In connection with the planned government of the Russian Federation transfer to international Standards financial statements (IFRS) of the entire Russian business by 2018, one of the actual accounting problems for this transitional period It is the development of a standard plan of IFRS accounts, which makes it possible to keep records, using both active and passive IFRS accounts and classical accounts of an account balance from the recommended account account account plan for Russian standards accounting (RAS).

In this paper, a variant of such a model plan of IFRS accounts is proposed. The basic basis for its development is the presence of the author and described in 2012 in its book: "Cherkay A. D. Theory of two rows of 4 accounts accounting and financial accounting. A single plan for accounting for IFRS and RAS "procedures for the unambiguous translation of RAS accounts, with accounting objects with defined under IFRS in accordance with paragraph 7 of PBU 1/2008" Accounting Policy of Organizations ", in IFRS accounts, and back, IFRS accounts in the accounts of the RAS. A feature of the proposed account plan is to provide them with a separate write of articles of non-financial and financial assets and obligations in the statement of financial position of the Organization (balance), which ensures the expansion and simplification of the analysis of financial reporting by interested users.

General view of IFRS accounts plan

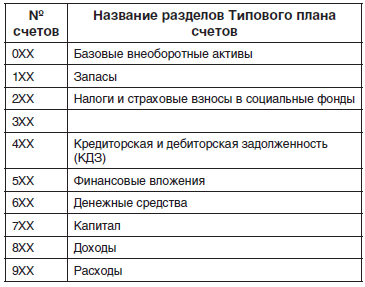

The general view of the IFRS account plan is presented in Table 1. The first five classes of accounts of the IFRS account plan have the same names as the first five sections of the financial statement (balance) of the organization. The names of these accounts in IFRS accounting usually coincide with the names of the statutes of the financial position report on which their final balance is recorded. Income and expenses accounts determine the financial results of the organization's activities. The submitted account plan has the classes of balance sheet accounts that correspond to the sections of the balance sheet in the RAS recorded in the order of increasing liquidity.Table 1.Chart of accounts IFRS

Perfect balance

An accounting balance with a separate entry of non-financial and financial assets and obligations is called by the ideal balance, the list and the procedure for writing subsections in its sections is presented in Table 2.Table 2.Perfect balance

| Sections | Subsections |

| 1.Wellular assets | Non-financial non-current assets |

| Financial outgoing assets | |

| 2. Coordinate assets | Non-financial reverse assets |

| Financial current assets | |

| 3.Kapital | |

| 4.long term duties | Non-financial long-term commitments |

| Financial long-term commitments | |

| 5.Short-term liabilities | Non-financial short-term obligations |

| Financial short-term commitments |

In the sections of its assets and obligations, non-financial articles are initially recorded, and then financial articles defined in accordance with paragraphs 11 and AG3-AG12 IAS 32 "Financial Instruments: Presentation of Information" (as amended on July 18, 2012), while:

the main feature of financial assets and liabilities is to carry out calculations of both monetary and other financial instruments, and the financial instruments themselves, as well as cash, are financial assets. physical assets (Such as stocks, fixed assets), as well as leased assets and intangible assets (such as patents and trademarks) are not financial assets. If the contract provides for work, services and material values, then this is a sign non-financial assets and obligations. obligations or short-term assets (such as taxes that arise as a result of the requirements prescribed by the law entered by the government) are not financial obligations or financial assets. IN Russian Federation This type of assets and obligations also include insurance contributions in social funds.

Typical plan of IFRS accounts corresponding to the ideal balance

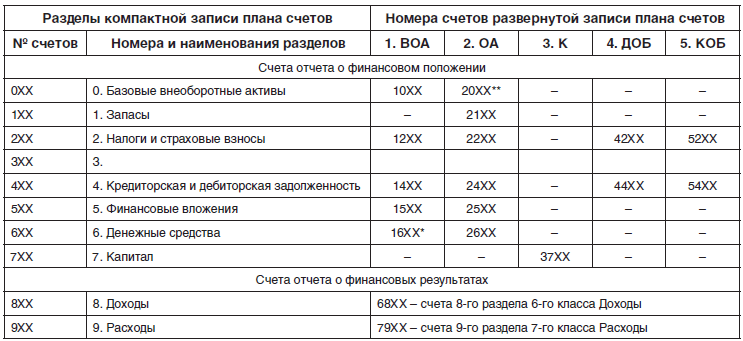

Since IFRS standards define the requirements for submitted financial statements, and not to the accounts plan and accounting rules, the IFRS account plan using only active and passive accounts is not mandatory. To the accounts of the IFRS account plan, which I can be with a balance variable, we require a requirement to comply with the articles of the ideal balance with providing the possibility of recording the amounts of bills of accounts in the articles of the ideal balance, with grouping them by the type of accounting objects in the order of increasing their liquidity.The structure of the standard IFRS accounting plan in a compact recording with a 3-s-numeration of accounts with an alternation of the balance, grouped into ten partitions, is presented in the left part of the table 3. In it, sections from zero on the 6th partitions of accounts are recorded in the order of liquidity increases. In the right-hand side, the structure of the expanded recording of a standard account plan with active and passive accounts with a 4-digital numbering received by the recording before the 3-digit number of the class number number is given. At the class "non-current assets" (VOI) 1, "Capital Assets" (OA) 2, "Capital" (K) 3, "Long-term liabilities" (DOD) 4, "short-term obligations" (COB) 5, "Revenues" 6 and "expenses" 7.

Table 3.The structure of the compact and deployed recording of the standard IFRS account plan

| Sections of a compact report of the plan of accounts of IFRS | Account numbers detachable account recording accounts | |||||

| Account number | Rooms and names Sections | 1.Wea | 2.Oa. | 3.k. | 4. | 5.Cob |

| Financial statement report | ||||||

| 0xx | 0. Basic non-current assets | 10xx | 20xx ** | ─ | ─ | ─ |

| 1xx | 1. Stocks | ─ | 21xx | ─ | ─ | ─ |

| 2xx | 2. Taxes and insurance premiums | 12xx | 22xx | ─ | 42xx | 52xx |

| 3xx | 3. | |||||

| 4xx | 4. Credit and receivables | 14xx | 24xx | ─ | 44xx | 54xx |

| 5xx | 5. Financial investments | 15xx | 25xx | ─ | ─ | ─ |

| 6xx | 6. Cash | 16xx * | 26xx | ─ | ─ | ─ |

| 7xx | 7. Capital | ─ | ─ | 37xx | ─ | ─ |

| Financial Results Accounts | ||||||

| 8xx | 8. Revenues | 68xx - account of the 8th section of the 6th grade income | ||||

| 9xx | 9. Costs | 79xx - account of the 9th section of the 7th grade costs | ||||

16xx * - Cash with restrictions in the class of accounts "non-current assets" and 20xx ** - Basic non-current assets intended for sale in the class of "Current assets".

Compact recording of a model plan of IFRS accounts

Table 4 presents a compact entry of the authorized pilot plan of IFRS accounts by the author. In the column 3 tables recorded the names of accounts, subaccounts and sections in which they enter. In column 1, there are 2-digit numbers of accounts of a standard account plan accounts from the recommended RAS account plan. In a column 2, the number of digits in the number of accounts is 3rms and in subaccount numbers, more than 3, and in column 4 in accounts, respectively, equal to the 4th and subaccounts more than 4. At the same time, the second and third digits in the 3rd and third and fourth digits in the 4-digit numbers of the accounts of the standard IFRS account plan in most cases coincide with the 2-digit numbers of the accounts of the recommended RAS account plan.For example, the "Goods" account with a 3-digit number 141 in the second column and the 4-digit number 2141 in the fourth column has an RSB number 41 presented in the first column of the line of this account.

Table 4.Typical accounts of IFRS accounts

| Account number | Typical accounts of IFRS accounts | Account number | |

RAS | IFRS with RAS. | IFRS | |

| 1 | 2 | 3 | 4 |

| 0. Basic non-current assets | |||

| 001 | Fixed assets (OS) | 1001, 2001 | |

| 01 | 0011 | Fixed assets | 10011 |

| 07 | 0017 | Installation equipment | 10017 |

| 08 / OS | 0018 | Investments in fixed assets | 10018 |

| 00181 | Construction in progress | 100181 | |

| 00189 | Other investments in fixed assets | 100189 | |

| 0019 | Other fixed assets | 10019 | |

| 002 | Depreciation and depreciation of fixed assets | 1002 | |

| 02 / OS | 0021 | Depreciation of fixed assets | 10021 |

| 02 / IS. | 0023 | Depreciation of investment property | 10023 |

| 00291 | Impairment of fixed assets | 100291 | |

| 00293 | Impairment of investment property | 100293 | |

| 003 | Investment property (IP) | 1003, 2003 | |

| 03 | 0033 | Investment property in the organization | 10033 |

| 08 / IS. | 0038 | Investment Investment Property | 10038 |

| 004 | Intangible assets (NMA) | 1004, 2004 | |

| 04 | 0041 | Intangible assets in the organization | 10041 |

| 08 / NMA | 0048 | Investments in intangible assets and development | 10048 |

| 0049 | Other intangible assets | 10049 | |

| 00491 | Results of research and development | 100491 | |

| 005 | Depreciation and depreciation intangible assets | 1005 | |

| 05 | 0054 | Depreciation of intangible assets | 10054 |

| 0056 | Depreciation Goodwill | 10056 | |

| 00594 | Impairment of intangible assets | 100594 | |

| 00596 | Impairment Goodwill | 100596 | |

| 006 | Goodwill | 1006 | |

| 11,01 / p, Ost | 011 | Biological assets (plants (P), main herd (OST)) | 1011 |

| 97 | 097 | Exploration and preparatory work | 1097 |

| 1. Stocks | |||

| 110 | Productive reserves | 2110 | |

| 10 | 111 | Raw materials | 2111 |

| 14 | 114 | Reserves for depreciation material values | 2114 |

| 15 | 115 | Preparation and acquisition of material values | 2115 |

| 16 | 116 | Deviations in the value of material values | 2116 |

| 119 | Other production reserves | 2119 | |

| 120 | Unfinished production | 2120 | |

| 20 | 121 | Primary production | 2121 |

| 21 | 122 | Semi-finished products own production | 2122 |

| 23 | 123 | Auxiliary production | 2123 |

| 25 / PST | 125 | Overhead (RSBU account 25 / Permanent (PST)) | 2125 |

| 128 | Marriage in production | 2128 | |

| 129 | Serving production and farm | 2129 | |

| 140 | Goods I. finished products for sale | 2140 | |

| 41 | 141 | Products | 2141 |

| 42 | 142 | Trading markup | 2142 |

| 43 | 143 | Finished products | 2143 |

| 45 | 145 | Goods shipped | 2145 |

| 46 | 146 | Performed steps in incomplete work | 2146 |

| 40 | 147 | Production (works, services) | 2147 |

| 190 | Other stocks | 2190 | |

| 2. Taxes and Insurance Contributions to Social Funds | |||

| 09 | 209 | Delay tax assets | 1209 |

| 19 | 219 | VAT on purchased assets | 2219 |

| 68 | 268 | KDZ on taxes | 2268,5268 |

| 69 | 269 | CDZ on insurance premiums | 2269,5269 |

| 77 | 277 | Delay tax obligations | 4277 |

| 3. | |||

| 4. Credit and receivables (KDZ) | |||

| 400 | Cdz | V400, V \u003d 1,2,4,5 | |

| 401 | KDZ with related parties | V401, V \u003d 1,2,4,5 | |

| 402 | Cdz with unrelated sides | V402, V \u003d 1,2,4,5 | |

| 60 | 460 | Suppliers and contractors | V460, V \u003d 1,2,4,5 |

| 76 / OA | 461 | Operating Rent (OA) | 2461, 5461 |

| 62 | 462 | Buyers and customers | V462, V \u003d 1,2,4,5 |

| 63 | 463 | Reserve for doubtful debts | 2463 |

| 66 | 466 | Short-term loans and loans | 5466 |

| 67 | 467 | Long-term loans and loans | 4467,5467 |

| 70 | 470 | Calculations | 2470,5470 |

| 71 | 471 | Accounting faces | 2571 |

| 73 | 473 | Other personnel operations | V473, V \u003d 1,2,4,5 |

| 75 | 475 | Participants and founders | 2475,5475 |

| 76 / F. | 476 | Financial Rental (Leasing) (FA) | V476, V \u003d 1,2,4,5 |

| 79 | 479 | Outdoor settlements | 2479,5479 |

| 480 | Other non-financial assets and obligations | V480, V \u003d 1,2,4,5 | |

| 490 | Other Financial Debt and Obligations | V490, V \u003d 1,2,4,5 | |

| 4901 | Notes for receipt | 14901,24901 | |

| 4902 | Interest to getting | 24902 | |

| 4903 | Bonds for payment | 4903 | |

| 4904 | Mortgages to pay | 4904 | |

| 4905 | Bill of exchange for payment | 44905,54905 | |

| 4906 | Account interest | 54906 | |

| 4907 | Pension Plan Obligations | 44907, 54907 | |

| 4908 | Actual reduction in the value of obligations | 44908 | |

| 4909 | Obligations intended for sale | 54909 | |

| 98 | 498 | revenue of the future periods | 4498 |

| 5. Financial investments | |||

| 58 | 558 | Financial investments | 1558, 2558 |

| 5581 | Investments in related parties | 15581 | |

| 55811 | Investing in subsidiaries | 155811 | |

| 55812 | Investments in associate organizations | 155812 | |

| 55813 | Investments in joint organizations | 155813 | |

| 5582 | Investments in unrelated side | 15582 | |

| 5583 | Financial investments held to repayment | 15583 | |

| 5584 | Financial investments held for trading | 15584, 25584 | |

| 5585 | Financial investments available for sale | 25585 | |

| 5586 | Loans and loans issued | 15586, 25586 | |

| 5587 | Long-term deposits on a simple partnership | 15587 | |

| 5588 | Deposits | 15588, 25588 | |

| 5589 | Other financial investments | 15589, 25589 | |

| 59 | 559 | Reserves for depreciation financial investments | 2559 |

| 6. Cash | |||

| 50 | 650 | Cashbox | 2650 |

| 51 | 651 | Settlements | 2651, 1651 |

| 52 | 652 | Currency accounts | 2652, 1652 |

| 55 | 655 | Special accounts in banks | 2655 |

| 57 | 657 | Translations on the way | 2657 |

| 659 | Other financial assets | 2659 | |

| 7. Capital | |||

| 80 | 780 | Authorized capital | 3780 |

| 81 | 781 | Own shares repurchased from shareholders | 3781 |

| 83 / Ed | 782 | Em session income (ED) | 3785 |

| 83 / R. | 783 | Reserves and other reserves (P) | 3783 |

| 84 | 784 | Undestributed profits ( uncoated loss) | 3784 |

| 86 | 786 | Special-purpose financing | 3786 |

| 787 | Profit and losses from currency broadcast | 3787 | |

| 788 | Profit and losses on pension plans | ||

| 99 | 799 | Profit and losses of the current year | 3799 |

| 8. Revenues | |||

| 90.1 | 810 | Income from the main activity | 6810 |

| 811 | Revenues from the sale of goods, products and services | 6811 | |

| 812 | Returns sold goods and discount suppliers | 6812 | |

| 814 | Revenues under construction contracts | 6814 | |

| 815 | Revenues in financial lease | 6815 | |

| 816 | Income by biological assets | 6816 | |

| 817 | Income on operations with financial instruments | 6817 | |

| 819 | Other income from the main activity | 6819 | |

| 91.1 | 820 | Income from minority | 6820 |

| 821 | Revenues from sales of other assets | 6821 | |

| 822 | Accounts from course differences | 6822 | |

| 823 | Revenues OT. participation in associates | 6823 | |

| 824 | Income from interest | 6824 | |

| 825 | Incomes for deferred taxes | 6825 | |

| 826 | Reversing loss from depreciation | 6826 | |

| 827 | Profit from change fair value | 6827 | |

| 829 | Other income from non-mining activities | 6829 | |

| 9. Costs | |||

| 90.2 | 910 | Costs for main activities | 7910 |

| 911 | Cost of goods sold, products and services | 7911 | |

| 44 | 912 | Expenditure on the sale of goods provided | 7912 |

| 26,25 / PC | 913 | General and administrative expenses | 7913 |

| 914 | Costs under construction contracts | 7914 | |

| 915 | Financial Rental Expenditures | 7915 | |

| 916 | Biological asset costs | 7916 | |

| 917 | Expenses for operations with financial instruments | 7917 | |

| 919 | Other expenses for the main activity | 7919 | |

| 91.2 | 920 | Costs for non-core activities | 7920 |

| 921 | Expenses for the disposal of other assets | 7921 | |

| 922 | Loss from exchange rate differences | 7922 | |

| 923 | Loss from equity participation in associated companies | 7923 | |

| 924 | Percentage expenses | 7924 | |

| 925 | Deferred taxes | 7925 | |

| 926 | Costs for the current income tax | 7926 | |

| 927 | Expenses for the reserve for doubtful debts | 7927 | |

| 928 | Losses from depreciation | 7928 | |

| 929 | Other expenses for non-core activities | 7929 | |

In the number of KDZ accounts with the V4XX numbers, the first letter V can take values \u200b\u200b1, 2, 4 and 5 (V \u003d 1, 2, 4, 5), respectively, when v \u003d 1, these accounts of long-term receivables non-current assets With 14xx numbers, with v \u003d 2, these are short-term accounts receivable accounts turnover assets with 24xx numbers, with v \u003d 3 these are long-term accounts accounts payable Long-term liabilities with 34xx numbers, with v \u003d 5, these are short-term accounts billing accounts for short-term liabilities with 54xx numbers.

We draw attention to the fact that in the currently entered part sections of the standard accounts plan, after non-financial partitions, an additional free section with the number 3 is included, which is intended to be transferred to it from the 4th section of the Balance of non-financial accounts of the KDZ to record them in the financial statement before Balance of financial accounts KDZ. For example, the sum of short-term accounts debt to buyers and customers after payment of the supply of goods reflected on the account with number 5462, refers to the non-financial balance sheet with number 5362, replacing the number 5462 second numbers from 4 to 3. Similarly, replacing the number 5466 of the account number 5466 Short-term loans and loans "At the number 4166 of the balance sheet item can be recorded the balance of these loans first in short-term balance liabilities, as traditionally accepted in the reporting on RAS.

Thus, the proposed sample schedule of IFRS accounts solves the task of separate recording of articles of non-financial and financial assets and obligations in the statement of financial position.

Chart of accounts IFRSAndrei Gershun Why do I need an IFRS bill plan?Unlike russian standardsInternational Financial Reporting Standards do not regulate how the billing plan should be. In particular, in the United States and Great Britain, each company can use its own account plan. In other countries, for example, in France, the plan of accounts, as in Russia, is standardized, and its application is required for all enterprises. Unlike the Russian account plan, French has a variable number of numbers in the account number. So, the account 21 is the fixed assets, and the account 281 is the accumulated depreciation of fixed assets. Example: French account plan (is partial) When building reporting in accordance with IFRS, you can use the Russian account plan. However, its structure was developed more than 50 years ago and with the time of creation lost its clarity for practicing accountants (remember how hard it is to fill in the balance and income statement based on this account plan). When moving to international standards, some CIS countries (Ukraine, Moldova, Kazakhstan and others) have changed account plans to simplify accountants to collect information and building financial statements in accordance with IFRS. Work on the new Russian plan of accounts is not yet completed, according to forecasts, it will be published no earlier than 2001. In the meantime, the company may draw up its account plan, which will ensure the convenient construction of financial statements under IFRS. |

Place the button on your website:

kurs.znate.ru.

kurs.znate.ru.

IAS account plan According to the materials of Article A. Gershun "Plan of Accounts of IFRS" asset

Sample IAS account plan *

* According to the article by A.German, "Plan of Accounts of IFRS"

ASSETS

1 FIXED ASSETS

11 INTANGIBLE ASSETS

111 Intangible assets

112 Depreciation of intangible assets

12 Long-term material assets

121 Land and real estate

122 wear land plots and real estate

123 Fixed assets

124 Depreciation of fixed assets

125 Natural resources

126 Exhaustion of Natural Resources

13 Long-term investments

131 Long-term investments in unrelated sides

132 Long-term investments in related parties

133 Changing the value of long-term investments

14 Deferred income tax assets

141 Defolation Affairs Tax Assets

15 OTHER NONCURRENT ASSETS

152 Long Term Receivables

153 Long-term advances issued

154 long-term expenses of future periods

155 Other long-term assets

2 Current assets

21 Inventory

211 Raw materials and materials

212 Unfinished production

213 Finished products

214 products

22 CONSTRUCTION IN PROGRESS

221 Inscribed construction under contracts

23 Short-term receivables

231 Calculations with customers

232 Reserve for doubtful debts

233 short-term receivables related parties

24 Other receivables and prepayment

241 Advances issued

242 expenses of future periods

243 Calculations with the budget

244 VAT for reimbursement

245 Calculations with accountable persons

246 Accrued revenues

247 loans issued

248 Other receivables

25 Short-term investments

251 short-term investments in unrelated side

252 short-term investments in related parties

253 Changing the cost of short-term investment

26 Cash and Equivalents

262 Settlement account

263 Currency account

264 Special accounts in banks

265 Money transfers on my way

27 Other current assets

272 Other current assets

Passive

3 EQUITY

31 Authorized and extension capital

311 Authorized capital

312 Emission revenue

313 Unpaid capital

314 Own Promotions

32 RESERVE CAPITAL

321 Revaluation of long-term assets

322 course differences in investment in subsidiaries

323 Subsidies to public enterprises

33 RETAINED EARNINGS

331 Retained earnings (loss) past years

332 Amend the results of past years

333 Net profit reporting year

334 announced dividends

4 LONG TERM DUTIES

41 Long-term financial obligations

411 Long-term loans

412 other long-term financial obligations

42 Deferred income tax obligations

421 Defolation of income tax obligations

43 Other long-term commitments

431 Long-term income of future periods

432 Long-term advances received

433 Other long-term accrued obligations

5 SHORT-TERM LIABILITIES

51 Short-term financial obligations

511 Short-term loans

512 Current share of long-term liabilities

513 Other short-term financial obligations

52 Short-term payable debt

521 Calculations with suppliers

522 short-term liabilities related parties

53 Short-term accrued obligations

531 Payroll Calculations

532 Calculations with accountable persons

533 tax calculations

534 Calculations with founders

535 percent accrued for payment

536 reserves of upcoming expenses and payments

54 Other short-term commitments

541 Short-term advances received

542 current income of future periods

543 Other short-term commitments

Operating accounts

6 Revenues

61 Revenues from sales

611 Revenues from the sale of finished products

612 Revenues from the sale of goods

613 Revenues from Services

64 Other operating income

641 Revenues from the implementation of current assets

642 Income from the current rental

643 income in the form of fines and penalties

644 Revenues from the change of the method of assessing current assets

645 Revenues from Reimbursement Losses

646 Other operating income

65 Income from investment activities

651 Revenues from the disposal of intangible assets

652 Revenues from the disposal of long-term material assets

653 Revenues from the disposal of long-term financial assets

654 Dividends received

655 percent obtained

656 Revenues from related parties

657 Other income from investment activities

66 Financial revenues

661 royalty

662 Lease Revenues

663 revenues from gratuitous assets

664 Grant Revenues

665 Accounts from course differences

666 Other financial revenues

68 Emergency revenues

681 compensation obtained for damages from natural disasters

682 other extraordinary income

7 COSTS

71 Cost of sales

711 Cost of completed products

712 Cost of goods sold

713 Cost of services rendered

72 Commercial expenses

721 Marketing Costs

723 package costs

724 Sales Costs

725 Warranty repair

726 costs for doubtful debts

727 Return and price reduction costs

728 Other Commercial Expenses

73 General and administrative expenses

731 Depreciation of fixed assets

732 Amortization of intangible assets

733 Salary of Admistrative and Economic Staff

734 Social deductions

735 taxes, fees and payments (except for income tax)

736 Professional services

737 Executive and Travel Costs

738 Office expenses, communication costs

739 Other general and administrative expenses

74 Other operating expenses

741 Expenses for the implementation of current assets

742 Current Rental Costs

743 Costs for fines and pencils

744 Costs from changes to current assessment methods

745 Expenses for interest on loans and loans

746 Unallocated indirect production costs

747 shortages and losses

748 Other operating expenses

75 Investment costs

751 Costs for the disposal of intangible assets

752 Expenses for the disposal of long-term material assets

753 Costs for the disposal of long-term financial assets

754 Costs for operations with related parties

755 Other Investment Costs

76 Financial expenses

761 Royalty Free

762 Leasing Costs

763 Course Course Differences

764 Other Financial Expenses

77 Profit tax costs

771 income tax

78 Emergency losses

781 Disaster losses

782 Other Emergency Expenses

8 Account account accounts

81 Direct material costs

811 consumption of raw materials and materials

82 Direct labor costs

821 Direct labor costs

822 Social contributions

83 Direct overhead production costs

831 Overhead Production Costs

84 Indirect production costs

841 Wear, repair and maintenance

842 Amortization of intangible assets

843 Salary of Management and Personnel

844 Social deductions

845 Travel Costs

846 Other Indirect Production Costs

85 Other accounts accounting accounts

851 other accounts accounting accounts

9 Wash balances

AND.

A. Slobodnyak Tests Collection and Tasks on International Standards Financial Report

Collection of tests

Test tasks and tasks for the accounting of individual types of assets and revenues of the organization are given in accordance with the requirements of international financial statements.

Introduction (142)

Public report

The main instrumentaries of accounting reform in Russia are international financial reporting standards. The concept of the development of accounting and reporting on the medium term defined the provisions

Theoretical foundations of international financial statements as a system

Public report

Protection will be held in 2009 in 1515 at the meeting of the dissertation council D501.001.18 at Moscow State University them. M.V. Lomonosov at: 11 2, Moscow, GSP-2, Vorobyov Mountains, Moscow State University.

Discipline program "International Financial Reporting Standards" Direction 080500. 62 "Management"

Discipline program

The real program of academic discipline establishes the minimum requirements for the knowledge and skills of the student and determines the content and types of training sessions and reporting.

Educational and methodical complex Work curriculum for students of the specialty 08. 01.

09 "Accounting, Analysis and Audit"

Training and metodology complex

O.A. Kuzmenko. International Accounting Standards and Financial Reporting: Educational and Methodical Complex. Work curriculum for students of the specialty 08.

Other similar documents ..

Selection of the most important documents on request Chart of accounts IFRS (Regulatory acts, forms, articles, expert advice and much more).

Tax Guide.

Practical manual for annual accounting reporting - 2017neer assets can be checked for impairment in the manner determined by international financial statements (pb. 22 PBU 14/2007). The procedure for reflection in the accounting records of losses from impairment of NMA facilities was not established by PBU 14/2007, nor the instructions for the application of the account plan nor other regulatory acts of the Russian Federation for accounting. According to paragraph 59, 61 of IFRS (IAS) 36 impairment loss is the reduction of the carrying amount of the asset to its recoverable value and this decrease is shown in the report on financial results (If the asset was not previously completed). How should it be reduced book value NMA, the standard does not specify. The logic of building a table 1.1 In the example of the design of the explanation to the accounting balance and the report on the financial results proposed by the Ministry of Finance of Russia, it is implied to reflect the impairment loss from the impairment of NMA with a constant value of the initial (current market) value.

Article: Features of reforming accounting of insurance activities

(Koltakova I.A.)

("Financial Bulletin: Finance, Taxes, Insurance, Accounting", 2016, N 3) The author reviewed some of the features of the transition of insurance organizations to a new account of accounting accounts and it is shown that the application of the new account plan, industry accounting standards and international financial standards Reporting will lead to an increase in accounting analytics and reporting transparency and will contribute to attracting investments, including foreign ones to the Russian insurance market.

The document is available: in the commercial version ConsultantPlus

We continue the cycle of articles on international financial statements. The focus of this material is the bill plan used when conducting registration under IFRS.

Immediately let's say, unlike Russian standards, international financial reporting standards do not regulate what the account plan should be. Consequently, the company that maintains and makes accounting financial statements in accordance with IFRS, can develop and use an account plan, which is different from the plan of accounts of other companies. In other words, the International Account Plan is developed by the company independently, without any pointer from above. In Russia, as is well known, the bill plan is regulated by the Order of the Ministry of Finance of Russia of October 31, 2000 No. 94n. And although it is a recommendatory nature, in practice, most companies use it almost unchanged.

So, consider how an exemplary plan of the company's accounts that constitutes reporting under IFRS will look, and compare it with the Russian analogue. At the same time, we note that we can keep accounting for international standards, using the Russian account plan, but expanding it for IFRS purposes.

General rules Building International Account Plan

When building an account plan according to IFRS, it is necessary to remember that it should:

Ensure simple compilation of the main financial reports (first of all accounting balance and income statement);

Be so flexible to be able to expand in the future due to the change in the company's structure or business;

Provide sufficient detail to build management reports.

To simplify the filling of financial reports, the plan of accounts usually constitutes such a principle. In the first part of the billing plan, all balance sheet accounts are listed (the so-called regular accounts) in the order in which they are specified in the balance sheet report: assets, capital, obligations. And in the second part indicate the accounts of profits and losses ("temporary accounts", which open at the beginning of the fiscal year and are closed at the end). Note that the international standards themselves do not establish the procedure for transferring balance sheet items, but only regulate which information should be disclosed in the balance sheet.

With such a construction plan, an account of the accounting balance sheet and the Company's profit and loss statement can be obtained immediately after the printing of the operating station or trial balance. It should be noted that such a board has built plans for the majority of European companies.

As a rule, articles are listed in an increase in liquidity (which is similar to Russian practice). At the same time, the bills in international accounting have a numerical designation containing not two signs (as in Russia), but, for example, five, six or even 20. Often, some general accounts are introduced, which will never contain data in monetary terms. An example is the score of "non-current assets", which will fall into the balance only as the name of the corresponding partition, and the specific values \u200b\u200bwill be reflected according to the relevant articles within this section. Such an approach is uncharacteristic for Russian accounting.

We also note some other discrepancies. Western accounting practice allows several accounts to participate in the wiring (several bills debit and credit), whereas in Russia, the wiring has a rigidly specified view - the debit of the account ... a credit of the account ... In this case, all financial reports according to IFRS are constructed in such a way that they are operated only with incoming and outgoing, as well as rolled turns (without sharing them on debit and credit).

Thus, each account of the international account plan is either active or passive. Active passive accounts, such as an analogue of the Russian account 76 "Calculations with different debtors and creditors", are absent. Instead of the account in international Practice Several accounts are used. Another example: Russian account 90 "Sales" in Western accounting corresponds to individual accounts "Revenues from Sales" and "Sales Cost".

All this leads to the fact that the billing plan necessary to build reporting in accordance with IFRS, usually contains from 100 to 300 accounts and subaccounts.

Example of account plan according to IFRS

In accordance with the above principles, the International Account Plan can be built, for example, so (the approximate sample is shown on page 1, on page 2, on page 3, on page 4):

1xxx - non-current assets;

2xxx - reverse assets;

3xxx - capital;

4xxx - long-term obligations;

5xxx - short-term obligations;

6xxx - income;

7xxx - expenses;

8xxx - account accounting accounts;

9xxx - off-balance accounts.

Accounts beginning with 1, 2, 3, 4 and 5 are balance sheet accounts and are arranged in the manner repeating the balance sheet report on IFRS. Accounts beginning with 6 and 7 are income and expenses accounts. Accounts starting with Figures 8 are temporary accounts designed to collect analytical information when taking into account production costs. In fact, they fulfill the role of accounts section III "The costs of production" of the Russian account plan. At the end of the reporting period, they close to the accounts of unfinished production and finished products. Finally, the accounts starting with the figures 9 are.

It is possible to list income and expenses accounts in the order in which they are specified in the income statement. In this case, the bill plan in part of temporary accounts could look like this:

61xx - revenues from sales;

62xx - the cost of implementation;

71xx - commercial and administrative costs;

72xx - other incomes;

73xx - other expenses;

74xx - income tax;

75xx - extraordinary profit and losses.

As you know, the structure russian plan Accounts looks somewhat different.

International Financial Reporting Standards (IFRS) is a set of international accounting standards, which indicates how specific types of operations and other events should be reflected in the financial statements. IFRS is published by the Council on International Financial Reporting Standards, and they define accurately, as accountants must lead and present accounts. IFRS were created in order to have a "common language" of accounting, because business standards and accounting may differ from both the company and the country to the country.

The purpose of IFRS is to maintain stability and transparency in the financial world. This allows enterprises and individual investors to take qualified financial decisions, as they can see exactly what is happening with the company in which they want to invest.

IFRS are standard in many parts of the world, including the European Union and many countries of Asia and South America, but not in the United States. Commission for securities Both Exchange (SEC) is in the process of making decisions on adopting standards in America. Countries that most win from standards are those that lead international business and invest in it. Experts suggest that the global introduction of IFRS will save money on alternative comparative costs, and will also allow you to more freely transmit information.

In countries that adopted IFRS, both companies and investors benefit from this system, since investors are more likely to invest in the company, if the company's business practice is transparent. In addition, the cost of investments is usually lower. Companies that are conducted by international business are most benefit from IFRS.

IFRS standards

Below is a list of applicable IFRS standards:

| Conceptual Fundamentals of Financial Reporting | |

|---|---|

| IAS 1 | Representation of financial statements |

| IFRS / IAS 2 | Stocks |

| IFRS / IAS 7 | |

| IFRS / IAS 8 | Accounting Policy, Changes in accounting estimates and errors |

| IAS 10 | Events after the end of the reporting period |

| IFRS / IAS 12 | Profit taxes |

| IFRS / IAS 16 | Fixed assets |

| IFRS / IAS 17 | Rent |

| IFRS / IAS 19 | Remuneration workers |

| IAS 20 | Accounting for state subsidies, disclosure of information on state aid |

| IFRS / IAS 21 | The impact of currency exchange rates |

| IFRS / IAS 23 | Costs of loans |

| IFRS / IAS 24 | Disclosure of related parties |

| IFRS / IAS 26 | Accounting and reporting on pension plans |

| IFRS / IAS 27 | Separate financial statements |

| IFRS / IAS 28 | Investments in associate and joint ventures |

| IFRS / IAS 29 | Financial statements in the hyperinflation economy |

| IAS 32 | Financial Tools: Information Presentation |

| IFRS / IAS 33 | Profit per share |

| IFRS / IAS 34 | Intermediate financial statements |

| IAS 36 | Impairment of assets |

| IAS 37 | Reserves subject obligations and conditional assets |

| IFRS / IAS 38 | Intangible assets |

| IFRS / IAS 40 | Investment property |

| IAS 41 | Agriculture |

| IFRS / IFRS 1 | First use of IFRS |

| IFRS 2 | Stocks based on shares |

| IFRS 3 | Business associations |

| IFRS 4 | Insurance contracts |

| IFRS / IFRS 5 | Long-term assets intended for sale and terminated activities |

| IFRS 6 | Intelligence and Assessment of mineral reserves |

| IFRS 7 | Financial Instruments: Information Disclosure |

| IFRS / IFRS 8 | Operating segments |

| IFRS / IFRS 9 | Financial instruments |

| IFRS 10 | Consolidated financial statements |

| IFRS 11 | Team work |

| IFRS 12 | Disclosure of information on participation in other enterprises |

| IFRS 13 | Estimation of fair value |

| IFRS 14 | Accounts deferred tariff differences |

| IFRS / IFRS 15 | Revenue under contracts with buyers |

| SICS / IFRICS | Decisions on the interpretation of standards |

| IFRS for small and medium enterprises |

Representation of financial statements in accordance with IFRS

IFRS covers a wide range of accounting operations. There are certain aspects of business practices for which IFRS establishes compulsory rules. The basics of IFRS are elements of financial statements, the principles of IFRS and types of basic reports.

Elements of financial statements in accordance with IFRS: assets, obligations, capital, income and expenses.

Principles of IFRS

Fundamental principles of IFRS:

- the principle of accrual. In accordance with this principle, events are reflected in the period when they occurred, regardless of movement money.

- the principle of continuity of activity that implies that the company will continue to work in the near future, and the leadership does not have plans or the need to turn the activity.

Reporting in accordance with IFRS should contain 4 reports:

Financial Statement: It is also called Balance. IFRS affects how the components of the balance are interconnected.

Cumulative income report: This may be one form, or it can be divided into a report on the profits and losses of IFRS and other income report, including property and equipment.

Capital Change Report: Also known as a report on retained profits. It reflects changes in profit for this financial period.

Cash Movement Report: This report summarizes the financial transactions of the company for this period, while cash flows We are divided into flows on operating activities, investment and financing. Recommendations for this report are contained in IFRS 7.

In addition to these basic reports, the company must also submit applications with a summary of its accounting Policy. A full report is often considered in comparison with the previous report to show changes in the profit and loss. The parent company should create separate reports for each of its subsidiaries, as well as the consolidated financial statements of IFRS.

Comparison of IFRS and American Standards Standards (GAAP)

There are differences between IFRS and generally accepted accounting standards of other countries that affect the calculation financial relationship. For example, IFRS is not as strict when determining revenues and allow companies to report income faster, therefore, therefore, the balance within this system can show a higher flow of income. IFRS also have other costs of expenses: for example, if the company spends money on developing or investing for the future, it does not have to show them as a consumption (that is, they can be capitalized).

Another difference between IFRS and the GAAP is to determine the order of accounting. There are two ways to track stocks: FIFO and LIFO. FIFO means that the latest unit of reserves remains non-sold before selling previous stocks. LIFO means that the latest unit of stock will be sold first. IFRS prohibits LIFO, while American and other standards allow participants to use them freely.

History of IFRS

IFRS arose B. European Union With the intention to spread them on the whole continent. The idea quickly spread throughout the world, since the "common language" of financial statements made it possible to expand links around the world. The United States has not yet adopted IFRS, as many consider the American OPAP as a "gold standard". However, since IFRS becomes a more global norm, the situation may change if SEC decides that IFRS is suitable for American investment practice.

Currently, about 120 countries are used by IFRS, and 90 of them require that the reporting companies are fully presented in accordance with the requirements of IFRS.

IFRS is supported by the IFRS Foundation. IFRS Foundation Mission - "Provide transparency, accountability and effectiveness on financial markets around the world". The IFRS Foundation (IFRS) not only provides and monitors financial statements, but also makes various offers and recommendations to those deviate from practical recommendations.

The purpose of the transition to IFRS is the maximum simplification of international comparisons. It is difficult, because each country has its own set of rules. For example, US GAAP differs from Canadian GAAP. Synchronization of accounting standards around the world is a continuous process in the international accounting community.

Transformation of financial statements in accordance with IFRS

One of the main methods for the preparation of financial statements in accordance with the requirements of IFRS is a transformation.

The main stages of the transformation of financial statements in accordance with IFRS:

- Development of accounting policies;

- Selection of functional currency and representation currency;

- Calculation of the initial balance sheets;

- Development of a transformation model;

- Assessment of the company's corporate structure in order to identify subsidiaries, associated, affiliate and joint ventures included in accounting;

- Identifying the company's business features and collecting information necessary to calculate the transformation adjustments;

- Rearrangement and reclassification of financial reports on national standards to IFRS.

Automation of IFRS

The transformation of the financial statements of IFRS in practice is difficult to submit without automation it. There are various programs on 1C platform, which allow you to automate this process. One of these solutions is "WA: Financier". In our solution, there is an opportunity to broadcast accounting data, mapping on the accounts of the IFRS accounts plan, to make various adjustments and reclassification, to eliminate intragroup revolutions in consolidating reporting. In addition, 4 main reports of IFRS are configured:

Fragment of the financial status report of IFRS in "WA: Financier": Bookmark IFRS "Fixed assets".

In connection with the introduction of international financial statements in Russia, one of the actual accounting problems for this transition period is to develop a standard accounting plan for IFRS accounting, simplifying the transition from accounting on RAS to accounting under IFRS. This paper offers a model plan for IFRS accounting accounts, which allows you to record under IFRS, using both active and passive accounts of IFRS and classical accounts of the RAS - active, passive, and bills with alternating balance, and simplifies the transformation of reporting on RAS Reporting under IFRS.

In accordance with the plan of the Ministry of Finance of the Russian Federation for 2012-2015 on the development of accounting and reporting in the Russian Federation on the basis of international financial reporting standards (approved by the Order of the Ministry of Finance of Russia dated November 30, 2011 No. 440 as amended on November 30, 2012) Development and preparations for the approval of projects of new federal accounting standards based on IFRS are underway. The base for solving these issues is that international financial statements are enacted in Russia, and since 2013 they are applied by organizations identified Federal law dated July 27, 2010 No. 208-FZ "On the consolidated financial statements", to prepare, along with reporting on RAS and IFRS reporting. At the same time, most of these organizations are accounting for RAS, and then the reporting transformation drawn up on RAS in IFRS reporting.

In connection with the widespread transition to IFRS planned by 2018, it is necessary to simplify this transition. This issue is the easiest to solve this issue by developing such an IFRS account plan, which provides the possibility of keeping accounting for IFRS, using not only active and passive accounts of IFRS, but also classic active, passive and accounts with alternating balance used in the RAS, determination of accounting objects on which Currently, it is already possible using IFRS. This is possible because in accordance with paragraph 7 of PBU 1/2008 "Accounting Policy of Organizations" "When forming an accounting policy of the Organization on a specific issue of organizing and conducting accounting, a choice of one method is made from several, allowed by the legislation of the Russian Federation and (or) regulatory legal legal Accounting acts. If on a specific issue in regulatory legal acts, accounting methods have not been established, then in the formation of accounting policies, the organization of the relevant method is being developed, based on these and other accounting provisions, as well as international financial reporting standards. At the same time, other accounting provisions are used to develop an appropriate method in terms of similar or related facts of economic activity, definitions, the conditions for recognizing and the procedure for assessing assets, liabilities, income and expenses. "

In the works of the author, it is given to the justification of the possibility of transition from IFRS accounts to the accounts of the RAS with the objects of accounting defined on IFRS and back from the RAS accounts to the accounts of IFRS, and the example of the working plan of IFRS accounts is deciding the task under consideration. On the basis of these results, it was developed, submitted in this paper, a variant of the standard IFRS account plan, which makes it possible to record under IFRS both using IFRS accounts and using RAS accounts without changing their numbering and grouping, but with accounting objects to them defined under IFRS . This is expanding the possibilities of using the current accounting software for Russian firms to keep registering under IFRS, simplifies the entire process of accounting and preparation of reporting under IFRS russian accountantsAs well as an understanding of interested Russian and foreign users thus prepared reporting.

IFRS requirements for the balance structure. Types of MSFO Accounts Plans

Although this is not determined by the requirements of international financial statements standards, the IFRS account plans to record the names of the balance sheets and their sections that coincide with the name of articles and sections of the report of the financial situation used by the enterprise - balance, and the list and names of the income accounts and expenses of the IFRS accounts plan to determine In accordance with the report on financial results. Both reports must meet the requirements of the IAS standard 1 "Representation of Financial Reporting". Thus, the basis for the development of IFRS billing plans is the implementation of the IFRS requirement to reports on the financial status and financial results of the enterprise.

According to clause 60 of the IAS standard 1 "Representation of financial statements", "the enterprise must submit in its statement of financially short-term and long-term assets, as well as short-term and long-term obligations as separate sections in accordance with paragraphs 66-76, except Cases when providing information based on the degree of liquidity provides reliable and more appropriate information. " In practice, accountants seek to carry out both requirements of paragraph 60 of the IAS 1 standard, with the selected manner of liquidity in the balance sheet not only sections, but also articles in them.

Since in paragraph 60 of IAS 1 is not exactly indicated in what order of short-term or long-term assets (obligations) are recorded in the financial position of the enterprise, as well as to submit information (according to the degree of increasing or decrease in liquidity), then the requirements of IFRS meet two types of balance . In the first (i) assets are arranged in order from less liquid to more liquid (initially non-current assets, then turnover assets), then the Capital section and the obligations in order to reduce the maturity of obligations (first the long-term, then short-term). In the second (ii) assets are arranged in order from more liquid to less liquid (initially current assets, then non-current assets), then commitments in the order of increasing the repayment of obligations (first short-term, then long-term) and the partition of capital.

The consequence of this is the use of two main types of IFRS account plans, the record of which is presented in Table 1 in the form corresponding to the two types described above under IFRS.

The numbering of the first seven account classes, allows the first digit of the four-digit number of each account to establish whether the account is active or passive.

Table 1

Two basic types of IFRS bills plans

Balance accounts (accounts corresponding to the articles of a financial statement), beginning with figures 1 and 2, are active, and accounts beginning with figures 3, 4 and 5 - passive. Scores that starting the number 6 are passive income accounts, and the number 7 - active (counter-grade) expenses used in the preparation of a report on financial results.

For example, in the Republic of Kazakhstan in 2006, a typical plan of second-type IFRS invoices was introduced, with active and passive accounts, located in order to reduce the liquidity of assets and an increase in the maturity of obligations.

In the Russian Federation, the assets are traditionally located in the statement of financial position in accordance with the procedure from less liquid to more liquid and liabilities with a decrease in their maturity. It complies with the plan of the first-type IFRS accounts and the author's support plan of IFRS (type I) accounts with active, passive and variable accounts.

We draw attention to the fact that in terms of accounts of IFRS account accounting accounts may not be allocated to a separate account class, as this is presented in the second type in Table 1. This simply builds a more detailed account plan with accounting accounts within other main account classes. .

Sections of a model plan of IFRS accounts with alternation accounts

In accordance with the requirements of paragraph 54 of IAS (IAS), 1 "Representation of Financial Reporting" determined the minimum list of articles of the financial statement report, which is proposed to streamline and expand with the division of non-financial and financial articles Assets and obligations of the balance and their grouping on the type of accounting objects and the degree of their liquidity. The use of this approach allowed to propose to write a model plan of IFRS accounts with the allocation of ten partitions presented in Table 2. These sections included an additional section with the number 3. It is intended to highlight and write to the article of this section of the non-financial part of the balance of the balance of non-financial accounts accounts and receivables and accounts of other non-financial assets and obligations from section 4.

The model plan of IFRS invoices with its proposed sections can be recorded, both in Table 2 (in compact form with accounts active, passive and accounts with variable balance) and in the deployed form with accounts only active and passive, as presented in the right In the table 3 of the table 3 of the left, the structure of the compact IFRS account plan is presented, and the structure of the expanded standard IFRS account plan is shown in the right side of this table, as well as the mutual compliance of the accounts of the first of their form, reflected in the left side of the table 3, and the second Their species presented in the right-hand side of Table 3, and vice versa.

table 2

Sections of the standard IFRS account plan

The accounts of the compact standard accounting plan of IFRS accounts have a three-digit numbering represented in columns 1 of tables 2 and 3, passing into four-digit when recording in the expanded form of a standard account plan, the structure of which is presented in Table 1 and in the right-hand side of Table 3 with Balance Claim classes "non-current assets "(VO)," Redeems "(OA)," Capital "(K)," Long-term liabilities "(DOD) and" short-term obligations "(COB). In the class of accounts "Revenues" records the accounts of the income section, in the class of accounts "expenses" of the account of the section "Expenditures".

Classes of accounting accounts and off-balances in this work are not discussed. Note that the four-digit numbers of accounts in the right-hand side of Table 3 allow from a compact view of a standard account plan to obtain its deployed entry with only active and passive IFRS accounts. Using specific four-digit, the numbers of which are given later in Table 4, and without specifying account numbers - in generalized form in Tables 1 and 3. In this case, in the four-digit account numbers, the first digits of their classes are practically signs of subaccount recorded in front of three-digit account numbers and characterizing the section Balance in which the sums of their balance should be recorded.

Table 3.

The structure of the compact and deployed recording of the standard IFRS account plan

16xx * - cash accounts with restrictions in the class of accounts "non-current assets", 20x ** - accounts of basic non-current assets intended for sale in the class of accounts "Current assets".

Table 4 presents a compact entry of the IFRS-proposed model plan with the accounts with variable variables. In the column 3 tables recorded the names of accounts, subaccounts and partitions in which they enter. In the left part of it in column 1, two-digit numbers of accounts of a standard account plan of accounts from the recommended plan of RAS accounts are given, and the column 2 shows the three-digit numbers of IFRS via variables and with three and large numbers of numbers of their subaccounts. On the right side of Table 4 in column 4, two-digit numbers of the easiest perspective encoding of accounts are shown, and four-digit numbers of IFRS accounts and four and large numbers of numbers of their subaccounts are recorded in the fifth column, allowing their class number by the first digit of their class be recorded in the balance sheet. At the same time, the numbers and names of the partitions and accounts are recorded in bold, and the numbers and the names of the subaccounts are recorded by ordinary font.

Table 4.

Compact recording of the standard IFRS account plan with alternation accounts

Note that in the second column, the second and third digits, and in the fifth column, the third and fourth digits of account numbers and subaccounts in most cases coincide with two-digit numbers of the recommended account plan for RAS from the first column. For example, the account "Goods" with a three-digit number 141 in the second column and four-digit number 2141 in the fifth column has an RAS number 41 presented in the first column of the line of this account, the "deferred tax assets" account with a three-digit number 209 in the second column and four-digit number 1209 In the fifth column, it has an RAS number 09 in the first column of the line of this account, the account "VAT, on acquired values" with a three-digit number 219 and four-digit number 2219 in the fifth column in the second column number 19 in the first column of the line of this account, and etc. Since objects in terms of accounts are defined by IFRS, this rule is not always performed. For example, in the account of IFRS "Fixed assets", along with fixed assets under RAS, included equipment for installation, as well as investments in fixed assets from investments in non-current assets in the RAS. Therefore, the score of IFRS "Fixed Tools" with the number 010 does not correspond to the RAS account with the number 01, and we introduced a subaccount "Fixed assets in the organization" with number 011, the corresponding account 01 "Fixed assets" on RAS. A similar situation takes place with other accounts from the section "Basic non-current assets".

Note that in accounting on the RAS part of the accounts has a number with the last digit equal to zero (0), for example, 10 "Materials", 20 "Basic Production", 40 "Production (works, services) and others. In the proposed plan of IFRS accounts with three-digit numbers, accounts 110 "Production reserves" are recorded, with a number 120 "unfinished production", with a number 140 "goods and finished products for sale." Therefore, in these and in a number of other cases, there is a deviation in the numbering of the last two digits of three-digit accounts and four-digit accounts of the standard IFRS account plan from two-digit numbers of the RAS account plan. But in all cases where it is possible, and this is not observed in most cases such deviations. In the fourth column, the bills plan recorded double-digit account numbers that do not have these shortcomings, and on their database, more compact and convenient recording of IFRS account numbers, both with accounts with alternate balance, and only with active and passive accounts can be recorded.

We note that in the deployed recording of a model plan of the IFRS accounts of Table 4, in its non-current assets, current assets, capital, long-term obligations and short-term account obligations of the first seven balance sheets of a compact standard account plan are found several times. For example, accounts with three-digit numbers of the 5xx "Financial Investments" section from a compact account of account account accounts in the deployed recording are found twice. They can be long-term financial investments with numbers 15xx and belong to the class of non-current assets, and may also be short-term financial investments with 25xx numbers and belong to the class of current assets. The unified recording of two numbers of 15xx accounts and 25xx is carried out in the form of U5XX, where the first letterv says that the first figure of these rooms is variable (according to the first letter of the word variable - "variable").

In this case, the accounts with the V5XX numbers with V \u003d 1, 2 (with V equal to 1 or 2) accounts of financial investments, and at the same time, with v \u003d 1, these accounts of long-term financial investments of non-current assets with a number 15xx, and at V \u003d 2 - is Accounts of short-term financial investments of current assets with a number 25xx. In other accounts - accounts of payables and receivables (KDZ) with V4XX numbers The first letter V can take values \u200b\u200b1, 2, 4 and 5 (V \u003d 1, 2, 4, 5), respectively, with v \u003d 1, these accounts of long-term receivables The debt of non-current assets with 14xx numbers, with v \u003d 2, these accounts of short-term receivables of current assets with numbers 24xx, with V \u003d 3, these accounts of long-term accounts payable long-term liabilities with numbers 34xx, with v \u003d 5, these are the short-term accounts accounts for short-term liabilities with numbers 14xx.

Note that for keeping accounting, the recording of invoices with the first digit indicating what class does a specific account relates is not mandatory, since this figure does not determine the object of accounting, but simply where it will be reflected in the reporting, in which section of the Financial Report - balance or in which line of the report on financial results will reflect the balance of the account, and, accordingly, what is the expense of active or passive. Therefore, the first digit with an indication of the class class is almost to account a sign of the number of its subaccount, but not recorded after the account number, but before it. Since the IFRS standards contain reporting requirements, and not to the rules of accounting and used at the same time, the accounts, as in classical account on Pachet and in accounting for RAS, accounting for IFRS can be used by alternating balance, and not Only active and passive accounts. It is important that the accounting objects for them are determined in accordance with the requirements of IFRS, which is already in accounting for the RAS, in accordance with paragraph 7 of PBU 1/2008 "Accounting Policy of Organizations", which we are supposed to when using the standard accounting plan proposed in this work IFRS with accounts with alternation balance. At the same time, along with other requirements and features of IFRS accounting, this requirement should be reflected in the approved "organization accounting policy".

It should be noted that the author offered by the author a model plan of IFRS invoices simply ensures the fulfillment of IFRS requirements when preparing a statement of financial position. In balance and in terms of accounts, IFRS adopted non-financial articles of advances issued by suppliers of goods, works and services, to record separately before financial segments of receivables, and non-financial articles on the advances received from buyers and customers are accepted to record payable bills before financial accounts. Since it makes sense for certain accounts of the calculation to share them on non-financial and financial it makes sense in the preparation of the balance, then it is not worth doing this in advance. Therefore, we have not carried out such a division in the type of accounts.

For a separate entry in the balance sheet of non-financial and financial groups Articles by creditor I. receivables We include a spare free section of accounts with the number 3. The presence of free numbers of the third section of the accounts allows you to simply reflect the balance of non-financial accounts and receivables accounts and other non-financial assets recorded in the account plan in the section 4 in terms of Non-financial articles of balance debtations, while changing them the second digit of the four-digit number 4 to number 3, and thereby writing their balance in the balance before the balance of accounts of the Financial Devit Group. For example, reflecting short-term accounts debt to buyers and customers of goods, works, services on the account with four-digit number 5462 after payment of the supply of goods, the balance on this account in the balance sheet may refer to the article with the number 5362, which, being an article of non-financial short-term obligations, will settle In the balance sheet in the article by financial debt to suppliers and contractors, whose number, like at the account of payables, before suppliers and contractors will be 5460.

As B. accounting balance RSB reporting Traditionally, the "borrowed funds" articles are taken to record the first in section 4 "long-term liabilities" and section 5 "short-term obligations" of the balance sheet, then when using the proposed schedule of IFRS accounts, this task is solved by replacing the four-digit number 5466 of the "short-term loans and loans" IFRS accounts on the number 5166 of the balance sheet, and the account number 5467 of the short-term parts of the account "Long-term loans and loans" is replaced by the number 5167 of the balance sheet. The number of 4467 of the long-term account "Long-term loans and loans" is replaced by the number 4167 of the balance sheet.

In general, it should be noted that, if necessary, it also does not cause special difficulties to conduct further detail of the considered account plan, as well as the recording of a model plan of IFRS accounts only with active and passive accounts when using four-digit account numbers from the fifth column of Table 3.

Bibliography

- The plan of the Ministry of Finance of the Russian Federation for 2012-2015 on the development of accounting and reporting in the Russian Federation on the basis of international financial statements, approved by the Order of the Ministry of Finance of Russia dated November 30, 2011 No. 440, as amended on November 30, 2012. // URL: http://www.minfin.ru/common/img/uploaded/library/2012/12/ plan_po_razvitiu_bu_ na_osnove_msfo.pdf.

- Model accounting account plan in accordance with international financial reporting standards. Recommended for the application by the Expert Council of the Ministry of Finance of the Republic of Kazakhstan on accounting and auditing issues according to the Protocol of January 24, 2005 No. 1. // URL: http://kazbook.narod.ru/knigi/buh/buh.htm.

- Sukharev I. R. The importance of the introduction of IFRS in Russia / I. R. Sukharev // Accounting. -2012. - Number 3. - P. 7-11.

- Cherkay A.D. Theory of two rows of four accounts accounting and financial accounting. Unified Accounting Plan for IFRS and RAS. - M.: 2012. - 120 s.

- Cherkay A.D. Accounting and financial accounting - business language for managers. IFRS, US GAAP, RAS: the theory of two rows of 4 bills, new balance equations and linguistic metering models. - M.: 2013. - 120 s.

- Cherkay A.D. On the possibility of developing a single plan of accounts of IFRS and RAS / A. D. Cherkai // Accounting. - 2013. - №5. - P. 113-116.

- Cherkay A.D. A single universal account plan for maintaining parallel accounting for IFRS and RAS / A. D. Cherkai // Financial newspaper. - 2013. - №17-18. - P. 7-8. // URL: http://fingazeta.ru/discuss/50624/.

- Shadilova S.N. Accounting Policy features in the accounting and reporting system in accordance with international financial statements. / Shadilova S.N. // All for Accountant -2014. - №3 - p. 14-18.