Picking up a loan, the borrower is studying credit products A number of banks, draws attention to the promotions of credit institutions offering low interest rates on loans. But few people know that

What is the full cost of the loan?

The total cost of the loan (PSK) is the amount that the client will actually pay the bank for the use of funds, the real loan price.

The practice of disclosing the present price of the bank loan appeared in Russia not immediately, but after several years of indignant misunderstanding between credit institutions and borrowers. Psychologically, the loan price under 11% per annum seems attractive for 15 years, but according to the result, for the entire repayment period, you will have to pay twice as much as it was taken. The case of the abundance of commissions, as a percentage and with a fixed value even more complicated. Some percentages were calculated from the amount of the residue, while others from the initial loan amount. In such a situation, it is impossible to identify the real cost of the bank loan without complex calculations.

PSK is expressed in%, but does not coincide with the annual interest rate, by contract. This is because the price besides interest, payments for:

- for processing the application and verification of the data of the borrower;

- for registration and maintenance of a loan account;

- for the release of bank cards within the loan agreement;

- for operations in the process of registration and maintenance of the loan;

- insurance cost if conclusion insurance contract is a bank condition for issuing a loan, or determines the amount of rates and commissions on it;

- other customer expenditures directly related to the issuance of a bank loan, including and obligatory payments to third parties.

The total cost of the loan must be calculated before it is received, because Lending conditions are known in advance.

It is important to take into account that the list of expenses included in the PCT is not infinite. It cannot be expanded by analogy, according to one of the parties to the transaction or by the solution of any other people and organizations.

IN Russian Federation Since 2013, the law "O consumer credit (loan). " In the following, 2014, mandatory for banks was the formula for calculating the full cost of the loan (we will talk about below).

In PSK do not contribute:

- The expenses of the borrower committed not under the terms of the loan, but based on the requirements of the law. This may also relate to certain types of insurance.

- Penalties and additional costs associated with violation of payment discipline.

- Additional loan maintenance costs that are a consequence of the selection of the client. Example - an increase in the repayment of the loan, which caused recalculation total amount percent.

- Miscellaneous Commission and additional payments for certain ways to repay the loan: in cash, through terminals of other banks, using third-party payment systems.

- Payment fees in the bank card issued within loan agreement.

It follows from this that the full cost of the loan is not necessarily equal to the amount that the borrower will actually pay the creditor. Because During the repayment process:

- Payment delays or early repayment. The first penalty is charged, the second promises the recalculation of interest and a decrease in the total cost of a loan or penalties, if this is provided for by the contract.

- Changes to the refund conditions of the loan. This possibility is often prescribed in the contract, but its offensive is linked to external circumstances.

These and other circumstances may affect the amount actually paid by the borrower. But if the changes at the time of receiving the loans are not known, or their offensive does not depend on the lender, then they will not include them in the total cost of the loan.

It is important that the full cost of the loan has been known in advance, even before it is received. If the bank hits information about it, the transaction must be invalid, the lending agreement is terminated, and the funds spent by the client are returned to him.

For recipients of bank loans, it is the value of the full cost of the loan, and not the interest rate, should be a criterion for assessing and comparing different credit products.

How to calculate the full cost of the loan?

The process of calculating the real price of a loan occurs according to complex formulas, to learn which for an ordinary consumer for a long time and not necessarily. However, to understand how this calculation is useful.

First of all, we clarify - all payments within the loan are calculated by own formulas. Separately calculated the main percentage, separate commission and other payments (depending on the terms of the contract - on the initial amount or from the unpaid residue). Then all the figures obtained are summed up and make up the total loan price.

The following formulas for calculating the cost of the loan will help to learn payments, and not the principal amount from which interest and other relative values \u200b\u200bare being calculated.

The first of the calculated formulas looks like this:

PSK \u003d I x ChbP x 100;

here Psk is the full cost of the loan; ChBP - the number of basic periods; I - a percentage rate in the base period. Under the base period it is understood as the term between the introduction of mandatory credit payments.

This equation is given in the text of the law "On Consumer Credit (Loan)" and applied.

The upper part of the fraci, with the letters of DC, is the amount of a specific payment. If he is committed against the bank, then the amount is accepted with a positive sign, if this is a loan issuance with negative. The second bracket is the value of the payment in the full base period, the fee is calculated in the period of the period. All results obtained are summed up and in the end equals 0. What does equality mean cash streams obtained by the bank and paid by the borrower. For calculations with a handle and paper, this equation is rarely used. Calculate PSK is more convenient to substitute data into the Excel table with already entered formulas.

The simplified formula for calculating the cost of the loan will help to make an independent calculation:

The calculation on it happens like this:

- the sum of all credit payments (s) is divided into the amount received from the bank (S0);

- from the result of the division, the unit is deducted;

- the resulting number is divided into N - the number of years of repayment of the loan, and is multiplied by 100.

The final value is represented as a percentage. It can be compared with the main interest rate and find out the size of additional overpayment.

An example of calculating PSK.

Calculate the total cost of a loan of 1 million rubles for 2 years, under 10% per annum and with an additional commission of 12 thousand per year. Type of payments - annuity, i.e. equal shares in all periods.

The payment schedule will be like this:

by the main amount | percentage payments | commission | unpaid residue |

||

The overall loan payment is 1 million 131 thousand 478 rubles 32 kopecks. Insert this figure into a simplified formula:

((1 131 478,32/1 000 000)-1)/2*100 = 6,57%.

The total cost of the loan amounted to just over 6 and a half percent per year, i.e. 13.15% in two years.

Why is it not like a declared rate of 10% per annum?

Because interest was charged only on the sum of unpaid residue, but the Commission was accrued from the initial loan amount.

This simple example shows how the reality is very different from what seems clear to the calculation.

How to calculate the cost of a loan online?

Calculation of the full cost of the loan, according to a common (and not simplified) formula, manually, can become a very long exercise in mathematics. Tract time is guaranteed here, and the risk of errors is very large. But, the joy of users, the Internet offers many - programs in which there are already all necessary for the calculation of the formula, and it remains only to put their data into the appropriate forms.

In the practice of finding a loan, calculators will be particularly useful with the possibility of a credit selection of satisfying specified parameters, with the loan search function for the desired amount and with a suitable interest rate. Here is a good example of such a calculator.

2,063 views

Psk (the full cost of the loan) shows a valid interest rate on a loan loan. Previously, this criterion was called an effective interest rate. The parameter takes into account not only the main amount of debt and interest, but also almost all additional payments of the borrower under the terms of the loan agreement (commission, the fee for the credit card, insurance contributions and premiums if insurance affects the procedure for issuing credit loan). Registration fees, penalties, penalties and other payments that do not affect the size and conditions of the loan are not taken into account.

Formula for calculating PSK.

From September 1, 2014 there is a new formula for calculating the full cost of the loan. The foundation - FZ No. 353 dated December 21, 2013 "On the consumer loan (loan)" (see Art. 6 "The total cost of consumer loan (loan)").

For a new settlement of PCC, legislators have established a formula that in a number of foreign countries is used to find an effective annual interest rate (APR, or Annual Percentage Rate).

Formula itself:

PSK \u003d I * BBP * 100.

- ChBP is the number of basic periods in the calendar year. The duration of the calendar year is taken equal to 365 days. With a standard payment schedule with monthly payments according to the AnnuCurt system, ChBP \u003d 12. For quarterly payments, this indicator will be 4. for annual - 1.

- i - interest rate basic period In decimal form. Located in the method of selection as the least positive value of the following equation:

We will analyze the components:

- DP K is the value of the K's thread under the loan agreement. The amount provided by the Bank of the Borrower is included in the cash flow with the "minus" sign. Regular payments on a loan agreement - with a sign "Plus".

- m is the number of payments (the number of amounts in cash flow).

- e k - a period expressed in parts of the established base period, calculated from the time of completion of the QK-th period before the date of the K ww cash payment;

- q k - the number of basic periods from the date of issuance of the loan to the K-wow cash payment;

- i - the base rate in decimal form.

Let us show the calculation on the example.

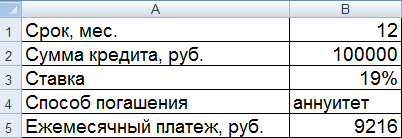

Example of calculating PSK in Excel

The borrower takes 100,000 rubles on 01.07.2016 at 19% per annum. Launch period - 1 year (12 months). The payment method is an annuity. Monthly payment - 9216 rubles.

Create input to the Excel table:

We will calculate:

In our example, it turned out that i \u003d 0.01584. This is the monthly size of the PSK. Now you can calculate the annual value of the value of the loan.

The formula for calculating the PCC in Excel is simple:

For cells with a value, a percentage format is installed, so multiply by 100% no need. We just found the work of the loan term and the interest rate of the base period.

The calculation on the new formula showed a PSK equal to the contractual interest rate. However, in this example, the borrower does not pay additional amounts to the creditor (commission, fees). Only interest.

Consider another example, with additional costs.

Cash flow, respectively, will change. Now the borrower will receive 99,000 rubles in the hands. And the monthly payment will increase by 500 rubles due to the collection.

The interest rate of the base period and the full cost of the loan increased significantly.

This is understandable, because Borrower, except for interest, pays the creditor to the commission and collect. And the collection monthly. Therefore, such a noticeable increase in PSK is observed. Accordingly, the cost of the credit product will cost more.

Not so long ago, federal law No. 353, obliging financial organizations disclose information about the so-called "full cost of a loan (loan)" (hereinafter - PSK).

In this article (in principle, related to workers in the financial sector), I would like to give an example of calculating the PSK. Perhaps someone will come in handy.

Important! Not so long ago, legislators make changes to the formula that enters into force only from September 1, 2014. All the above is only suitable for a new formula. The article describes the exclusively technical implementation of the calculation of the PC in accordance with the norms of the law.

More importantly! The whole information below is relevant for the case when the loan is issued by one payment, i.e. The borrower receives money once, and returns occur on a predetermined payment schedule. This option covers 99% of loans issued (credit cards do not count).

Actually, here is the beast:

Understand the values \u200b\u200bof terms

The PSK is defined as a product of 3 quantities - I, ChPP and Numbers 100. We will analyze the terms used and notation:What is BP (base period)

BP under a consumer loan agreement (loan) is a standard time interval that meets with the highest frequency in the payment schedule under the consumer loan agreement (loan). If there are no time intervals between payments to a duration of less than one year or equal to one year, the BP is missing in the payment schedule of the consumer loan agreement (loan).

In fact, BP is the most common time interval between payments. If there are no recurring time intervals in the payment schedule and other order is not established by the Bank of Russia, the base period is recognized as the time interval, which is the average arithmetic for all periods, rounded up to the standard time interval. The standard time interval is recognized a day, month, year, as well as a certain number of days or months, not exceeding the duration of one year. So you can define your BP. If payments are monthly, then bp \u003d 365/12 ~ \u003d 30What is a BBP (number of base periods in the calendar year)

The definition in the law is very blurred, but as I understand it is the number of basic periods that "go" in one calendar year, i.e.:- For a standard payment schedule with monthly payments: ChBP \u003d 12

- Quarterly payments: ChPP \u003d 4

- Payout once a year or less often: ChbP \u003d 1

- If the payment schedule is cunning: for example, it is foreseen first 2 payouts once a quarter, and then 6 payments once a month, then 3 payments once a day, then the base period is 1 month. A BBP \u003d 12 (12 BP per calendar year).

What is I (the percentage rate of the base period, expressed in decimal form)

It is impossible to understand (at least to me). Perhaps in the definition of the number I there is some point, but this sense to catch intuitively impossible. How to count i - we will analyze in the next section.

How to count I.

Let us leave attempted to understand the "physical" meaning of the number I, and let him definition:The number I is calculated by solving the following equation:

Where:

Where: - m is the number of cash flows, which is equal to the number of payments in the payment schedule plus one (another payment arises due to the first payment - the issuance of the loan).

- DP K - the size of the money flow (issuance of a loan with a "minus" sign, returns with the "plus" sign).

- Q to - the number of full base periods from the moment of issuing a loan to the K th flow. Q to can be calculated by the formula:

Q K \u003d Floor [(DP to -DP 1) / BP], where- DP K - date of the cash flow,

- DP 1 - date of the first cash flow (i.e. Date issuance),

- BP - the term of the base period,

- floor - rounding down to the whole.

- E to - Here you immediately write the formula to your brain to explode from the wording in the law:

E k \u003d MOD [(DP to -DP 1) / BP] / BP, where MOD is the balance of division

Algorithm for calculating PSK.

Incoming data: two arrays. The key is the cash flow number, the values \u200b\u200bare the date of payment and the amount of payment.Outgoing data: PSK value (number).

Calculation procedure:

- Calculate the ChPP (number of base periods). The number of basic periods - how many of these periods "will fit" in 365 days, i.e. PBP \u003d Floor [365 / BP].

- For each k-th payment we consider dp k, q k, e k.

- Methods of approximate calculation exactly up to two signs after the comma, we consider i.

- Multiply ChBP * I * 100.

The code!

there is ready decision On javascript, as well as on VBA (there will be even an Excel file for calculations).Why VBA and Excel?

If suddenly you have a fire and nothing will work on September 1, 2014, the most reasonable thing is to send an Excel sign to the places of conclusion of contracts so that the PSK can be calculated at least so in the first time.

The examples take a schedule for a loan at 100,000 rubles for 3 months at a rate of 12% per annum. Date of issue - September 1, 2014:

Solution on JavaScript

the code

function PSK () (// Incoming Data - Dates of Payments Var Dates \u003d [New Date (2014, 8, 01), New Date (2014, 9, 01), New Date (2014, 10, 01), New Date (2014 , 11, 01)]; // Incoming data - the amount of payments VAR SUM \u003d [-100000, 34002.21, 34002.21, 34002.21]; var M \u003d Dates.Length; // The number of payments // Set the base period BP BP \u003d 30; / / We consider the number of basic periods of the year: var cbp \u003d math.round (365 / BP); // Fill an array with the number of days from the date of issue to the date of the payment varnays \u003d; for (k \u003d 0; k< m; k++) {

days[k] = (dates[k] - dates) / (24 * 60 * 60 * 1000);

}

//посчитаем Ек и Qк для каждого платежа

var e = ;

var q = ;

for (k = 0; k < m; k++) {

e[k] = (days[k] % bp) / bp;

q[k] = Math.floor(days[k] / bp);

}

//Втупую методом перебора начиная с 0 ищем i до максимального приблежения с шагом s

var i = 0;

var x = 1;

var x_m = 0;

var s = 0.000001;

while (x > 0) (x_m \u003d x; x \u003d 0; for (k \u003d 0; k< m; k++) {

x = x + sum[k] / ((1 + e[k] * i) * Math.pow(1 + i, q[k]));

}

i = i + s;

}

if (x > x_m) (i \u003d i - s;) // We consider PSK var psk \u003d math.floor (I * CBP * 100 * 1000) / 1000; // withdraw PSK ALERT ("PSK \u003d" + PSK + "%"); )

Demo on JSFIDDLE: jsfiddle.net/exmmo/m5kbb0up/7

Solution on VBA + Excel

The code

In the column A, starting from the 2nd line there are dates of cash flows.

In column B, starting from the 2nd line there are sums of cash flows.

Sub psk () Dim Dates () Columns ("A: A"). Select Dates () \u003d Application.transpose (Range (ActiveCell.column) .end (XLUP))) Dim Summa ( ) Columns ("B: B"). SELECT SUMMA \u003d Application.transpose (Range (ActiveCell, Cells (Rows.Count, ActiveCell.column) .end (XLUP))) Dim M AS Integer M \u003d Ubound (Dates) BP \u003d 30 CBP \u003d Round (365 / BP) Redim Days (M) for k \u003d 2 to m Days (k) \u003d Dates (k) - Dates (2) NEXT REDIM E (M) REDIM Q (M) for k \u003d 2 to MQ (k) \u003d Days (k) \\ bp e (k) \u003d (Days (k) MOD BP) / BP next i \u003d 0 x \u003d 1 x_m \u003d 0 s \u003d 0.000001 do while x\u003e 0 x_m \u003d xx \u003d 0 for k \u003d 2 to mx \u003d x + summa (k) / ((1 + e (k) * i) * ((1 + i) ^ q (k))) next i \u003d i + s loop if x\u003e x_m i \u003d i - s End If Psk \u003d Round (I * CBP, 5) Cells (3, 7) .Value \u003d PSK End Sub

The total cost of the loan (PSK) is one of the most important indicatorsThe definition of which allows to judge the financial costs of the borrower due to the loan agreement and arising from it. Moreover, if the bank is not complied with the calculation regulations or the borrower is not adequately informed about the PSK before the conclusion of the contract, this is considered by the violation of the requirements provided for by the law, which may entail his recognition invalid with the return of the borrower illegally retained amounts.

In the Russian banking practice, the term "full cost of the loan" has been applied since 2008, having come to replace the term "effective interest rate". The rules for calculating the PCC (formula and algorithm), as well as the conditions for use in relation to certain loan products are established by the Central Bank and law. They are subject to change, so if necessary, the PCC should always be referred to as relevant at the time of the calculation of regulatory and legal acts and take into account the date of concluding a loan agreement and its condition.

Currently, the so-called updated formula for calculating PSK is used.which appeared after making changes to the Consumer Lending Act. It approached the actual lending conditions and became more accurate, but the main thing - allowed the conditions of microloans more understandable and transparent to the population, in which huge interest and final cost of the loan were hidden under small daily accruals.

The concept of the full cost of the loan

The amount expressed as a percentage that the borrower has to be paid to repayment credit debt And for the service of the loan. Psk reflects the real expenses of the borrower associated with the loan, but includes only those payments, which are due to the appropriate execution and service of the loan and in compliance with the conditions specified in the loan agreement. It is for this reason that PSK does not take into account the costs associated with penalties, the execution of legislation requirements, such as, for example, the CTP, the Commission and the penalty, which depend on the actions of the borrower and leave him the right to choose - to go on such costs or not.

PSK should include amounts:

- principal debt and percent on it;

- commissions for registration and (or) issuance of a loan, opening and (or) maintenance of a loan (credit) account, the implementation of settlement operations on the loan, etc., if such payments are provided for;

- commissions for the issue and (or) service credit card;

- additional payments arising from the loan agreement, in particular those related to the liability insurance of the borrower, assessment and insurance of the pledge, notarized transaction.

Calculation of the PSK and its size must be given in the terms of the loan agreementAnd often published by the bank in advance in the information description of a specific credit product. Moreover, it is often on the bank's website or on other Internet resources, which publishes bank bids, provides for an online calculator for calculating PSK.

What gives the borrower himself the rate of PSK and his analysis? For the overwhelming majority of people, the importance represents the real amount of overpayment of the loan. For this, it is not necessary to count on its own. The annual percentage of PSK himself will clearly show how much overpayment will be based on the amount received in debt, interest, credit period and the applied debt repayment system (differentiated or annuity). Thus, it is easy to analyze the cost of different credit products and choose the one that will be more profitable. True, it should be noted that competent analysis involves a deeper understanding in the specifics of the calculation of the PCC and the content of the loan conditions. The full cost will give an idea of \u200b\u200bthe possible amount of overpayment, but it does not take into account, and it cannot take into account the situations in which the borrower will decide to repay the loan ahead of schedule, thereby reducing the amount of overpayment. In addition, the PCT itself does not allow to analyze how much a product will be beneficial qualitatively, and not quantitatively. Therefore, the Psk is a good, but not the only landmark when choosing a loan. Everything must be taken into account in the aggregate.

Calculation of PSK

Algorithm and formula for calculating PSK are united for all banks. However, given the fact that individual credit products (consumer, car loan, mortgage, etc.) have nuances in terms of compulsory inclusion in the calculation of specific parameters and the specifics of their formation, some individual features of the application of the algorithm and performing calculations are admissible. In any case, this should not affect the principles and rules of settlements provided for by regulatory legal acts.

Algorithm and formula for calculating PSK are united for all banks. However, given the fact that individual credit products (consumer, car loan, mortgage, etc.) have nuances in terms of compulsory inclusion in the calculation of specific parameters and the specifics of their formation, some individual features of the application of the algorithm and performing calculations are admissible. In any case, this should not affect the principles and rules of settlements provided for by regulatory legal acts.

To calculate the PSK, let's say, according to a consumer loan, it is necessary to be guided by the rules of Article 6 of the Consumer Loan Law. Here are also listed and requirements for informing the borrower on PSK and how to display the full cost of the loan under the terms of the contract. Requirements established for consumer loans are applied to microfinance organizations that are issued to the population's microloans. However, they do not apply to the mortgage - here you need to be guided by the acts of the Central Bank.

Given the need to have mathematical knowledge, an understanding of the specifics of algorithms and settlements of the PSK, current norms, the ability to analyze the terms of credit contracts, independent calculations - the laborious process. In addition, it is impossible to unconditional application of the provisions of laws in established rules Calculation of PSK, which does not provide access to the relevant acts (instructions, explanations, provisions) Central Bank. The need for this is also indicated in the laws themselves, where references are often used to the parameters and conditions established by the Bank of Russia. In this regard, the independent implementation of the settlements of the PSK almost none of the borrowers does or use the software, including online calculators that do not require understanding in the calculation algorithm.

To simplify the task, it is enough to refer to the conditions of your credit agreement. Banks are required to indicate the PSK in the contract, while it is assumed that their responsibility for informing the client they fulfilled this in full. In case of unreliability of information, the Bank or MFIs bear administrative responsibility, and the borrower has the right to claim the correct recalculation of the PSK, the return of illegally retained amounts and compensation for damages.

When analyzing the PSK, indicated in the consumer loan agreement (microloan), it is important to draw attention to ensuring that its size does not exceed more than 1/3 of the average value of the PCT, calculated by the Central Bank for the similar category of loans and the contract applied in the calendar quarter. However, by its decision, the Central Bank has the right to limit the application of this rule. This feature has already been used by the Bank of Russia in the first half of 2015. The average value of the PSK and restrictions on its use (if available) can be found on the website of the Central Bank of the Russian Federation or from other official sources.

Banks, private and state, are trying to bring clients with their credit proposals. For this reason, in advertisements, you can often see attractive loans rates, and in fact, overpays great amount. The total cost of the loan is a formula, the decoding of which includes in addition to the interest rate, all additional payments on consumer or any other loan.

What is the full cost of the loan

Taking advantage of the bank's offer to take money from him, you should always know that interest is just the payment for the use of money. In addition, there are additional commissions that also plunge on monthly payments. The whole amount of these components is called a complete interest rate. PSK, such an abbreviation of this indicator is the main importance to which it is necessary to focus when a loan is selected. Providing information about the value of the full cost loan is carried out in annual percent and is indicated in the upper right corner of the bank loan agreement.

The concept of an effective interest rate was previously applied. It was calculated by the formula complex interest, which included the incomplete income of the borrower from the possible investment of the amount of interest payments for the loan throughout the credit period under the same interest rate as the loan. For this reason, even in the absence of additional payments, the rate value was higher than the nominal. It did not reflect the real cost of the debt service borrower, as the Bank's client recognized only when it comes to pay for a loan.

Legal regulation

Seeing such a state of affairs, the central bank has become over the side of ordinary people and ordered all credit and financial institutions to convey to customers the full cost of the loan. In 2008, the Bank of Russia issued an indication "On the procedure for calculating and bringing to the borrower - individual full credit cost. " After the entry into force of the Federal Law "On Consumer Loan (Loan)", but it happened on July 1, 2014, the value of the total value of borrowed funds is determined depending on the subsidia-established central bank.

How to find out the price of a loan

It is noteworthy, but in microfinance companies, the full cost of the loan is always indicated, and all other payments concern only penalties and fines for the delay and non-fulfillment of obligations. In the bank, the main indicator is the interest rate for the use of a loan, additional payments that relate to the loan are indicated by individual items in the contract and additional agreements to it.

Notification of the full cost of the loan

Previously, the indicator of the PSK could be indicated in the contract, but the value there was spelled out by small font, which was not immediately in the eye. According to federal law A loan agreement is divided into 2 parts: general and individual conditions. So, in the second part, which has a tabular shape, the number of PCs is necessarily prescribed by the largest font that is applied when designing. An indication of the information is made in the frame, which should cover at least 5% of the area of \u200b\u200bthe entire sheet, on which individual credit conditions are prescribed.

What includes the full cost of the loan

The maximum possible value of the PCC should not exceed one third of the average indicator of the average value and is brought to the borrower in obligatory. In order to figure out where the total number of PSK follows from and why it may sometimes differ from the value in advertising or on the site credit organization, It is necessary to know all its components. These include:

- loan body and interest on it;

- fee for consideration of the application;

- commissions for issuing loan agreements and their issuance;

- interest for opening and annual account maintenance (loan) or credit card;

- the liability insurance of the borrower;

- assessment and insurance of pledge;

- voluntary insurance;

- notarial design.

What expenses do not increase the cost of the loan

In addition to the obligatory payments, which are included in the PCT, other payments may be charged from a lender, which do not affect the calculation of effective, i.e. Full bets:

- fee for failure to fulfill the contract. These include all sorts of fine and penalties, accrued due to the late payment of the next payment.

- voluntary payments. These include the Bank's Commission for early repayment of the loan, payment for extracting and references, restoring a lost credit card, etc.

- additional contributions. Here we are talking about payments that do not belong to the contract, but may be mandatory in connection with russian legislation (for example, the policy of OSAGO) or initiated by the loans themselves (additional insurance).

How to calculate the full cost of the loan

You can ask in the formula of the PSK before the conclusion of the contract in the Bank's Office. It must be submitted to the agreement before signing the agreement. You can calculate it and independently. However, in this case, it is necessary to carefully approach the calculation and not to miss a single moment, as this may lead to inaccuracies. Very often, the borrowers allow gross errors, inattentively reading the contract and skipping certain data.

Formula PSK.

The calculation of the full cost of the loan is made on the basis of the norms established by Central Bank Russia. The formula itself and the calculation algorithm are constantly being improved, therefore, independently determining the PCT, you need to seek the latest relevant data, which are published on the regulator's website. Last changes The methodology was produced in connection with the adoption of the Consumer Lending Act. The size of the PSK is calculated as follows:

Psk \u003d i × pbp × 100, where

Psk - the full cost of the loan, expressed as a percentage with an accuracy of the third mark after the comma;

ChbP - the number of basic periods throughout the calendar year (according to the Central Bank methodology one year is 365 days);

i is the percentage rate of the base period, which is expressed in decimal form.

(FORMULA)

Σ is Sigma, which means summation (in this formula - from the first payment to M-th).

DPK - the sum of the K th money payment under the contract. The amount of the loan provided to the borrower is made to the sign "-", and payments to return with the sign "+".

qK - the number of full base periods from the moment of issuing a loan to the date of the k-th payment.

eK - a deadline that is expressed in the shares of the base period, from the end of the QK-th base period to the date of the K-th payment. If the debt payment is carried out strictly according to the repayment schedule, the value will be zero. In this case, the formula has a simplified view.

m is the number of payments.

i - the percentage rate of the base period, expressed not in percent, and decimal form.

Algorithm of calculation

As can be seen from the calculation formula above, the loan rates are calculated simply, with the exception of the indicator referred to as the interest rate of the base period. This is the most complex indicator for calculating, not everyone can cope with. Calculate the same multi-year loans are physically unrealistic. To simplify calculations, you can contact online calculators or directly to the bank. In addition, if you think that the rate given in the contract is not accurate, you can send a copy of the contract to the Central Bank with a request to calculate the correct value.

Complete Cost Consumer Credit

Before concluding a consumer loan agreement, the Bank's employee is obliged to inform the loan real value Loan, which is often confused with the interest rate. Banks can impose payment of services, such as Internet banking or SMS notification, the fee for which is charged only with the permission of the borrower. The full cost includes not only the overpayment amount formed in connection with the accrued interest, but also the payment of the following operations:

- consideration of the application;

- issuing a loan;

- bank card issue;

- issuance of cash from the cashier;

- life insurance (optional).

Loan price when buying a car

By buying a car on credit, you should know that four sides are involved in the transaction. First, it is a buyer and a bank who credits the purchase, and secondly, the seller, which can be a car dealership or private person, and insurance Company. It is necessary to immediately say that car insurance on the CASCO system is obligatory if vehicle Transmitted to the bank as a collateral. Otherwise, the requirement to acquire the insurance policy is illegal.

The total cost of the credit on the car is calculated taking into account payments in the following positions:

- interest charges;

- commissions for transferring funds to the seller's account;

- pledge insurance;

- additional expenses of the borrower associated with the notarization of documents.

The cost of mortgage lending

It became easier to become the owner of own meters with the advent of the mortgage. Banks offer various lending options - with initial contribution Or without, with state subsidy or use maternal capital - All this will affect the full cost of the loan. In addition to paying interest to the PCD to buy real estate, add the following list of payments:

- insurance protection property (payments of the loan insurance loan to the subject of pledge are included in the calculation of the PSK in the amount proportional to the region of the real estate price paid by the loan, as well as the ratio of the period of lending and the term of insurance, if the term of borrowing is less than the term of insurance);

- property valuation;

- notarial design of the transaction;

- fee for registration mortgage loan and translation money On account.

All payments to third parties (notarial, insurance and other companies) are manufactured using the tariffs of these organizations. If the contract provides for the minimum monthly payment, the calculation of the full cost of the consumer loan occurs on the basis of this condition.

An example of calculating PSK.

- the main amount of the loan is 340,000 rubles;

- loan period - 24 months;

- the rate is 13% per annum;

- commission for the provision of a loan - 2.8% of the total;

- commission for issuing cash from the bank's office - 2.5%.

Below is a system with monthly uniform payments. The amount of interest accrued for the period will be 72414 rubles (it can be viewed in the contract or payment schedule).

Then calculate the amount of the Commission for issuing a loan and cashing:

340000 × 2.8% \u003d 9520 rubles;

340000 × 2.5% \u003d 8500 rubles.

After that, we summarize all the indicators and get:

340000 + 72414 + 9520 + 8500 \u003d 430434 ruble.

Online calculator

The network has a large number credit calculatorsthat will help calculate the PSK of standard loans, microloans and even overdrafts. However, it is necessary to understand that due to the fact that each bank has its own version of the bid, the data may differ. In addition, it is necessary to take into account the date of issuing a loan and repayment, and more ways to object to the amount of debt: annuity, differentiated or boblit.

Maximum and weighted average value of consumer loans

The Central Bank counts quarterly and publishes the average market value of the PSK different types consumer credits. The main thing that maximum rate The loan did not exceed the weighted average rate of more than a third. Below are values \u200b\u200bfor the 3rd quarter of 2019, taken from official sources:

The average values \u200b\u200bof the total value of consumer loans,% | Limit values \u200b\u200bof the full cost of consumer loans,% |

|

Consumer loans for the acquisition of vehicles with simultaneous transmission to pledge |

||

motor vehicles, the mileage of which is 0-1000 km | ||

motor vehicles, the mileage of which is more than 1000 km | ||

Consumer loans with a limit of borrowing (over the amount of limit borrowing on the day of signing the contract) |

||

30000-100000 p. | ||

100000-300000 p. | ||

Over 300000 p. | ||

Targeted consumer loans, which are issued through the transfer of credit funds by a trade and service company to the payment of goods (services), if there is a relevant agreement (POS credits) without ensuring |

||

30000-100000 p. | ||

Over 100000 p. | ||

More than a year: |

||

30000-100000 p. | ||

Over 100000 p. | ||

Neamed consumer loans, targeted consumer loans without collateral, consumer loans for refinancing of debt (except POS credits) |

||

30000-100000 p. | ||

100000-300000 p. | ||

Over 300000 p. | ||

More than a year: |

||

30000-100000 p. | ||

100000-300000 p. | ||

Over 300000 p. | ||

What gives the analysis of the PSK borrower

For most people to know the PSK - to understand it, how much will it cost them borrowed fundsbecause sometimes the loan by which only payment of interest is provided, in the end it will cost the same amount as the loan with a smaller interest rate, but with availability additional fees. This is even found in the same bank, and created in order to attract more customers. Receiving a loan agreement, where the PSK is specified, or independently calculating the indicator, it is necessary to understand that certain nuances may not always be taken into account, such as early repayment of the principal debt.

How to reduce loan cost

Having received information about the full cost of the loan, sometimes there is a desire to take money into debt. However, if you approach this issue with the mind, you can reduce the digit offered by the bank. For this, there are different number of ways:

- Early loan repayment. If partially or fully repayment is out of schedule, it will help reduce the credit load in the form of non-percent. However, you need to carefully read the contract for penalties, which, on the contrary, can make a loan expensive.

- Money issuance on bank card. Many lenders offer cash loans, but at the same time they do not advertise that they will have to pay a certain percentage for issuing them from the cash register. You can ask if there is the possibility of transferring money to existing map or an account (it can be discovered for free) and will be charged for it. Most likely, this option will be cheaper.

- Carefully read the terms of the loan agreement. Sometimes bank managers do not quite correctly, not declare additional contributions. In some cases, the agreement includes payments for SMS informing, voluntary life insurance, Internet bank and similar services. If you know that you do not need them - boldly refuse, thereby we will save money.

Video

Found in the text error? Highlight it, press Ctrl + Enter and we will fix everything!