federal Law from 06.12.2011 No. 402-ФЗ).

Also the balance can request suppliers or founders to evaluate the financial position of the firm.

Deadline accounting balance For 2018. - Until April 1, inclusive 2019 (the time is shifted due to the weekend).

How to make accounting balance

Asset and passive are components of the balance.

The asset includes two sections: current assets (debt of debtors, money in accounts, etc.) and fixed assets (NMA, fixed assets, deferred tax assets, etc.).

Passive consists of three sections:

- Capital and reserves.

- Short-term liabilities.

- Long term duties.

The balance of the balance informs about all the property of the company, and the Passion will tell about the sources of the receipt of this property. Equality must be respected: asset \u003d passive.

The balance contains information at the end of the year. It also indicates information on all indicators at the end of the previous two years. So, in the balance for 2018, accountants will also indicate the data for the years 2017 and 2016.

All balance indicators are combined into articles. Each line of balance has its own code. Small businesses can be a brief balance, but other companies give detailed decoding of all articles. As far as in detail the information in the balance sheet, the organization determines itself, relying on the level of materiality level of one or another (note number 2 to the balance sheet indicated in the order of the Ministry of Finance of Russia of 02.07.2010 No. 66n). Information about materialization levels is usually prescribed in accounting policies.

When conducting accounting, the economic entity should be on certain dates mandatory forms reporting. Their number includes balance sheet. Many state and regulatory authorities consider it one of the main documents. Therefore, the accountant should know exactly how to fill the balance sheet, which accounts where to attribute.

The balance sheet is one of the forms that are included in the accounting package. According to the law, any legal entity, no matter what the organizational form and the selected tax regime he has, should fill these reports and send them to the tax and statistical authorities.

Also, such a responsibility is assigned to non-commercial structures and advocate colleges.

Balance and profit and loss statement are established as optional only for entrepreneurs, as well as open in Russia units foreign companies. But make out and transmit these forms on own initiative The law does not prohibit them.

Attention! In the previous year, the law allowed some business entities to make reporting. However, now these reliefs are canceled. If the subject is assigned to the category of small enterprises, the reporting should still be drawn up, just to do this in a simplified form. At the same time, the balance in this case is still mandatory, and it is still necessary to apply it to the controlling bodies.

Terms of delivery of the balance

The rules established that the accounting balance form 1 must be sent in the total reporting package for the previous year until March 31 of that year, which follows.

At the same time, this period is mandatory for execution both when transferring a balance to the tax service and statistics.

Under some conditions, together with accounting reporting, the statistics need to convey the audit report. It must be done on a period of 10 days, but no later than December 31, which is coming for the reporting.

For some organizations, due to the type of activity, either by other criteria, is imposed not only to execute and submit reports to government agencies, but also to publish it. For example, firms that perform the role of tour operators must provide in Rostrud documents for 3 months after the statement approval.

Attention! The law also defines certain deadlines for submission of reports for organizations that have been registered after September 30. Due to the fact that the calendar year in such companies will be considered in different, the first time to apply reporting they will be required until March 31 of the second subsequent after registration of the year.

For example, LLC "Empire" was submitted to the register on October 20, 2017. The first time the company will need to prepare a package of accounting until March 31, 2019.

As a rule, the balance is issued on the basis of the company's work for the year. However, it is allowed to make it not only every quarter, but also, for example, monthly. In this case, these documents will be called intermediate. This kind of documentation is usually necessary banking organizations When evaluating solvency, owners of the company, etc.

Where is provided

The legislation determines that the balance form 1 and form 2 of the profit and loss statement, as well as other mandatory forms included in the accounting reporting, must be filed:

- Tax Service - Documents Rent at the place of registration of the company. If the company has separate units or branches, then, at the place of their location, reports are not submitted, and only the parent company gives general summary statements. Make it is also necessary at the address of its registration.

- Statistics - Currently, the provision of accounting reporting in Rosstat is strictly mandatory. If this is not done on time, then on the organization responsible and officials Penalties will be imposed.

- Owners, founders are necessary because any annual report must first be approved by them.

- Other regulatory authorities, if the provisions of the legislation establish the obligation of this step.

Attention! There are also organizations that may be asked to provide them with reports to perform any action. For example, banking institutions when considering an application for a loan on the balance sheet assesses the solvency of the company.

Some large companiesWhen concluding contracts for the supply or provision of services, asked to provide their future partners Form 1 Balance form 2 Profit and Loss Statement. However, this is done at the discretion of the administration.

On the other hand, a large number of services provide the ability to check organizations and entrepreneurs in the Coda of Inn or OGRN. All information is selected from the reports filed earlier.

Methods providing

The form on OKD 0710001 can be sent to government agencies in the following ways:

- Personally in the hands of an employee of the FTS or statistics;

- With the help of a valuable postage - a letter must be attached to an inventory, it should also have a monetary value;

- With the help of the Internet - the company should be issued by the EDS, and the data transfer agreement with any special operator has been concluded. You can also submit a report directly through the tax site, but for this will also be required. The report must be defined electronically if the company operates from 100 people and above.

Accounting Balance Blank 2018 free download

Download for free in Word format.

2018 Download for free in Excel format (without string codes).

2018 Download for free with lines in Excel format.

For 2018, download in PDF format.

How to fill out an accounting balance in form 1

Title

Filling is performed according to the following scheme. After the name of the document is affixed by the date on which the data is made. On the right in the table you need to specify the actual date of filling. This is produced in the column "Date (number, month, year)".

Following the full name of the organization, and then in the table - it is. Below here in the table it is necessary to put the Inn firms.

Following the full name of the organization, and then in the table - it is. Below here in the table it is necessary to put the Inn firms.

Then you need to put the name of the organizational form, as well as the form of property. The table needs to enter the corresponding codes. For example, if this is a llc - then you need to put the code 65. Private property Corresponds to 16.

In the next graph, you must select in which units are entered money sums Balance - in thousands or millions of rubles. Here in the table you need to enter the window code. The last line is intended to record the address of the organization.

Assets

Fixed assets

In p. 1110 "Intangible assets" reflects the balance of account 04 In addition to works on R & D minus account balance 05.

In p. 1110 "Intangible assets" reflects the balance of account 04 In addition to works on R & D minus account balance 05.

In p. 1120 "Research results" reflects the balance of subaccounts of account 04, where the works of R & D are taken into account.

In p. 1130 "Intangible search queries" reflects the balance of the account 08 by subaccount material expenses on search work.

In page.1140 "Material search queries" reflects the balance of the account 08 on the subaccount of material expenses for search work.

In p. 1150 "Fixed assets" reflects the balance of account 01, reduced to the account balance 02.

In p. 1160 " Profitable investments In the MC "reflects the balance of account 03, reduced to the balance of account 02, subaccount, relating to the depreciation of assets attributable to revenue investments.

In p. 1170 "Financial investments" reflects the balance of account 58, reduced to the balance of the account 59, as well as the balance of 73, reflecting interest loans for more than 12 months.

In p. 1180 "Deferred Tax Assets" reflects the balance of the account 09. It is allowed to reduce the balance of account 77.

In p. 1190 "Other non-current assets" can be shown any other indicators that refer to this section, but cannot be attributed to any of the specified lines.

Attention!In p. 1100 you need to sum up and record the result in the section, namely lines from 1110 to 1190.

Current assets

This section reflects information on short-term assets of the enterprise.

This section reflects information on short-term assets of the enterprise.

Page 1210 "Reserves" contains a final indicator of folding from:

- The rest of the debit of sch. 10, from which it is necessary to deduct the value of the account balance. 14, add the balance of sch. 15 adjusted for sch. sixteen.

- Debit balances on accounting accounts 20, 21, 23, 29, 44, 46, which reflect the amounts of unfinished products.

- The rest of the debit of sch. 41 (minus sch. 42) and sch. 43, which shows the cost of goods and finished products.

- Saldo in sch. 45, reflecting shipped products to customers.

P. 1220 "VAT" includes the balance of the SC. 19, which reflects the amount of VAT on acquired material values, works and services.

In art. 1230 " Receivables»Reflects information on the following accounts:

- Remains on the debit of accounts 62, 76, which reflect the short-term receivables of buyers, taking into account the account indicator. 63 "Reserves for long-term debts"

- The rest of the debit of sch. 60, 76, which fixes the sums of sent advances to suppliers.

- Debit residue by subaccount account. 76 "Insurance calculations."

- Balance. 73, which reflects the debt of the company's personnel, except for the amounts of loans for which loans are accrued.

- Part of the balance of sch. 58 "Provided loans", taking into account loans for which interest is not accrued.

- The rest of the debit of sch. 68 and 69, which reflects overpayment for mandatory payments to the budget.

- Debit balance on sch. 71. Which reflects the calculations on the report.

- Saldo in sch. 75, which takes into account the inclined contribution to the share capital.

P. 1240 "Financial Investments" is designed to reflect in it:

- Saldo in sch. 58 adjusted for the balance of sch. 59.

- Saldo in sch. 55 "Deposits"

- Saldo by subaccount sch. 73 "Loan calculations", in terms of loans for which interest is made.

P. 1250 Reflects the final value on all accounts on which the company's money is taken into account. 50, p. 51, sch. 52, sch. 55, sch. 57.

In p. 1260 "Other revolving assets" balances on accounts that are part of the property, but were not reflected in the above lines.

In p. 1200 of this report, you need to add and reflect the amount of all values \u200b\u200bof the indicators of section II C p. 1210 to 1270.

Attention!P. 1600 "Balance" reflects the balance of the balance, which is determined by addition the values \u200b\u200bof the final strings of the asset partitions: p. 11300, p. 1200.

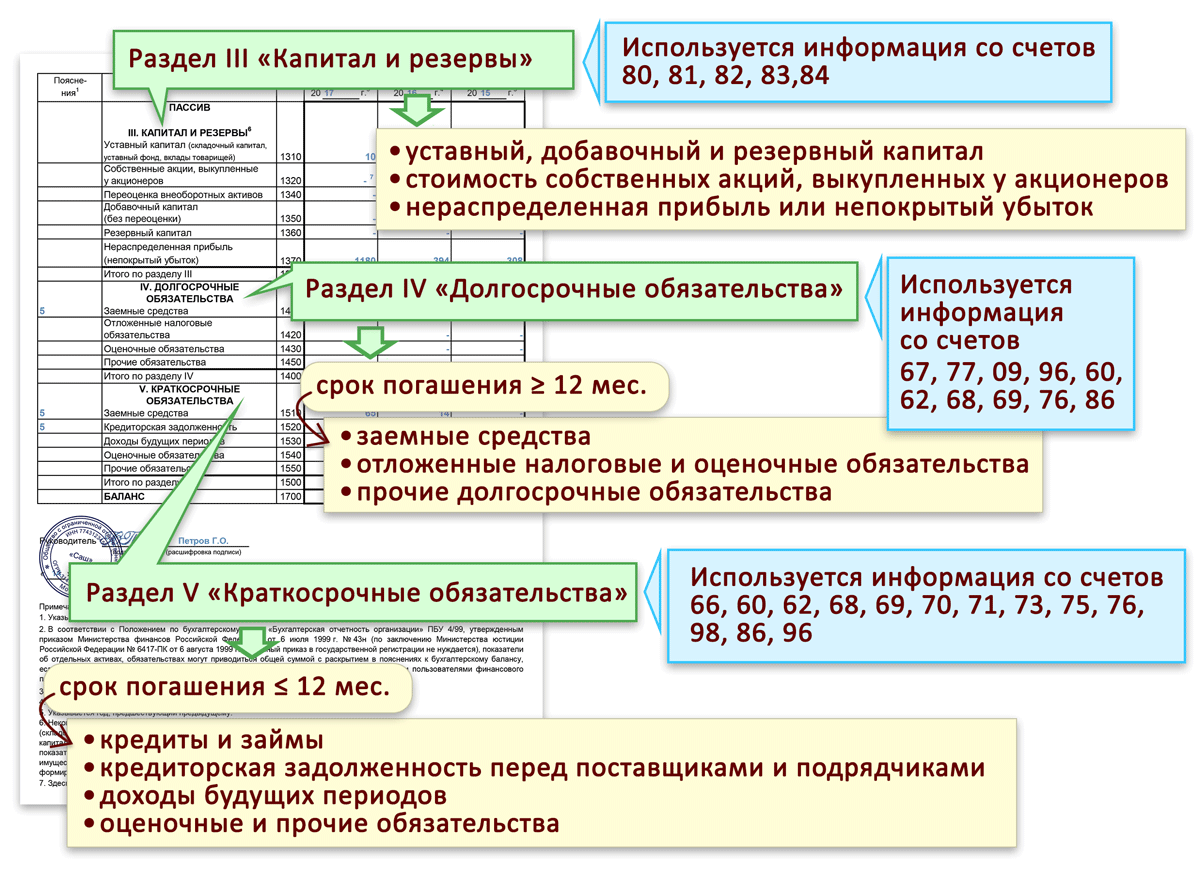

Passive

Capital and reserves

In p. 1310 " Authorized capital»The company's capital will be recorded, which is indicated in the registration documents of the business entity. It reflects on the loan. 80.

In p. 1310 " Authorized capital»The company's capital will be recorded, which is indicated in the registration documents of the business entity. It reflects on the loan. 80.

In p. 1320 "Own shares" indicate the balances on the loan. 81, which reflects information about the repurchased promotions of the enterprise.

P. 1340 "Revaluation of non-current assets" here is postponed information from the loan balance. 83, which contains data on the revaluation of NMM and fixed assets.

P. 1350 " Extra capital»Includes credit balance data. 83, from which information on the revaluation of long-term assets is excluded.

In p. 1360 "Reserve Capital" reflects the loan balance on the account. 82, which shows the amounts created in accordance with the charter or legislation of reserves. Here is the part of the balance of the account. 84, which falls on special funds.

In p. 1370 "Retained Profit" records information on the part of the SC. 84, reflecting the unused profit of the company. When calculating, amounts to special funds should be deleted.

In p. 1300 balance should be summed up and record the total of all values \u200b\u200bof the indicators of section III C Art. 1310 to 1370.

long term duties

In p. "1410" " Borrowed funds»Reflect the credit balance data. 67, and here it is necessary to indicate both the sum of the amount of debt and accrued interest.

In p. "1410" " Borrowed funds»Reflect the credit balance data. 67, and here it is necessary to indicate both the sum of the amount of debt and accrued interest.

P. 1420 "Deferred tax obligations"Includes an indicator calculated by subtracting from the loan balance. 77 Balance on the debit of sch. 09.

P. 1430 "Evaluation Obligations" is intended to reflect the information on the loan of subaccounts. 96 on reserves of upcoming expenses, as well as estimated reserves with a period of more than one year.

P. 1450 "Other obligations" reflects the balances on the loan. 60, 62, 68, 69, 70, 76, containing information about debt over one year.

In p. 1400 balance sheet should be summed up and recorded all the values \u200b\u200bof the indicators of section IV, namely Art. 1410-1450.

Short-term liabilities

In p. 1510 "borrowed funds" should reflect the loan balance in the account. 66, while it must contain both the debt itself and interest accrued on it.

In p. 1510 "borrowed funds" should reflect the loan balance in the account. 66, while it must contain both the debt itself and interest accrued on it.

In p. 1520 " Accounts payable»The following accounting data should be specified:

- Credit balance. 60 and sch.76, which reflect the existing debt of the business entity in front of its partners, serving suppliers and contractors.

- Loan balance. 70, which includes the indebtedness of the enterprise in front of people working on it. However, it must be remembered that the debt on the payment of income is not reflected here.

- The amount of accounts payable 76 by subaccount "Calculations on depositiated debt", which reflects not paid amounts of deposited salary.

- Loan balance. 68 and sch. 69, which takes into account the debt of the company before the budget and extrabudgetary funds For mandatory payments.

- Loan balance. 71, which makes accounting for the existing debt of accountable persons in front of the enterprise.

- Credit balances on sch subaccounts. 76 "Calculations for property insurance"And" Calculations for claims. "

- Loan balance. 62 and 76, on which they are reflected from buyers the amount of advance payments.

- The balance of the loan of subaccounts is sch. 70 "Calculations on the payment of income on shares" and sch. 75 "Calculations for income payment".

In addition, this section shall be disclosed as follows:

- P. 1530 "Income of future periods" is intended for fixing balances in it. 86 and sch. 98.

- P. 1540 "Evaluation Obligations" contains balance on the loan of the SCC. 96 "Reserves of upcoming expenses", as well as on accounts where they are reflected estimated obligationsmi with deadlines less than one year.

- P. 1550 "Other short-term commitments" other obligations of the company with a period of less than one year, which were not reflected in section V report form on OKD 0710001.

- In p. 1500 of this report should be summed up and recorded the total values \u200b\u200bof the indicators p. 1510-1550.

Attention! P. 1700 "Balance" reflects the balance currency, which is determined by the addition of the values \u200b\u200bof the final lines of the liabilities: p. 1300, page 1400, p. 1500.

Common bugs when filling the balance

The following most common errors can be distinguished when drawing up balance sheet:

- Indicators of receivables and payables Many experts fold. It is necessary to indicate the balance sheets as follows: accounts receivable as part of the balance of the balance sheet, the creditor - in the liabilities. For example, debt buyers in the asset, and advances received from them - in the password of the report.

- Receipts from buyers in the form of an advance should be reflected together in addition to its VAT.

- Long-term objects. For which depreciation is charged must be indicated in the balance at the residual value, and not at the initial one. Many here allow a mistake.

- When an organization provides a loan, in which the calculation of interest is not provided for, it should be reflected not in financial investments, but as part of receivables, by dividing the terms of payment.

- When filling out the balance, many accountants have negative values \u200b\u200bof indicators indicate in graphs with the "-" sign.

Balance of typical shape number 1. Filling out an accounting balance occurs in thousands and millions of rubles as well, it does not contain any decimal signs after the comma. If you have an accounting balance foreign currency, then it is recalculated as a domestic at the rate of the Central Bank for the thirty-first. From the ruble and salad statement take data and fill out all accounting balances.

IN balance form In the upper line, the date on which the balance is made. For example "December 31, 2011." Further indicates the abbreviated or full name of the company, an identification number The taxpayer and the type of activity, which is approved by state statistical bodies. Next, in the completion of the balance sheet, you should specify the code of organizational and legal form of the company, as well as the property code for classifiers, which correspond to OKFS and OKOPF. Choose a suitable unit of measurement and then specify its code, for example 385-thousand. rub.; 182-million rub. In the form of accounting balance In the "Location" line you want to specify legal address firms. Further, the Blanc Blanc includes data to the "Approval Date" line, where the date is set for annual reporting. The "Sending / Adoption Date" line indicates the exact date of the accounting reporting date, sending to e-mail, mail, or in other ways, and also, in this line, you can specify the date for the actual transmission of the balance sheet.

Now go to the table to fill the balance sheet. It consists of five sections: three sections relate to the liabilities of the organization, and two to the assets of the organization. You can download an accounting balance form. In the empty graphs of the shape of the balance sheet, are cast. The balance at the beginning of the year is recorded on accounting accounts to the third column. Next comes filling the fourth graph. In the last and final line 190 of the balance sheet for each appropriate graph, the lines of one hundred ten are one hundred and fifty.

For filling an accounting balance The final line 290 of the second partition for each appropriate graph is folded two hundred ten - two hundred seventy. The three-line line is written to the string line one hundred and ninety - two hundred ten. In the line 490, when the balance of the balance sheet fits the amount of four hundred ten-tech seventy years, the line of four hundred eleven is not taken into account. The line 590 records the amount of five hundred ten - five hundred twenty. The line 621 indicates the amount of the strings of six hundred twenty one - six hundred twenty five. In line 690 of the fifth section, the sums of six hundred ten, six hundred twenty, six hundred thirty - six hundred sixty are recorded. And in line 700, the amounts of such lines should be specified: four hundred ninety, five hundred and ninety, six hundred and ninety, three liabilities partitions.

Accounting balance form №1 confirmed by the signature with the decoding of the chubbuch and the leader. Date is indicated by title page Opposite the Count Graphs.

Everything russian organizationsAs well as official representative offices of foreign companies in our country are obliged to report on their financial and economic regulations for the reporting year. This commitment is regulated by the Law "On Accounting" No. 402-FZ.

Also, the law provides for "cross-partings" for some categories economic Subjectswho are entitled to keep accounting in simplified form. However, regardless of the way of maintaining accounting, the main or simplified, form number 1 is mandatory for all economic entities: organizations, IP and private owners.

This year will have to form reporting for 2017. The current form is approved by the Order of the Ministry of Finance of Russia No. 66n dated 02.07.2010.

Form 1 "Accounting Balance", download Word Blank

Download Accounting Blanca 2019, Excel

Accounting Balance with Line Codes, Blank, Excel

How to Fill Balance

When filling out the form number 1, we should guide the section 4 of the Order of the Ministry of Finance of the Russian Federation of 06.07.1999 No. 43N (ed. From 08.11.2010). We define the key rules for filling out the reporting document:

- fill out the report indicators in accordance with the actual balances of Busts at the reporting date, formed taking into account the requirements of the PBU and the Company's accounting policy;

- reflect the indicators in monetary terms in the currency of the Russian Federation - in rubles, thousands of rubles or in millions of rubles;

- if the company has a branch network, then at the end of the year, a single accounting balance should be formed (the parent company plus branches);

- to short-term assets and obligations include indicators that exist no more than 12 months to long-term - existence of more than one year;

- property and main funds should be reflected in the "clean" cost, that is, taking into account depreciation deductions and other expenses provided for by PBU.

We offer a simple cheat sheet for filling out form No. 1.

An example of a filled form

When and where to donate reporting

In 2017, it is necessary to provide accounting statements in form No. 1 at once in several organizations: FTS and Rosstat - for all organizations and IP, to the Ministry of Justice and (or) to the Ministry of Finance of Russia - for non-Profit Organizations and state employees. Upon additional request, accountability can be requested by the founder or owners of the company.

Provide Balance B. Tax inspection and Rosstat for 2017 need no later than 90 calendar days From the first day of the year following the reporting period. That is, no later than 31.03.2018. However, in 2019, March 31 drops on a day off, therefore, the transfer rule is valid. It means that the deadline for the delivery of the accounting balance for 2017 is 04/02/2018.

For organizations of the budget sector, there may be other deadlines for reporting, earlier. This information is brought to institutions in the prescribed manner.

Reporting, filed in the Ministry of Finance, the Ministry of Internal Affairs or the founder, does not cancel the obligations to report to the Federal tax Service and territorial statistical authorities within the specified time.

Terms of delivery for "special" cases

Note that for newly educated, liquidated and reorganized enterprises, the deadlines are somewhat different. Consider the extraction dates for reporting for such companies:

- Creature. The organization that was formed before September 30, 2017 is obliged to report on the generally accepted rules, that is, until 04/02/2018. But those companies that were formed after September 30, 2017 must report not in 2019, and in 2019, that is reporting period 2019 plus existence period in 2017.

- Reorganization. The company is obliged to report three months after making recent changes in the register. This rule is established not only for firms that continued their activities, but also for "attached" companies that completed their activities.

- Liquidation. The institution that completed its activities is officially obliged to provide reports no later than three calendar months from the date of appropriate entries in the register.

- Annual balance with USN delivery time for 2015

- Blanca for 2015 new form free download

- Blanca for 2015 Sample

Balance with USN in a new form only surrender organizations. Entrepreneurs do not fill and do not pass the balance. Simplified-firms related to small businesses are entitled to choose: either fill the balance on the usual form, or by simplified. The rest of the simplists who do not fall under the criteria of small firms, give the balance on the usual form. Balance form with USN for 2015 is on our website. Please note that when you subscribe to our magazine, the book "Simplified. Annual Report 2015".

Blanca for 2015 new form free download

GNIVTS FNS of Russia has prepared a machine-readable form of accounting (financial) reporting. Since the Federal Tax Service of Russia recommends accountants to report precisely on this form, we place it for download. The difference between this form is that the details (FULL NAME, OKVED, name, etc.) you put once on the first two sheets of form. And in the balance sheet and the report on the finisults, they are not necessary to write. In addition, a special barcode is applied in the upper left corner of each sheet. This barcode is not on official form of the Ministry of Finance. And the tax authorities without this barcode can not accept reports.

Blanca for 2015 New Form Free Download You can on our website:

- PDF.

- Download Simplified EXEL's Accounting Form

- PDF.

In the reporting form, fill in those lists that are required for your case. For example, if targets You did not use, then the report on target use funds you do not fill and do not pass.

After filling out the report, print it in 2 copies, sign up (signs the director, can sign an accountant or another employee, but only by proxy) and hand over one copy to the Rosstat branch, and the second - in the IFTS. IP Accounting reports do not pass.

- See also (to download, take trial access or)

The term of the balance for 2015 in the tax

The term of the balance for 2015 in the tax asked many accountants.

Question: Annual balance sheet deadlines for 2015? Answer: S.rock delivery of the balance for 2015 - no later than March 31, 2016. The balance is surrendered in the accounting statements in the inspection and statistical authorities (one copy).

Entrepreneurs Accounting reporting do not pass.

Accounting balance on simplified form in 2016

The simplified form of an accounting balance provided in Appendix No. 5 to order No. 66n can only be used by subjects of small entrepreneurship and contains graphs in which they lead enlarged indicators for each article:

Balance with USN consists of an asset and liability. The final indicators of partitions are calculated in lines with codes 1600 and 1700 and should be equal. The codes along the rest of the rows are affixed in their own added column 2 indicate the indicator that has the highest specific weight in the structure of the enlarged indicator (clause 5 of the Order No. 66n).

The asset reflects the amount of non-current and current assets, in passive - size own capital and borrowed funds, as well as accounts payable.

We list what is included in the integrated article of the simplified balance. At the same time, we will not specifically relate to the constituent of each indicator, we will not talk in detail about this further when we proceed to the balance based on general form.

After consideration of all forms, we present an example of filling the simplified form of an accounting balance. And also for comparison, a sample of the balance of the balance in general form.

Asset of simplified balance for 2015

Material non-current assets. This line reflects, in particular, fixed assets and unfinished capital investments in fixed assets.

Intangible, financial and other non-current assets. The name of the article suggests that the intangible assets and long-term financial investments should be reflected in it. The string also includes research results and developments, incomplete investments in intangible assets, research and development.

Stocks. This string should not cause special issues. Since the article is the same name in the usual form of an accounting balance.

What is stated in relation to the previous line applies to this.

Financial and other revolving assets. The string is designed to reflect short-term financial investments, receivables and other assets.

Passive Simplified Balance for 2015

Capital and reserves. This includes authorized capital, added and reserve capital (if available), retained earnings ( uncoated loss), reassessment of fixed assets ( intangible assets) If this is carried out. Also own shares, redeemed from shareholders to cancel (the share of founders).

Long-term borrowed funds. Here are the borrowed funds obtained by long-term loans and loans.

Short-term borrowed funds. This line is designed to reflect the borrowed funds obtained by short-term loans and loans.

Accounts payable. The amount of other short-term debt Organizations in front of its creditors indicate this line.

For indicators that remained irresistible, lines "Other long term duties"And" other short-term obligations. "

Accounting Balance for 2015 Total Shape

- Download the general form of accounting reporting PDF

The total balance of the balance is given in Appendix No. 1 to the order number 66n. And, as we have already said earlier, the subjects of small businesses have an alternative - simplified balance. But no one for such firms prohibits applying a common form.

Balance in general form has graphs in which each article leads indicators:

- at the reporting date (when filling out the balance for 2015 - as of December 31, 2015);

- as of December 31 of the previous year (when filling out the balance for 2015 - as of December 31, 2014);

- as of December 31, the previous year preceding the previous one (when filling out the balance for 2015 - as of December 31, 2013).

Count 1 of the balance is designed to indicate the number of the corresponding explanation to the accounting balance (if an explanatory note is drawn up).

Count 3 organizations add themselves to the stroke code in it.

The balance contains two parts - an asset and passive that should be equal to each other. The asset reflects the amount of non-current and current assets, and in passive - the size of equity and borrowed funds, as well as accounts payables.

Section I of Balance in general form for 2015. Fixed assets

Intangible assets. The residual value of intangible assets is reflected on line 1110. Paragraph 3 of PBU 14/2007 "Accounting for intangible assets", approved by the Order of the Ministry of Finance of Russia dated December 27, 2007 No. 153n, lets what belongs to this group. So, for taking accounting of an object as an intangible asset, it is necessary that the following conditions are carried out at the same time:

- the object is able to bring economic benefits in the future, and the organization has the right to receive them;

- the object can be highlighted or separated (identified) from other assets;

- the object is intended for use for a long time, that is, its term useful use exceeds 12 months;

- it is possible to reliably determine the actual (initial) cost of the object;

- the object does not have a material and real form.

For example, when performing these conditions, the intangible assets include works by science, literature and art, programs for electronic computing machines, inventions, useful models, selection achievements, secrets of production (know-how), trademarks and maintenance signs. As part of intangible assets also take into account the business reputation arising in connection with the purchase of an enterprise as a property complex (as a whole or part of it).

note: Intangible assets are not the costs associated with education legal entity (organizational expenses), intellectual and business qualities of staff personnel, their qualifications and labor ability (p. 4 PBU 14/2007).

Results of research and development. Expenses for research and development, invited on account 04 "Intangible assets" reflected on line 1120.

Intangible and material search assets. These two indicators are listed in lines under the numbers 1130 and 1140. They are intended to organizations - users of subsoil to reflect information on mastering costs natural resources (PBU 24/2011 "Accounting for the expenditure of natural resources", approved by the Order of the Ministry of Finance of Russia from 06.10.2011 No. 125n).

Fixed assets. According to amortized objects, the residual value of fixed assets is recorded in line 1150. If we are talking about non-immitrable property, then in the line indicate it initial value.

Assets found to fixed assets must comply with the conditions of clause 4 PBU 6/01 "Accounting for fixed assets", approved by the Order of the Ministry of Finance of Russia of 30.03.2001 No. 26N.

Objects must be owned by the organization or on the right of operational management or economic management. The basic means are allowed to include the property obtained under the lease agreement, if it is taken into account on the balance sheet of the lessee.

Objects subject to mandatory state registration of property rights are considered to be fundamental funds from the moment they are registered, that is, as well as all other objects. The fact of filing documents in the appropriate instance does not matter.

In the Balance Forms section, there is no stroke "unfinished construction". The question arises: what kind of balance sheet it is necessary to reflect the cost of building real estate objects? The answer is simple - on line 1150 "Fixed assets". This is stated in paragraph 20 of PBU 4/99, approved by the Order of the Ministry of Finance of Russia of 06.07.99 No. 43N. And it is best to line 1150 add a decoding string "unfinished construction", according to which the named costs are written.

Profitable investments B. material values . Data on profitable investments in material values \u200b\u200bcorresponds to the Row Row 1160. This residual value The property intended for rental (leasing) and accountable on account 03. If the property was first used for the needs of production and management, but in the future it was leased, it must be reflected in a separate subaccount of account 01 as part of fixed assets. It is caused by the fact that the transfer of the value of fixed assets in the revenue investments and back in accounting is not provided (letter of the Federal Tax Service of Russia dated 19.05.2005 No. GW-6-21 / [Email Protected]).

Financial investments. For long-term financial investments, i.e., with a period of circulation for more than a year, the line 1170 is assigned (for short-term - line 1240 of section II "Current assets"). Here is the investment in subsidiaries, dependent and other societies. Financial investments are accepted for accounting in the amount spent on their acquisition.

Do not forget: the cost of own shares bought from shareholders to resale or cancellation, and interest-free loans issued to employees do not refer to financial investments (paragraph 3 of PBU 19/02 "Accounting for Financial Investments", approved by the Order of the Ministry of Finance of Russia of December 10, 2002 126N). For the first indicator, line 1320 is provided. The second indicator reflects in the composition of receivables, namely: long-term loans are shown on line 1190, short-term - on line 1230.

Deferred tax assets. Line 1180 "Deferred Tax Assets" fill in profits tax payers. Since "simplities" are not included in their number, it must be put in it.

Other noncurrent assets. Here (line 1190) shows data on non-current assets that have not found reflections on other rows of the accounting balance of the Balance.

SECTION II BALANCE ON MODY FOR 2015. Current assets

Stocks. The cost of material reserves is reflected in line 1210. Previously, this indicator needed to decipher. In the existing form, the decoding is not required. However, it is needed if the indicators included in the string 1210 are essential. In this case, add decoding lines, such as such:

- raw materials and materials;

- costs in incomplete production;

- finished products and resale products;

- goods shipped, etc.

Value Added Tax on Acquired Values. This line with the code 1220 "Simplifiers" can be filling out if, according to the accounting policy of the organization of the amount of "entrance" VAT, the account of 19 "Value Added Tax on Acquired Values" is recorded.

Receivables. This line 1230 is designed for short-term receivables, that is, the repayment of which is expected within 12 months after the reporting date.

Financial investments (with the exception of cash equivalents). For these assets, line 1240 is provided, according to which, in particular, loans provided by the Organization for a period of less than 12 months have been shown.

If you define the current market value Financial investments, use all sources available to you, including data from foreign organized markets or trade organizers. Such recommendations are contained in the letter of the Ministry of Finance of Russia dated January 29, 2009 No. 07-02-18 / 01. If at the reporting date you cannot determine the market value on the previously evaluated object, reflect it at the cost of the last assessment.

Cash and cash equivalents. To fill the line, you need to summarize the cost of cash equivalents (balance of relevant accounts of account 58) and balances on cash accounts (50 "Cassa", 51 "Current accounts", 52 "Currency Accounts", 55 "Special Accounts in Banks" and 57 "Translations on my way").

The concept of cash equivalents, we recall, is contained in the accounting office "Report on cash flow" (PBU 23/2011), approved by the Order of the Ministry of Finance of Russia of 02.02.2011 No. 11n. Cash equivalents can be assigned, for example, open in credit organizations Deposits to demand.

Other current assets. Here (Row 1260) shows data on turnover assets that did not find reflections on other strings of the Balance II section.

Section III balance in general form for 2015. Capital and reserves

Authorized capital (share capital, charter capital, contributions of comrades). On line 1310 of the accounting balance reflect the amount of the authorized capital of the company. It should coincide with the sum of the authorized capital, which is recorded in the constituent documents of the company.

Own shares repurchased from shareholders. We have already said that if the organization bought out his own shares (the shares of the founders) in the authorized capital is not for sale, then their costs are made in line 1320. Such shares are allowed to cancel, which automatically leads to a decrease in the authorized capital, so the indicator of this line as the value is negative lead in brackets. But if your own stocks are redeemed and resold, they are already considered asset and their cost must be entered into a string of 1260 "Other current assets".

Revaluation of non-current assets. This line is assigned number 1340 (notice, the indicator for the string with the number 1330 is not provided). It shows the order of the facilities of fixed assets and intangible assets, which is taken into account on account 83 "Extreme Capital".

Extreme Capital (without revaluation). The amount of additional capital is reflected in line 1350. We note that the indicator for this line is taken without taking into account the amounts of the revaluation, which should be reflected in the string above.

Reserve capital. The balance of the reserve fund indicates line 1360. It reflects both reserves formed at the request of the legislation and reserves created in accordance with the constituent documents. The decoding is required only if the indicators are essential.

Retained earnings (uncovered loss). Accumulated for all the years, including the reporting, retained earnings is shown in line 1370. According to it, they reflect uncovered loss (only such an amount consists in brackets).

The components of the indicator (profit (loss) for the reporting year and (or) for previous periods) can be recorded in additional lines, that is, make decryption on the received financial results (Profit / loss), as well as for all years of the company.

Section IV. Long-term obligations in the balance for 2015

Borrowed fundsStroke 1410 is allocated for the debt of the organization itself on the long-term (with a maturity date on December 31, 2015 more than 12 months) loans and loans.

Deferred tax liabilities. Startup 1420 fill in profits tax payers. "Simplifiers" are not included in their number, therefore they put in this row.

Estimated obligations. This line 1430 is filled, if the organization recognizes evaluation obligations in accounting, according to the Accounting Regulation "Estimated obligations, subject obligations and conditional assets "(PBU 8/2010), approved by the Order of the Ministry of Finance of Russia dated December 13, 2010 No. 167n. Recall, the subjects of small entrepreneurship, which are most of the "simplists", may not apply this PBU.

Other obligations. Here (line 1450) shows other long-term liabilities that did not find reflections on other lines of the section IV balance. Note, the indicator for the line 1440 by order No. 66n is not provided.

Section V. Short-term obligations

Borrowed funds. The line 1510 indicates the debt on short-term loans and borrowings taken for a period of not more than 12 months. At the same time, the amount should be reflected in mind the interest due to pay at the end of the reporting period.

Accounts payable. Total Credit debts are fixed in line 1520. And it should be only short-term debt.

Note that there is no separate line for debt to participants (founders) on income pay. The amount of such debt should include here and decipher separate stringSince this indicator is always essential.

revenue of the future periods. Stroke 1530 is filled when accounting to accounting provisions are provided for recognition of this accounting object. For example, if your organization receives fiscal funds or target financing amounts. Such means are just subject to accounting as part of the income of future periods in the accounts 98 "Incomes of Future Periods" and 86 " Special-purpose financing"(P. 9 and 20 accounting provisions" Accounting state aid"(PBU 13/2000), approved by the Order of the Ministry of Finance of Russia of October 16, 2000 No. 92n).

Estimated obligations. Here are the explanations that we gave to line 1430: the line 1540 is filled, if the firm recognizes the accounting obligations in accounting. Only in line 1430 reflect long-term liabilities, and in line 1540 - short-term.

Other obligations. The line 1550 shows other short-term liabilities that did not find reflections on other lines of the Balance section.

Determination of accounting indicators for general form for 2015

Our scheme will help determine the indicators of the balance sheet in general form (debit and credit balance on account accounts will be denoted by DT and CT, respectively).

Section I "non-current assets"

Row 1110 "Intangible assets" \u003d DT 04 (without expenses for R & D) - CT 05.

Row 1120 "Research and Development Results" \u003d DT 04 (analytical account of accounting for R & D spending).

Row 1130 "Intangible search assets" \u003d Dt 08 (Analytical account of expense accounting for intangible search costs).

Row 1140 "Material Search Assets" \u003d Dt 08 (analytical account of expenses for material search costs).

Row 1150 "Fixed Tools" \u003d Dt 01 - CT 02 + DT 08 (analytical account of accounting for incomplete construction).

Row 1160 "Profitable investments in material values" \u003d DT 03 - CT 02 (analytical account of accounting for the depreciation of property relating to profitable investments).

Row 1170 "Financial Investments" \u003d Dt 58 + Dt 55 subaccount "Deposit accounts" + Dt 73 subaccount "Calculations for loans provided" (analytical accounts of accounting for long-term financial investments) - CT 59 (analytical account of accounting for long-term financial investments).

Row 1180 "Deferred tax Active» \u003d Dt 09.

Row 1190 "Other non-current assets" \u003d The cost of non-current assets, not taken into account in other indicators of the accounting balance of the Balance.

Row 1100 "Total to section I"\u003d The sum of the indicators of strings 1110-1190.

Section II "Current Assets"

Row 1210 "Stocks" \u003d debit balance accounts 10, 11, 43, 45, 20, 21, 23, 28, 29, 44 + dt 41 - CT 42 + DT 15 + DT 16 (or DT 15 - KT 16) - CT 14 + Dt 97 (Analytical account of expense accounting with a degree of write-off less than 12 months).

Row 1220 "VAT on acquired values" \u003d DT 19.

Row 1230 "Accounts receivable" \u003d Dt 62 + Dt 60 + Dt 68 + Dt 69 + Dt 70 + + Dt 71 + Dt 73 (except percentage loans) + Dt 75 + Dt 76 - CT 63.

Row 1240 "Financial investments (with the exception of cash equivalents)" \u003d Dt 58 + Dt 55 subaccount "Deposit accounts" + Dt 73 subaccount "Calculations for loans granted" (analytical accounts for accounting for short-term financial investments) - CT 59 (analytical account of the accounting of a reserve for short-term financial investments).

Row 1250 "Cash and cash equivalents" \u003d Dt 50 + Dt 51 + Dt 52 + Dt 55 + Dt 57 - Dt 55 subaccount "Deposit accounts" (analytical accounts for accounting for financial investments).

Row 1260 "Other current assets" \u003d The cost of current assets, not included in other indicators of the Balance II section.

Row of 1200 "Total in section II" \u003d The sum indicators 1210-1260.

Row 1600 "Balance" \u003d Row indicator 1100 + string indicator 1200.

Section III "Capital and Reserves"

Row 1310 "Authorized capital" \u003d CT 80.

Row of 1320 "Own shares repurchased from shareholders" \u003d Dt 81. Enclose the indicator in brackets.

Row of 1340 "Revaluation of non-current assets" \u003d CT 83 (analytical account of accounting amounts of accommodation of fixed assets and intangible assets).

Row 1350 "Extension Capital (without revaluation)" \u003d CT 83 (except the amount of the accommodation of fixed assets and intangible assets).

Row of 1360 "Reserve Capital" \u003d CT 82.

Row 1370 "Retained earnings (uncovered loss)" \u003d CT 84 (Dt 84). With the debit balance - the indicator is negative (that is, there is a loss), enter it into brackets.

Row 1300 "Total section III» \u003d The sum of the indicators of strings 1310-1370. If the result is negative (if there are negative indicators on strings 1320 and 1370), show it in parentheses.

Section IV "Long-term liabilities"

Row 1410 "borrowed funds"\u003d CT 67. At the same time, the accrued interest, the maturity of which at the reporting date is less than 12 months, should be excluded and reflected on line 1510 (preferably with decoding).

Row 1420 "Deferred Tax Obligations" \u003d CT 77.

Row 1430 "Estimated obligations" \u003d CT 96 (only evaluation obligations with a validity period of more than 12 months after the reporting date).

Row 1450 "Other obligations" \u003d Long-term debt that did not enter other indicators of the Balance IV section.

Row 1400 "Total to section IV" \u003d The sum of the indicators of the above rows 1410-1450.

Section V "Short-term obligations"

Row 1510 "borrowed funds" \u003d CT 66 + CT 67 (in terms of accrued interest, the maturity of which at the reporting date is not more than 12 months).

Row 1520 "Credit Debt" \u003d CT 60 + CT 62 + CT 76 + CT 68 + CT 69 + CT 70 + CT 71 + CT 73 + CT 75. In this case, consider only short-term debt.

Row of 1530 "Incomes of future periods" \u003d CT 98 + CT 86 in terms of target budget financing, grants, technical assistance, etc.

Row 1540 "Evaluation Obligations"\u003d CT 96 (only estimated obligations with a validity period of not more than 12 months after the reporting date).

Row 1550 "Other obligations" \u003d amounts of debt short-term obligationsnot taken into account when determining other indicators of the V balance sheet.

Row 1500 "Total by section V" \u003d The sum of the indicators of strings 1510-1550.

Row of 1700 "Balance" \u003d Row indicators 1300 + 1400 + 1500.

If everyone economic operations Refilled correctly and properly transferred to the balance, indicators of strings 1600 and 1700 coincide. If this equality is not respected, an error is made somewhere. Then you need to check, recalculate and adjust the entered data.

An example of completing the balance sheet for general and simplified form

On the same figures, let's see how to fill the annual balance sheet on the usual form and on simplified.

Small enterprise balance completed example of 2015LLC "Nasturtia", registered in 2015, applies a simplified tax system. Indicators of accounting registers at December 31, 2015 are shown in the table below. Table residues (CT - credit, DT debit) on accounting accounts as of December 31, 2015 "Nasturtia" Based on the available data, the accountant compiled an accounting balance for 2015 in general, as well as for comparison - on simplified. Samples of completed balances will be found in a separate section along with samples of completed financial results. In the header part in the string "at ___ 20__g. "Each form indicates: December 31, 2015. After that, the full name of society, type of activity, organizational and legal form and form of ownership are inscribed. The location of the company (address) is also indicated. The right codes are reflected on the right in special fields. Since the company was registered in 2015, in the last two graphs of each form of balance instead of indicators of dirty fiber. Balance of general form All lines of Count 1 Accountant fucked. This is possible because the organization does not make out explanations of the financial statements, the numbers of which indicate this column. Graph 4 is the only one that requires the fill in the newly created organization. The specified column reflects the data as of December 31 of the reporting year, that is, 2015. Count 3 is also added to specify row codes. Row indicator 1110 "Intangible assets" Accountant defined as follows: from the debit balance of the account 04 The loan balance of the account 05 is deducted. Total we get 96,660 rubles. (100 000 rub. - 3340 rubles.). All values \u200b\u200bin the balance sheet are indicated in total thousands, therefore 97 is recorded in line 1110. The indicator of the line 1150 "fixed assets" is defined as follows: the debit balance of the account 01 - the credit balance of the account 02. The result - 579 960 rubles. (600 000 rub. - 20 040 rub.). 580 recorded in the balance sheet. In line 1170 "Financial investments" is inscribed by a debit balance of accounts 58 - 150 thousand rubles. (That is, it is believed that all investments are long-term). The summary of the summary line 1100: 827 thousand rubles. (97 thousand rubles (line 1110) + 580 thousand rubles. (Line 1150) + 150 thousand rubles. (Rowing 1170)). Now turn turning assets. The value of the line 1210 "stocks" is defined as follows: debit balance account 10 + debit balance account 43. Result - 107 thousand rubles. (17 thousand rubles. + 90 thousand rubles.). The indicator of the line 1220 "Value Added Tax on Acquired Values" is equal to the debit balance of the account 19, so the balance sheet has made 6 thousand rubles. The indicator of the line 1250 "Cash and cash equivalents" was found by adding a debit balance of account 50 and debit balance of account 51. The result is 265 thousand rubles. (15 thousand rubles. + 250 thousand rubles). 265 is recorded in the string. The summary of the summary line 1200: 378 thousand rubles. (107 thousand rubles (line 1210) + 6 thousand rubles. (Row 1220) + 265 thousand rubles. (Line 1250)). At the final line 1600 shows the amount of indicators of strings 1100 and 1200. That is 1205 thousand rubles. (827 thousand rubles. + 378 thousand rubles). In the rest of the lines of the column 4 affixed fiber. Go to the balance liability. The indicator in line 1310 "The authorized capital (share capital, the authorized capital, contributions of comrades)" is equal to credit balance account 80, that is, there are 50 thousand rubles in the balance sheet. Row of 1360 "Reserve Capital" - credit balance account 82. In our case, it is 10 thousand rubles. In line 1370 "Retained earnings (uncovered loss)" is shown an account balance 84. It is loan. So, the organization at the end of the year has profits. Its value is 150 thousand rubles. You do not need to take an indicator in brackets. The indicator of the summary line 1300 is 210 thousand rubles. (50 thousand rubles. (Line 1310) + 10 thousand rubles (line 1360) + 150 thousand rubles. (Row 1370)). The indicator for the line 1520 "Accounts' debt" (the accountant considered that all the debt is short-term) is defined as follows: Credit balance account 60 + credit balance account 62 + credit balance account 69 + account credit balance 70. Result - 995 thousand rubles. (150 thousand rubles. + 506 thousand rubles. + 89 thousand rubles. + 250 thousand rubles.). In the line 1500, the accountant moved the value from the line 1520, since the other lines of the V balance sheet were not filled. The final line 1700 is equal to the sum of the rows 1300 and 1500. The value obtained is 1205 thousand rubles. (210 thousand rubles. + 995 thousand rubles.). The remaining lines of the lassive due to the lack of relevant data are switched. Indicators of final strings 1600 and 1700 are equal. And in that and in another line the value - 1205 thousand rubles. Balance fell asleep - it means that the form can be considered true. Balance of simplified form Here are filled colors 2 and 3 forms. At the same time, the Count 2 accountant added independently to reflect the line code. The column 3 reflects the values \u200b\u200bof the indicators directly. The cost of fixed assets of 580 thousand rubles. The accountant reflected under the article "Material non-current assets". The row code is 1150. Intangible assets (97 thousand rubles) are shown on the line "Intangible, financial and other non-current assets". This also includes financial investments (the accountant considered that all of them are long-term) in the amount of 150 thousand rubles. The final line indicator is 247 thousand rubles. (97 thousand rubles. + 150 thousand rubles.). Since the share of financial investments in the indicator is larger than the proportion of intangible assets, the line code 1170 is set (according to the "Financial Investments"). The same indicator that accountant calculated for the general form of balance, as the rules for calculating and filling out this string are the same. That is, on this line reflected 107 thousand rubles. And set code 1210. The line "Cash and cash equivalents" includes only cash in the amount of 265 thousand rubles. Row code - 1250. From current assets that have not reflected on the balance sheets specified above, value added tax remained, therefore its amount (6 thousand rubles) The accountant has stailed in the line "Financial and other revolving assets" (line code - 1260). The final indicator of the asset section (line 1600) is equal to the sum of the filled strings 1150, 1170, 1210, 1250 and 1260. And now the liabilities of the balance. Authorized and reserve capital as well retained earnings Reflected on one line "Capital and reserves". The amount of the string is 210 thousand rubles. (50 thousand rubles. + 10 thousand rubles. + 150 thousand rubles). The row code is placed in terms of the largest proportion of the enlarged indicator. This is retained earnings. Therefore, the row code is 1370. In the rest of the lines of the Graph 3 of the liability are rocked, since there are no indicators for filling. In column 2, it is permissible to do the same. Or you can specify the code that matches the indicator that the accountant did. The outcome of the liabilities section (line 1700) is equal to the sum of the rows 1370 and 1520. I will verify the indicators of strings 1600 and 1700. In both, in another line, the value is 1205 thousand rubles. Balance fell asleep - it means that the form can be filled true. Sample Fill Balance for Simplified Form 2015Sample Filling Balance in General Form for 2015

|

On our site you can also read everything on the topic. balance Reformation 2016. In the article: "Balance Reformation before drawing up accounting reporting for 2015." And you can arrange a subscription to our magazine, access to the site will open within 2-3 hours