Description of the presentation by individual slides:

1 slide

Slide description:

2 slide

Slide description:

Goals and objectives Goals: Expand knowledge of bank cards and the safety of their use Uncover technical methods of fraud Objectives: Obtain information about bank cards Study ways to protect bank cards Study technical methods of fraud

3 slide

Slide description:

Bank card Bank card (eng. Bank Card, BCard, BC) - a plastic card linked to one or more bank accounts; a tool that allows you to access your personal bank account. Used to pay for goods and services, including via the Internet, as well as withdraw cash.

4 slide

Slide description:

Rules for safe card use To avoid the use of your card by another person, keep the PIN code separately from the card, do not write the PIN code on the card, do not share the PIN code with other people (including relatives), do not enter the PIN code when working online Internet To avoid fraud using your card, require transactions with it only in your presence, do not allow the card to be taken out of your sight

5 slide

Slide description:

Rules for safe use of a bank card If you have been contacted by phone, on the Internet, through social networks or other methods, and under various pretexts they are trying to find out your bank card details, passwords or other personal information, be careful: these are clear signs of fraud. If you have any doubts, we recommend that you stop communicating and contact the bank by phone number indicated on the back of your bank card. Do not listen to the advice of third parties, and do not accept their help when carrying out transactions. If necessary, contact employees at a bank branch or call the numbers indicated on the device or on the back of your card

6 slide

Slide description:

Rules for safe use of a bank card Destroy receipts with passwords from Internet banking systems if you do not plan to use them. Do not transfer checks to third parties, incl. bank employees Keep your card out of reach of others. Do not give the card to another person, except the seller (cashier). It is recommended to store the card separately from cash and documents, especially when traveling

Slide 7

Slide description:

Fraud Fraud is the theft of someone else's property or the acquisition of rights to someone else's property through deception or abuse of trust. A person who does this is called a fraudster or fraudster.

8 slide

Slide description:

Main types of fraud with bank cards Theft of bank cards Technical tricks Copying card data Theft using viruses Phantom ATM Scotch method Impact on the psyche Technical tricks Skimming Letters and calls from scammers Phishing

Slide 9

Slide description:

Theft of bank cards Theft is the most common method of fraud. Your wallet was stolen, and there are several of your cards in it, including credit cards. If all cards have a chip, then the criminal will need to know the PIN code, without which you cannot pay for goods in a store, and you cannot withdraw money from an ATM. If there is an old-style card, you can cash it in the store by purchasing any product.

10 slide

Slide description:

Technical tricks. Copying card data by service workers The seller or waiter rolls your card through a special miniature hand-held skimmer. The PIN code or other card details are easily recorded on a video camera, after which a clone of your card is also made and money is withdrawn from it.

11 slide

Slide description:

Theft with the help of viruses A very dangerous type of technically advanced fraud, when a smartphone or computer is “infected” with a virus program, for example, a Trojan (details in the article). This is such a smart “digital pest” that it can not only corrupt data on your computer or “steal” valuable information, but also act on behalf of the owner of the phone (and more will happen!).

12 slide

Slide description:

Theft using viruses For example, you installed some free program from GooglePlay on your Android, and along with it a virus entered your smartphone. Your phone number is linked to the card, i.e. The mobile banking service is connected to your phone. So, a Trojan that you accidentally installed can use SMS banking commands to find out your balance, send an SMS command to transfer from your card to another, and independently respond with an SMS to a message confirming the operation. Moreover, the owner of the smartphone may not see any signs of activity, the virus will simply hide them from him, or he will see them, but it will be too late.

Slide 13

Slide description:

Phantom ATM Instead of a real ATM, scammers can build a plastic frame with a skimmer built into it. From the card inserted into the card reader, all the necessary information for its subsequent cashing can be read, and at the same time, the attackers will find out your PIN code typed on the “pseudo-keyboard”. Alternatively, the ATM may swallow the card altogether and not return the card.

Slide 14

Slide description:

Scotch method A person approaches an ATM, wanting to withdraw money from his card, inserts the card into the card reader and enters the PIN code on the keyboard. A characteristic rustling sound is heard from the dispenser, but for some reason no money is visible. The person “writes it off” to a malfunction of the ATM, shrugs, takes out his card and goes to another ATM. What's the result? The money was indeed withdrawn from the card and even the ATM dispensed it, but in reality it was stuck to double-sided tape stuck in the dispenser by the fraudster, who will take the money out for you.

15 slide

Slide description:

Letters and calls from scammers A typical example of SMS fraud is receiving an SMS message from a supposed bank number about blocking funds on your card due to an attempt to gain unauthorized access to them, with a recommendation to call the number provided in this message. Over the phone you will be informed that to unlock money on the card account you need to provide its details: card number, full name, expiration date and a three-digit secret code on the back of the plastic (CVV/CVC).

16 slide

Slide description:

Letters and calls from scammers Thus, the unlucky card holder, in order to save his money, transfers all the important data - he is not given time to think and analyze the situation, which is the calculation of cunning attackers. Moreover, the scammers will also ask you to dictate the password that was sent to the victim’s cell phone (and this is the same one-time password with which they need to confirm the operation of transferring money from the attacked card). If a person is not blind, then in the SMS he receives he will see a phrase about the inadmissibility of transferring the one-time password to an outsider. But he will read this only later, when he realizes that a decent amount has been taken from his card account.

Slide 17

Slide description:

Phishing A very common type of fraud, when, for example, an Internet user is “slipped” to a pseudo-site of his Internet bank, very similar to the original, on which they will try to fish out (catch) his card data by any means. Hence the name of this method of fraud, translated from English. "fishing" is fishing. The main thing is that a person goes to a fake site and believes that he is on the original resource. A link to such fake sites may contain, for example, an email from a fraudster, made in a standard banking form (colors, logo, etc.), and the text will encourage you to click on it, scaring you of possible problems with money in your card accounts. At the same time, the names of such sites are similar in appearance, but still differ slightly. Find, for example, the differences between the original name of the site sberbank.ru and the pseudo-site sbepbank.ru. The differences are not so easy for the “inexperienced” eye to notice.

18 slide

By clicking on the "Download archive" button, you will download the file you need completely free of charge.

Before downloading this file, think about those good essays, tests, term papers, dissertations, articles and other documents that are lying unclaimed on your computer. This is your work, it should participate in the development of society and benefit people. Find these works and submit them to the knowledge base.

We and all students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

To download an archive with a document, enter a five-digit number in the field below and click the "Download archive" button

Similar documents

Plastic card is a form of non-cash payment. Cards with magnetic stripe and smart cards. Comparative characteristics of magnetic cards and memory cards. National system "Belkart". The process of paying with plastic cards, the reasons for banning transactions with them.

abstract, added 04/29/2009

Aspects of operations of commercial banks with plastic cards. Payment system and its participants. Analysis of passive and active operations, compliance with economic standards of a commercial bank, financial results and transactions with plastic cards.

thesis, added 06/12/2009

Concept and types of plastic cards. Regulatory regulation of operations with plastic cards. Analysis of transactions with bank cards of OJSC VTB. Foreign experience in using plastic cards. Plastic cards in conditions of economic instability.

thesis, added 08/16/2010

Classification and types of bank cards. The current state of the banking system of the Russian Federation. Organization of transactions with plastic cards at OJSC "Northern Credit". Improving the system of transactions with plastic cards in Russia.

thesis, added 11/19/2014

Essence, meaning, classification of bank cards. Legal regulation of banks' work with bank cards. Comparative analysis of the organization of work with plastic cards by VTB 24 Bank (CJSC) and other banks in the Kostroma region.

thesis, added 09/11/2014

History of the development of plastic cards, their modern types. Features of the functioning of the payment system using plastic cards. Analysis of bank operations based on plastic cards. Functioning of a unified universal settlement network.

thesis, added 09/18/2012

The concept of a banking product. Principles of working with plastic cards. Analysis of services provided by the bank for individuals and legal entities. Prospects for improving operational and cash services in commercial banks of the Russian Federation.

thesis, added 06/02/2014

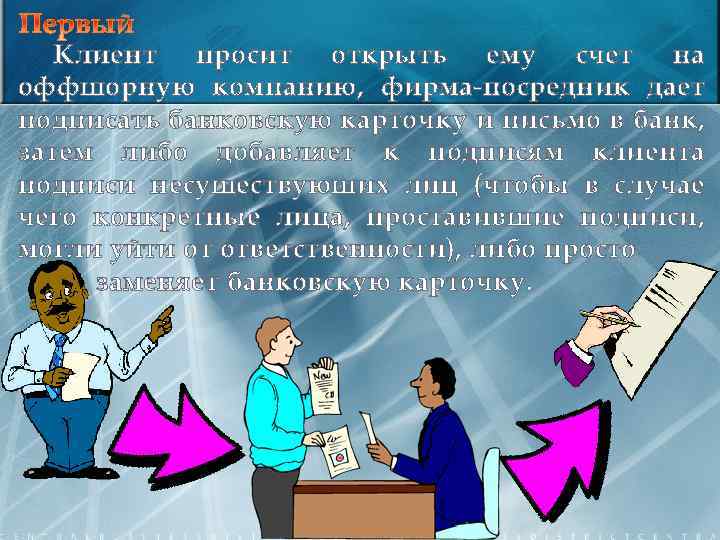

The client asks to open an account for an offshore company, the intermediary company gives him to sign a bank card and a letter to the bank, then either adds signatures of non-existent persons to the client’s signatures (so that in case of something specific persons who signed the signatures can evade responsibility), or simply replaces bank card.

The client asks to open an account for an offshore company, the intermediary company gives him to sign a bank card and a letter to the bank, then either adds signatures of non-existent persons to the client’s signatures (so that in case of something specific persons who signed the signatures can evade responsibility), or simply replaces bank card.

After the money arrives in the account, the bank receives an order to transfer it somewhere to an offshore account controlled by the scammers. Another scenario is that fraudsters periodically check with the bank about the account balance and transfer money only at the moment when a large amount has accumulated there.

After the money arrives in the account, the bank receives an order to transfer it somewhere to an offshore account controlled by the scammers. Another scenario is that fraudsters periodically check with the bank about the account balance and transfer money only at the moment when a large amount has accumulated there.

The second type of fraud is that the intermediary sells the client an offshore company at a very favorable price and at the same time very unobtrusively offers to open an account for it in a certain bank. The bank may have a very respectable name; its name may even almost duplicate the name of a well-known international bank (for example, Barclayes Bank instead of Barclays; the example is fictitious).

The second type of fraud is that the intermediary sells the client an offshore company at a very favorable price and at the same time very unobtrusively offers to open an account for it in a certain bank. The bank may have a very respectable name; its name may even almost duplicate the name of a well-known international bank (for example, Barclayes Bank instead of Barclays; the example is fictitious).

The client will be told that it is now very difficult for a Russian client to open an account in an internationally renowned bank, but this bank, on the contrary, loves Russian clients. It is also possible that interest rates will be promised higher than those offered by other banks, for example 7 -15%). The details of this bank will finally lull the client’s vigilance: he can have correspondent accounts in Switzerland, the USA and other seemingly reliable places.

The client will be told that it is now very difficult for a Russian client to open an account in an internationally renowned bank, but this bank, on the contrary, loves Russian clients. It is also possible that interest rates will be promised higher than those offered by other banks, for example 7 -15%). The details of this bank will finally lull the client’s vigilance: he can have correspondent accounts in Switzerland, the USA and other seemingly reliable places.

(As for the place of registration of the bank, they will most likely lie to the client, saying that the bank is registered in the country where he has a correspondent account (for example, Switzerland). As you guessed, in fact, the bank is not Swiss, but the cheapest offshore bank - for example, from Nauru (the cost of creation is 20-25 thousand dollars). And the owners of this bank are the owners of the company that offers offshore companies.

(As for the place of registration of the bank, they will most likely lie to the client, saying that the bank is registered in the country where he has a correspondent account (for example, Switzerland). As you guessed, in fact, the bank is not Swiss, but the cheapest offshore bank - for example, from Nauru (the cost of creation is 20-25 thousand dollars). And the owners of this bank are the owners of the company that offers offshore companies.

The first is that the bank owners will “spend” the client’s money in risky projects, hoping to both save the money and earn high interest rates. You can guess the fate of most of these projects. Secondly, the scammers will simply run away with the money. Be careful - this scam is very, very popular.

The first is that the bank owners will “spend” the client’s money in risky projects, hoping to both save the money and earn high interest rates. You can guess the fate of most of these projects. Secondly, the scammers will simply run away with the money. Be careful - this scam is very, very popular.

How bank management managed to steal money from company accounts. HERE IS A SIMPLE CLIENT MONEY MOVEMENT SCHEME:

How bank management managed to steal money from company accounts. HERE IS A SIMPLE CLIENT MONEY MOVEMENT SCHEME:

1. The client brings a payment receipt to the bank, with which he “instructs” the bank to transfer money from his account to the recipient’s account; 2. The bank operator (accountant) checks the correctness of the order, the correspondence of the signature of the top officials of the client company with the sample signatures on the bank card, the correspondence of the client’s seal with the sample seal on the same bank card, the presence of the transferred amount in the client’s account and, if all signs match and the correct execution of the payment order includes this operation in the list of bank transfers;

1. The client brings a payment receipt to the bank, with which he “instructs” the bank to transfer money from his account to the recipient’s account; 2. The bank operator (accountant) checks the correctness of the order, the correspondence of the signature of the top officials of the client company with the sample signatures on the bank card, the correspondence of the client’s seal with the sample seal on the same bank card, the presence of the transferred amount in the client’s account and, if all signs match and the correct execution of the payment order includes this operation in the list of bank transfers;

3. On one of the copies of the payment order (which remains with the client and is stored in his accounting archive), the bank operator puts the stamp “Paid” and formally from this moment the payment receipt for the client is considered completed, and the money is transferred to the recipient; 4. The bank manager (or his deputy) authorizes a banking transaction several times a day and the money (or rather, information about the fact of its transfer) goes through computer networks to the bank (banks) - the recipients of the money. 5. A paper notification of the fact of the transfer of money arrives at the recipient bank and at the recipient enterprise 7-10 days after processing the payment order.

3. On one of the copies of the payment order (which remains with the client and is stored in his accounting archive), the bank operator puts the stamp “Paid” and formally from this moment the payment receipt for the client is considered completed, and the money is transferred to the recipient; 4. The bank manager (or his deputy) authorizes a banking transaction several times a day and the money (or rather, information about the fact of its transfer) goes through computer networks to the bank (banks) - the recipients of the money. 5. A paper notification of the fact of the transfer of money arrives at the recipient bank and at the recipient enterprise 7-10 days after processing the payment order.

This is the ideal scheme for a simple banking transaction for transferring money. What needs to be changed so that the client receives confirmation of payment, money is debited from the client’s account, but does not actually end up in the recipient’s account?

This is the ideal scheme for a simple banking transaction for transferring money. What needs to be changed so that the client receives confirmation of payment, money is debited from the client’s account, but does not actually end up in the recipient’s account?

Probably, point 4 of our process should have looked like this: 4. 1. A certain specialist (or specialists) looks through the list of transfers and breaks it into two categories:

Probably, point 4 of our process should have looked like this: 4. 1. A certain specialist (or specialists) looks through the list of transfers and breaks it into two categories:

-the first category is money that cannot be ignored (this is, first of all, transfers to the account of the tax inspectorate, pension and other funds for payment of energy resources). Failure to receive money into the accounts of these recipients can lead to the rapid detection of the scam and the cessation of the scammers’ activities; -the second category is money that can be “lost” and that neither the recipient nor (even more so) the payer will look for immediately. These are, in particular, payments to housing organizations (DEZs and REUs), which, generally speaking, are extremely negligent in confirming the regularity of the facts of payment/non-payment of their clients.

-the first category is money that cannot be ignored (this is, first of all, transfers to the account of the tax inspectorate, pension and other funds for payment of energy resources). Failure to receive money into the accounts of these recipients can lead to the rapid detection of the scam and the cessation of the scammers’ activities; -the second category is money that can be “lost” and that neither the recipient nor (even more so) the payer will look for immediately. These are, in particular, payments to housing organizations (DEZs and REUs), which, generally speaking, are extremely negligent in confirming the regularity of the facts of payment/non-payment of their clients.

4. 2. Money from the list of “second category” accounts was withdrawn from these accounts and transferred (?), cashed (?), converted (?), exported (?) to distant countries? It is quite difficult to develop such a procedure, much less to carry it out in real banking practice, unless we assume the existence of a prior conspiracy among the bank’s top management and the presence of a trusted specialist, presumably in the computer service

4. 2. Money from the list of “second category” accounts was withdrawn from these accounts and transferred (?), cashed (?), converted (?), exported (?) to distant countries? It is quite difficult to develop such a procedure, much less to carry it out in real banking practice, unless we assume the existence of a prior conspiracy among the bank’s top management and the presence of a trusted specialist, presumably in the computer service

Fraudsters staged a masquerade for bankers. Real masquerades were staged for bankers by scammers who passed off the poor as successful managers and businessmen. The show was necessary to obtain large loans. Finding people who had neither property nor a stable income was not particularly difficult for swindlers.

Fraudsters staged a masquerade for bankers. Real masquerades were staged for bankers by scammers who passed off the poor as successful managers and businessmen. The show was necessary to obtain large loans. Finding people who had neither property nor a stable income was not particularly difficult for swindlers.

The scammers explained to the poor that they could not get a loan on their own, but were willing to pay interest for the services to obtain it. The guarantors were also selected using the same scheme. During the interviews, the scammers dressed borrowers in stylish suits, gave them certificates about their supposed salaries, and explained how to behave in the bank. Working off the promised fee, Muscovites received loans and gave them to benefactors. As a rule, these were amounts from 10 to 15 thousand dollars. When it was time to pay, the bankers

The scammers explained to the poor that they could not get a loan on their own, but were willing to pay interest for the services to obtain it. The guarantors were also selected using the same scheme. During the interviews, the scammers dressed borrowers in stylish suits, gave them certificates about their supposed salaries, and explained how to behave in the bank. Working off the promised fee, Muscovites received loans and gave them to benefactors. As a rule, these were amounts from 10 to 15 thousand dollars. When it was time to pay, the bankers

unexpectedly they found out that their clients were in fact insolvent. Moreover, such simpletons had no apartments, cars, or other property to compensate for the bank's losses. For a long time it was not possible to find the real recipients of the money. The scammers acted too cautiously. Nevertheless, on the eve of the weekend, when the swindlers staged another masquerade, they were caught in one of the central offices of a large bank. As it turned out later, this office was a favorite among scammers. Only here they carried out their scam 4 times.

unexpectedly they found out that their clients were in fact insolvent. Moreover, such simpletons had no apartments, cars, or other property to compensate for the bank's losses. For a long time it was not possible to find the real recipients of the money. The scammers acted too cautiously. Nevertheless, on the eve of the weekend, when the swindlers staged another masquerade, they were caught in one of the central offices of a large bank. As it turned out later, this office was a favorite among scammers. Only here they carried out their scam 4 times.

"Mirror bills" Several organizations at different times purchased bills issued by Bank "X". At the time of purchasing the bills, they checked their authenticity. Moreover, the authenticity of the papers was confirmed by the issuer himself (that is, the bank that issued these bills). However, when the organizations presented the bills for payment, the issuer refused to accept them, stating that they had already been repaid. The bank that issued these bills even provided documents confirming payment of exactly the same bills.

"Mirror bills" Several organizations at different times purchased bills issued by Bank "X". At the time of purchasing the bills, they checked their authenticity. Moreover, the authenticity of the papers was confirmed by the issuer himself (that is, the bank that issued these bills). However, when the organizations presented the bills for payment, the issuer refused to accept them, stating that they had already been repaid. The bank that issued these bills even provided documents confirming payment of exactly the same bills.

They could not answer the question of whether the bills were genuine or the examinations carried out. The forms were recognized as genuine, but there is no exact conclusion regarding the signatures on the bills. It became clear that the “mirror bills” were produced in the same printing house in which the forms of the bank’s real bills of exchange are printed. It is unlikely that they will be able to force the issuer to pay, because it is very difficult to prove that the bank itself is involved in issuing counterfeits. Usually at this stage of verification the case “hangs.”

They could not answer the question of whether the bills were genuine or the examinations carried out. The forms were recognized as genuine, but there is no exact conclusion regarding the signatures on the bills. It became clear that the “mirror bills” were produced in the same printing house in which the forms of the bank’s real bills of exchange are printed. It is unlikely that they will be able to force the issuer to pay, because it is very difficult to prove that the bank itself is involved in issuing counterfeits. Usually at this stage of verification the case “hangs.”

One Company purchased a bill of exchange from the company to which it was drawn. However, the problem is that now they cannot find this company. Another organization has been sitting at her address for a long time.

One Company purchased a bill of exchange from the company to which it was drawn. However, the problem is that now they cannot find this company. Another organization has been sitting at her address for a long time.

Many users received emails asking them to confirm their banking details on a special web page due to alleged technical problems.

Many users received emails asking them to confirm their banking details on a special web page due to alleged technical problems.

An example is an email sent to CITIBANK customers with the subject line “Important Fraud Alert from Citibank.” The message itself states that in order to carry out an operation aimed at detecting illegal banking activities, users need to check the correctness of their details on a special website.

An example is an email sent to CITIBANK customers with the subject line “Important Fraud Alert from Citibank.” The message itself states that in order to carry out an operation aimed at detecting illegal banking activities, users need to check the correctness of their details on a special website.

Panda Software warns that all these messages are falsifications, their main purpose is to obtain confidential information about the client (account numbers, user names, passwords, PIN codes and other secret data). The messages sent were carefully crafted in HTML to resemble the original online banking messages as closely as possible. Fake emails use the yet unpatched URLSpoof vulnerability in the Microsoft Internet Explorer browser. This hole causes the user to think that the web page they are accessing via a link from an email is an official banking site, when in fact it is just an exact copy of the original located on a different server.

Panda Software warns that all these messages are falsifications, their main purpose is to obtain confidential information about the client (account numbers, user names, passwords, PIN codes and other secret data). The messages sent were carefully crafted in HTML to resemble the original online banking messages as closely as possible. Fake emails use the yet unpatched URLSpoof vulnerability in the Microsoft Internet Explorer browser. This hole causes the user to think that the web page they are accessing via a link from an email is an official banking site, when in fact it is just an exact copy of the original located on a different server.

If the user enters the requested data, it will fall straight into the hands of the scammer who created this letter and web page. This type of online scam involves using fake emails, pop-ups and websites.

If the user enters the requested data, it will fall straight into the hands of the scammer who created this letter and web page. This type of online scam involves using fake emails, pop-ups and websites.

In the banking industry, abuse by staff is a fairly common phenomenon. World practice shows that abuses occur much more often in small banks than in large ones. This is primarily due to the combination of several positions in small banks by one person, which makes it possible to commit theft as a cashier, and then hide it as an accountant.

In the banking industry, abuse by staff is a fairly common phenomenon. World practice shows that abuses occur much more often in small banks than in large ones. This is primarily due to the combination of several positions in small banks by one person, which makes it possible to commit theft as a cashier, and then hide it as an accountant.

Most domestic banks are small by world standards. In addition, domestic business is now going through a stage of high criminalization and small banks are more easily influenced by criminal structures or even created by them. It is quite common for clients (“scammers”) to take out a loan in advance without intending to repay it. Bank employees, who have low wages by world standards, are often bribed. There are many “pocket” banks that are focused on serving their founders. Such founders are often given virtually free loans and the repayment of which is not particularly carefully monitored.

Most domestic banks are small by world standards. In addition, domestic business is now going through a stage of high criminalization and small banks are more easily influenced by criminal structures or even created by them. It is quite common for clients (“scammers”) to take out a loan in advance without intending to repay it. Bank employees, who have low wages by world standards, are often bribed. There are many “pocket” banks that are focused on serving their founders. Such founders are often given virtually free loans and the repayment of which is not particularly carefully monitored.

Recently, in Russia, Belarus and the Baltic states, the founders themselves have bankrupted a significant number of small banks. The scheme was standard: after registering the bank, new clients were attracted, who switched to settlement and cash services at the established bank or deposited money into it, and resources for interbank lending were actively attracted. After accumulating a fairly substantial amount in the bank, the bank’s founders were given particularly large loans, which together made the bank insolvent. After this, the founders left the game (if they had time), and third-party clients of the bank suffered losses.

Recently, in Russia, Belarus and the Baltic states, the founders themselves have bankrupted a significant number of small banks. The scheme was standard: after registering the bank, new clients were attracted, who switched to settlement and cash services at the established bank or deposited money into it, and resources for interbank lending were actively attracted. After accumulating a fairly substantial amount in the bank, the bank’s founders were given particularly large loans, which together made the bank insolvent. After this, the founders left the game (if they had time), and third-party clients of the bank suffered losses.

Abuses can occur in many departments of the bank. Let's consider the main methods of possible fraud in banking divisions. Fraud occurs quite often when providing cash services to clients. Particularly wide opportunities for fraud open up when one person combines the functions of an accountant and an operator. The most common methods are the following.

Abuses can occur in many departments of the bank. Let's consider the main methods of possible fraud in banking divisions. Fraud occurs quite often when providing cash services to clients. Particularly wide opportunities for fraud open up when one person combines the functions of an accountant and an operator. The most common methods are the following.

1. “Brazen” shortage. A large sum is stolen from the bank's cash register and this is not hidden in any way, so the cashier hopes to escape before the audit of the cash register begins. A man comes to the bank director: - Are you looking for a new cashier? - And the old one too.

1. “Brazen” shortage. A large sum is stolen from the bank's cash register and this is not hidden in any way, so the cashier hopes to escape before the audit of the cash register begins. A man comes to the bank director: - Are you looking for a new cashier? - And the old one too.

This method, like some of the frauds discussed below, has mainly historical value, since most banks currently have fairly strict controls and carry out a daily inventory of cash balances.

This method, like some of the frauds discussed below, has mainly historical value, since most banks currently have fairly strict controls and carry out a daily inventory of cash balances.

2. Fabrication of monetary documents covering the shortfall After taking money from the cash register “for a while” and the inability to return it, it is possible to fabricate monetary documents to cover the amount of the shortfall (for example, issuing a debit order).

2. Fabrication of monetary documents covering the shortfall After taking money from the cash register “for a while” and the inability to return it, it is possible to fabricate monetary documents to cover the amount of the shortfall (for example, issuing a debit order).

3. The cashier allegedly made a mistake. A small amount of money is withdrawn, a shortage is reported, which allegedly arose due to an error in previously made calculations, and it is proposed to redo the old documents to achieve “complete openwork.” In this way, small sums are stolen, but if you skillfully “fool the head” of the higher authorities, who unquestioningly accept corrections, the sum can be quite large.

3. The cashier allegedly made a mistake. A small amount of money is withdrawn, a shortage is reported, which allegedly arose due to an error in previously made calculations, and it is proposed to redo the old documents to achieve “complete openwork.” In this way, small sums are stolen, but if you skillfully “fool the head” of the higher authorities, who unquestioningly accept corrections, the sum can be quite large.

4. Theft of money by an unauthorized person This possibility arises in case of negligence of cashiers who allow unauthorized persons to enter the cash register premises. There are also many ways for scammers to deceive a careless and inexperienced cashier. In foreign practice, there is a known case when, when checking a cash register, the auditor destroyed his own check. However, such actions are not effective if the check is already entered in the check register. In some cases, the partner's checks are destroyed. As a result, the cashier will have a shortfall in the amount of the check, and the auditor and his companion will receive income. The person committing the crime does not have to be a bank employee. In the absence of a suitably equipped cashier's workplace, theft can also be committed by an unauthorized person.

4. Theft of money by an unauthorized person This possibility arises in case of negligence of cashiers who allow unauthorized persons to enter the cash register premises. There are also many ways for scammers to deceive a careless and inexperienced cashier. In foreign practice, there is a known case when, when checking a cash register, the auditor destroyed his own check. However, such actions are not effective if the check is already entered in the check register. In some cases, the partner's checks are destroyed. As a result, the cashier will have a shortfall in the amount of the check, and the auditor and his companion will receive income. The person committing the crime does not have to be a bank employee. In the absence of a suitably equipped cashier's workplace, theft can also be committed by an unauthorized person.

5. Concealment of the attracted deposit The client is given all the necessary documents about attracting his money to the deposit, but this money is not recorded. Upon expiration of the deposit period (and fraudulent transactions are usually carried out with long-term deposits), the money is returned to him by non-receipt of funds deposited by another client (the so-called “overlap operation”). Almost always, with such fraud, the shortage continues to increase until the trick is revealed with sad consequences for the cashier.

5. Concealment of the attracted deposit The client is given all the necessary documents about attracting his money to the deposit, but this money is not recorded. Upon expiration of the deposit period (and fraudulent transactions are usually carried out with long-term deposits), the money is returned to him by non-receipt of funds deposited by another client (the so-called “overlap operation”). Almost always, with such fraud, the shortage continues to increase until the trick is revealed with sad consequences for the cashier.

A type of concealment of a deposit may be some underestimation in bank documents of the actual amount deposited. If the understatement of the amount is insignificant, the term and interest are quite large, and the client does not like to check the correctness of calculation of the income received, then there may not even be a need to compensate for the previously taken deposit, since the “accumulated” interest will disguise the theft.

A type of concealment of a deposit may be some underestimation in bank documents of the actual amount deposited. If the understatement of the amount is insignificant, the term and interest are quite large, and the client does not like to check the correctness of calculation of the income received, then there may not even be a need to compensate for the previously taken deposit, since the “accumulated” interest will disguise the theft.

6. Write-off of funds from client accounts If an accountant is lazy and does not carefully monitor the movement of money in the account of his company, the money may be written off to a third company. If the client discovers a write-off, the fraudster apologizes to him and the money is returned. If the client does not notice anything, the income is received.

6. Write-off of funds from client accounts If an accountant is lazy and does not carefully monitor the movement of money in the account of his company, the money may be written off to a third company. If the client discovers a write-off, the fraudster apologizes to him and the money is returned. If the client does not notice anything, the income is received.

7. Transfer of money on behalf of the bank Money is not withdrawn from the client’s current account, but a payment is made on behalf of the bank to some company, for example, “for the purchase of a computer”, “for consulting services”, income on a deposit, etc. absence (or fabrication) of supporting documents.

7. Transfer of money on behalf of the bank Money is not withdrawn from the client’s current account, but a payment is made on behalf of the bank to some company, for example, “for the purchase of a computer”, “for consulting services”, income on a deposit, etc. absence (or fabrication) of supporting documents.

8. Substitution of counterfeit real currency The majority of clients still believe in banks and their employees. This makes it possible to sell counterfeit banknotes through the bank.

8. Substitution of counterfeit real currency The majority of clients still believe in banks and their employees. This makes it possible to sell counterfeit banknotes through the bank.

Although the slipping of counterfeit dollars and German marks happens quite often (especially at exchange offices), tellers of large banks prefer to take fewer risks. Their main “prank” in this regard is handing out old and tattered bills instead of new ones, which are difficult to sell for the full denomination.

Although the slipping of counterfeit dollars and German marks happens quite often (especially at exchange offices), tellers of large banks prefer to take fewer risks. Their main “prank” in this regard is handing out old and tattered bills instead of new ones, which are difficult to sell for the full denomination.

There have been cases where the same cashiers, after some time, accepted previously issued banknotes from a client who was desperate to sell them for part of the face value. Then these bills were again slipped into the packet of the inattentive client and the story repeated itself. In foreign practice, it is also common to slip counterfeit bills and other securities.

There have been cases where the same cashiers, after some time, accepted previously issued banknotes from a client who was desperate to sell them for part of the face value. Then these bills were again slipped into the packet of the inattentive client and the story repeated itself. In foreign practice, it is also common to slip counterfeit bills and other securities.

9. Pulling money out of bundles If a client receives a fairly large amount of money, then at the bank he often does not have the opportunity to recalculate the amount of money in each bundle. The money is taken away from the bank without being counted and only in the client’s office does the cashier count it. A shortage is discovered, to which the bank teller reacts with Olympian calm: “I should have recalculated it at the bank!” If a client discovers a shortage in the bank, they apologize to him and give him the money correctly.

9. Pulling money out of bundles If a client receives a fairly large amount of money, then at the bank he often does not have the opportunity to recalculate the amount of money in each bundle. The money is taken away from the bank without being counted and only in the client’s office does the cashier count it. A shortage is discovered, to which the bank teller reacts with Olympian calm: “I should have recalculated it at the bank!” If a client discovers a shortage in the bank, they apologize to him and give him the money correctly.

In domestic banks, in an era of non-payments, it is possible to marinate clients until almost lunchtime, and then start giving them money to everyone at once, creating chaos. In addition, clients' employees are waiting for wages, so accountants often have no time for recalculations. In foreign practice, bills of exchange are removed from standard packages or bills of exchange for large amounts are replaced with bills of smaller denominations.

In domestic banks, in an era of non-payments, it is possible to marinate clients until almost lunchtime, and then start giving them money to everyone at once, creating chaos. In addition, clients' employees are waiting for wages, so accountants often have no time for recalculations. In foreign practice, bills of exchange are removed from standard packages or bills of exchange for large amounts are replaced with bills of smaller denominations.

10. Deception of illiterate, gullible or sick clients The domestic population can be considered as universally literate and intelligent only for propaganda purposes. In practice, not only many grandfathers and old women, but middle-aged people and young people are ready to sign everything that the bank does not offer. The same method is also applied to those with poor vision, for whom the cashier fills out all the documents and says: “Sign here.”

10. Deception of illiterate, gullible or sick clients The domestic population can be considered as universally literate and intelligent only for propaganda purposes. In practice, not only many grandfathers and old women, but middle-aged people and young people are ready to sign everything that the bank does not offer. The same method is also applied to those with poor vision, for whom the cashier fills out all the documents and says: “Sign here.”

11. Write-off of the shortage to other divisions of the bank When employees of the cash settlement center have access to accounting documents, the shortage that arises is often written off to other divisions of the bank, where the shortage can only be discovered after a certain period of time. The delay in time allows you to confuse the situation.

11. Write-off of the shortage to other divisions of the bank When employees of the cash settlement center have access to accounting documents, the shortage that arises is often written off to other divisions of the bank, where the shortage can only be discovered after a certain period of time. The delay in time allows you to confuse the situation.

12. Methods of combating cash and settlement fraud In order to minimize the possibility of fraud in the cash and settlement centers of banks, it is necessary to: Carry out frequent unannounced cash recalculations both at the cash desks and in the vault. Cash desk work should have as little connection as possible with accounting banking operations. Cash desk employees should not be involved in drawing up deposit agreements or issuing certificates of deposit.

12. Methods of combating cash and settlement fraud In order to minimize the possibility of fraud in the cash and settlement centers of banks, it is necessary to: Carry out frequent unannounced cash recalculations both at the cash desks and in the vault. Cash desk work should have as little connection as possible with accounting banking operations. Cash desk employees should not be involved in drawing up deposit agreements or issuing certificates of deposit.

Only cashiers should handle cash. If an inspector or auditor checking the cash register is allowed to access the money, then control must be organized over him by the cash desk employees. Cashiers should not be allowed to fill out paperwork for their customers. If the client is poorly educated or ill, a special employee who is not involved in cash management services should help draw up documents. All transactions passing through the cashier must be properly identified as having been processed by him. All wrapped money should be marked with the cashier's name and the date the money was placed in the package.

Only cashiers should handle cash. If an inspector or auditor checking the cash register is allowed to access the money, then control must be organized over him by the cash desk employees. Cashiers should not be allowed to fill out paperwork for their customers. If the client is poorly educated or ill, a special employee who is not involved in cash management services should help draw up documents. All transactions passing through the cashier must be properly identified as having been processed by him. All wrapped money should be marked with the cashier's name and the date the money was placed in the package.

It is unacceptable, even at the client’s request, for the client’s savings book, his certificate of deposit, the client’s copy of the deposit agreement, etc. to be kept by an employee of the cash settlement center. It is strictly forbidden to leave large amounts of cash in sight of visitors or unauthorized bank employees. There are many tricks to distract the cashier and "fish" for money. All transfers of funds must be verified by an official so that fictitious movements of funds cannot be used for the "overlap" operation.

It is unacceptable, even at the client’s request, for the client’s savings book, his certificate of deposit, the client’s copy of the deposit agreement, etc. to be kept by an employee of the cash settlement center. It is strictly forbidden to leave large amounts of cash in sight of visitors or unauthorized bank employees. There are many tricks to distract the cashier and "fish" for money. All transfers of funds must be verified by an official so that fictitious movements of funds cannot be used for the "overlap" operation.

Shortages or surpluses found in the cash register must be immediately reflected in the consolidated accounting records. Client complaints about the cash settlement center are considered by an official not directly related to the employees of the specified structure.

Shortages or surpluses found in the cash register must be immediately reflected in the consolidated accounting records. Client complaints about the cash settlement center are considered by an official not directly related to the employees of the specified structure.

Fraud in the credit department (management) The very specifics of the work of credit departments (in large banks - credit departments) provide significant opportunities for abuse. The following types of fraud may occur in banks that do not take proper security measures.

Fraud in the credit department (management) The very specifics of the work of credit departments (in large banks - credit departments) provide significant opportunities for abuse. The following types of fraud may occur in banks that do not take proper security measures.

A loan secured by a “bogus” collateral or guarantee. The favorite pastime of domestic scammers is to take a loan and then not repay it. Moreover, when taking out a loan, they often do not have sufficient collateral or guarantee, and therefore they need a trusting relationship with the staff of the credit department, unless, of course, they have access to the bank’s senior management. It is not uncommon for employees of this department to help a dubious client obtain a loan, receiving a commission of up to 30 percent of the future non-repayable loan.

A loan secured by a “bogus” collateral or guarantee. The favorite pastime of domestic scammers is to take a loan and then not repay it. Moreover, when taking out a loan, they often do not have sufficient collateral or guarantee, and therefore they need a trusting relationship with the staff of the credit department, unless, of course, they have access to the bank’s senior management. It is not uncommon for employees of this department to help a dubious client obtain a loan, receiving a commission of up to 30 percent of the future non-repayable loan.

All collateral offered as security for a loan must be examined by responsible persons of the bank who are not directly related to the employees issuing the loan. This study should have the purpose of determining the real value of the collateral both before obtaining a loan and as the loan is repaid.

All collateral offered as security for a loan must be examined by responsible persons of the bank who are not directly related to the employees issuing the loan. This study should have the purpose of determining the real value of the collateral both before obtaining a loan and as the loan is repaid.

Unjustified loans to companies in which there is a personal interest It is not uncommon for senior bank officials to have shares or other economic interests in commercial structures. Moreover, they often themselves or through figureheads are members of the management bodies of such structures. Naturally, they are interested in the prosperity of their commercial enterprises, even to the detriment of the bank. As a result, “their” enterprises often receive a loan at a preferential interest rate even in the absence of collateral or a guarantor.

Unjustified loans to companies in which there is a personal interest It is not uncommon for senior bank officials to have shares or other economic interests in commercial structures. Moreover, they often themselves or through figureheads are members of the management bodies of such structures. Naturally, they are interested in the prosperity of their commercial enterprises, even to the detriment of the bank. As a result, “their” enterprises often receive a loan at a preferential interest rate even in the absence of collateral or a guarantor.

If a loan is issued by decision of the bank's senior management, all documents regarding the loan are filled out relatively correctly. However, if a loan to “your” enterprise needs to be extended by a mid-level bank manager, then the method of replacing the first sheet of the loan agreement, which indicates the loan amount, its term, and interest rate, is used. The signatures of the bank's management are usually on the second (non-replaceable) sheet. Naturally, problems arise in connection with the availability of consolidated reporting on loans, but in practice they are completely solvable.

If a loan is issued by decision of the bank's senior management, all documents regarding the loan are filled out relatively correctly. However, if a loan to “your” enterprise needs to be extended by a mid-level bank manager, then the method of replacing the first sheet of the loan agreement, which indicates the loan amount, its term, and interest rate, is used. The signatures of the bank's management are usually on the second (non-replaceable) sheet. Naturally, problems arise in connection with the availability of consolidated reporting on loans, but in practice they are completely solvable.

Wrongful release of collateral The bank may suffer significant losses due to the release of collateral for a loan. In domestic practice, everything is done quite primitively. A client who has taken out a loan begins to understand at a certain stage (if he did not foresee this from the very beginning) that he will not be able to repay the loan received. Under normal conditions, he does not have the opportunity to get back his collateral, which, according to the rules, should not be at the client’s disposal. However, he sometimes tearfully begs for it on the grounds that he is urgently needed for work.

Wrongful release of collateral The bank may suffer significant losses due to the release of collateral for a loan. In domestic practice, everything is done quite primitively. A client who has taken out a loan begins to understand at a certain stage (if he did not foresee this from the very beginning) that he will not be able to repay the loan received. Under normal conditions, he does not have the opportunity to get back his collateral, which, according to the rules, should not be at the client’s disposal. However, he sometimes tearfully begs for it on the grounds that he is urgently needed for work.

One domestic client provided several MAZ trucks as collateral. When the loan repayment period began to expire and the credit department began to worry, the client ran to the bank and joyfully reported that the goods with the sale of which he would pay for the loan had already arrived at the Brest customs and had already been released, as he showed the corresponding faxes. All that remains is to bring the goods to stores. But since the client’s money is running out, he cannot rent a vehicle. Therefore, he asked to return the pawned cars for a few days and promised that then everything would be fine.

One domestic client provided several MAZ trucks as collateral. When the loan repayment period began to expire and the credit department began to worry, the client ran to the bank and joyfully reported that the goods with the sale of which he would pay for the loan had already arrived at the Brest customs and had already been released, as he showed the corresponding faxes. All that remains is to bring the goods to stores. But since the client’s money is running out, he cannot rent a vehicle. Therefore, he asked to return the pawned cars for a few days and promised that then everything would be fine.

And although the bank knew how easy it was to falsify fax messages, they accommodated the client halfway and disclosed the deposit. As a result, the loan money went abroad irrevocably, and the cars were sold to an unsuspecting buyer. In foreign practice, everything is done more elegantly. At an American bank, a cotton broker was heavily indebted to the bank for bills of exchange, guaranteed by sales receipts covering large quantities of cotton. The decline in the cotton market has led

And although the bank knew how easy it was to falsify fax messages, they accommodated the client halfway and disclosed the deposit. As a result, the loan money went abroad irrevocably, and the cars were sold to an unsuspecting buyer. In foreign practice, everything is done more elegantly. At an American bank, a cotton broker was heavily indebted to the bank for bills of exchange, guaranteed by sales receipts covering large quantities of cotton. The decline in the cotton market has led

to the fact that the bank refrained from selling the collateral in the hope that the market value of cotton would increase. This should have allowed the loan to be repaid. Meanwhile, the broker needed additional funds, but his loan applications were rejected. To solve the problem, the bank teller, without the knowledge of the board of directors, released to the debtor the above sales receipts covering a large amount of cotton. The broker then drew up bills of exchange for one of his country offices, attached exempt sales receipts to them, and presented them to the bank teller for accounting.

to the fact that the bank refrained from selling the collateral in the hope that the market value of cotton would increase. This should have allowed the loan to be repaid. Meanwhile, the broker needed additional funds, but his loan applications were rejected. To solve the problem, the bank teller, without the knowledge of the board of directors, released to the debtor the above sales receipts covering a large amount of cotton. The broker then drew up bills of exchange for one of his country offices, attached exempt sales receipts to them, and presented them to the bank teller for accounting.

The amount paid upon discounting the note was deposited in the account of the broker, who promptly used the capital to pay the temporary obligations. Subsequently, the broker's country office paid the bill of exchange and returned the sales receipts to the bank teller, who replaced them in the collateral paper file. This operation was repeated several times until the bank controller eventually discovered the fraud.

The amount paid upon discounting the note was deposited in the account of the broker, who promptly used the capital to pay the temporary obligations. Subsequently, the broker's country office paid the bill of exchange and returned the sales receipts to the bank teller, who replaced them in the collateral paper file. This operation was repeated several times until the bank controller eventually discovered the fraud.

Underestimation of income received from loans issued In practice, the most common practice is for a mid-level manager, vested with appropriate authority, to issue a loan at a lower interest rate than the average for the bank. It is not difficult to find a justification for a low interest rate, especially if the issuance of such a loan is accompanied by a bribe

Underestimation of income received from loans issued In practice, the most common practice is for a mid-level manager, vested with appropriate authority, to issue a loan at a lower interest rate than the average for the bank. It is not difficult to find a justification for a low interest rate, especially if the issuance of such a loan is accompanied by a bribe

In banks with poorly established accounting for loan repayments, there are certain opportunities for misappropriation of funds by understating the interest received on the loan. In addition, it is possible to temporarily misappropriate funds in case of early repayment of loans. When working with cash, the corresponding amount of funds is withdrawn from the cash register. In a foreign bank, an assistant cashier serviced interest on loans. When compiling the accounting register at the end of the working day, he understated the total interest income received and took the corresponding amount of cash from the cash desk.

In banks with poorly established accounting for loan repayments, there are certain opportunities for misappropriation of funds by understating the interest received on the loan. In addition, it is possible to temporarily misappropriate funds in case of early repayment of loans. When working with cash, the corresponding amount of funds is withdrawn from the cash register. In a foreign bank, an assistant cashier serviced interest on loans. When compiling the accounting register at the end of the working day, he understated the total interest income received and took the corresponding amount of cash from the cash desk.

Taking on an unreasonably large loan amount Most banks give their employees the opportunity to take out a certain amount of loan on favorable terms. In some cases, a credit line is opened for them within the established limit. Such loans are periodically reviewed by bank management and credit committees. Nevertheless, some bank officials in practice manage to obtain an unreasonably large loan without notifying the bank management about it, for example, by fictitiously distributing it to several subordinate bank employees.

Taking on an unreasonably large loan amount Most banks give their employees the opportunity to take out a certain amount of loan on favorable terms. In some cases, a credit line is opened for them within the established limit. Such loans are periodically reviewed by bank management and credit committees. Nevertheless, some bank officials in practice manage to obtain an unreasonably large loan without notifying the bank management about it, for example, by fictitiously distributing it to several subordinate bank employees.

Forging signatures on clients' bills This operation is still exotic for domestic businesses, but is quite common abroad. Foreign banks issue loans against borrowers' bills of exchange, and in this case, to commit theft it is enough to forge such a bill of exchange. The existence of counterfeit bills is sometimes discovered when the bills are reviewed by officials familiar with the borrowers' signatures. However, in practice bills of exchange are checked quite rarely.

Forging signatures on clients' bills This operation is still exotic for domestic businesses, but is quite common abroad. Foreign banks issue loans against borrowers' bills of exchange, and in this case, to commit theft it is enough to forge such a bill of exchange. The existence of counterfeit bills is sometimes discovered when the bills are reviewed by officials familiar with the borrowers' signatures. However, in practice bills of exchange are checked quite rarely.

The most effective way to establish the authenticity of bills of exchange is their direct confirmation by the borrowers. Other methods include comparing signatures on documents with signatures of the same person on previously submitted documents held by the bank, as well as tracking the payment of amounts on documents. In large banks, work should be distributed among department employees in such a way as to eliminate the very possibility of counterfeiting (provided that there is no conspiracy between them). In small banks, such precautions are unlikely due to the limited number of employees.

The most effective way to establish the authenticity of bills of exchange is their direct confirmation by the borrowers. Other methods include comparing signatures on documents with signatures of the same person on previously submitted documents held by the bank, as well as tracking the payment of amounts on documents. In large banks, work should be distributed among department employees in such a way as to eliminate the very possibility of counterfeiting (provided that there is no conspiracy between them). In small banks, such precautions are unlikely due to the limited number of employees.

Fraud with discounted bills Another method that is still exotic for our conditions. When using it, bills of exchange already discounted by the bank are withdrawn for re-discounting in another bank or even in the same bank. The official responsible for accounting and storage of discounted bills of exchange has the opportunity to perform such an operation.

Fraud with discounted bills Another method that is still exotic for our conditions. When using it, bills of exchange already discounted by the bank are withdrawn for re-discounting in another bank or even in the same bank. The official responsible for accounting and storage of discounted bills of exchange has the opportunity to perform such an operation.

Loans against false debtor accounts This method is used when issuing loans secured by funds in the accounts of the loan recipient. In this case, there is scope for abuse by issuing false invoices. To prevent fraud, the bank must verify the authenticity of accounts receivable.

Loans against false debtor accounts This method is used when issuing loans secured by funds in the accounts of the loan recipient. In this case, there is scope for abuse by issuing false invoices. To prevent fraud, the bank must verify the authenticity of accounts receivable.

Misappropriation of funds by gaining confidence in the recipient of the loan In foreign practice, there have been cases when a bank employee misappropriated large sums of money using checks left at the bank by borrowers in order to pay for the received loans at the end of the term. The employee convinced his clients to write checks dated at a future date and give them to him for safekeeping. He then changed the dates of the checks and received cash on them, motivating his actions by the fact that the checks were issued to repay a debt that was due on the day the money was received.

Misappropriation of funds by gaining confidence in the recipient of the loan In foreign practice, there have been cases when a bank employee misappropriated large sums of money using checks left at the bank by borrowers in order to pay for the received loans at the end of the term. The employee convinced his clients to write checks dated at a future date and give them to him for safekeeping. He then changed the dates of the checks and received cash on them, motivating his actions by the fact that the checks were issued to repay a debt that was due on the day the money was received.

The citizen who received the loan died. Employees of foreign banks servicing loans to the population with repayment in installments discover that the borrower has died and there is no one to ask for the loan. In some countries (for example, in the USA), it is easy to obtain a death certificate even for a living person. As a result, it becomes possible to defraud both the bank and the borrower's life insurers by submitting false death claims.

The citizen who received the loan died. Employees of foreign banks servicing loans to the population with repayment in installments discover that the borrower has died and there is no one to ask for the loan. In some countries (for example, in the USA), it is easy to obtain a death certificate even for a living person. As a result, it becomes possible to defraud both the bank and the borrower's life insurers by submitting false death claims.

Combating abuse in obtaining bank loans A policy against unjustified obtaining of bank loans should include the following points. Decisions on issuing loans are made only collectively at a meeting of the credit committee or a similar body. The powers of managers of various ranks to issue loans and set interest rates are clearly delineated.

Combating abuse in obtaining bank loans A policy against unjustified obtaining of bank loans should include the following points. Decisions on issuing loans are made only collectively at a meeting of the credit committee or a similar body. The powers of managers of various ranks to issue loans and set interest rates are clearly delineated.

All issued or extended loans are fully secured by liquid collateral at the disposal of the bank or by sureties (guarantees). Constant and careful monitoring of the availability of collateral for loans is carried out. Regular checks are carried out to verify the legality of issuing loans and setting interest rates. The spending of funds from the special loan account of the client who took out the loan is strictly controlled. Disinterested employees are appointed to verify the obligations of each borrower.

All issued or extended loans are fully secured by liquid collateral at the disposal of the bank or by sureties (guarantees). Constant and careful monitoring of the availability of collateral for loans is carried out. Regular checks are carried out to verify the legality of issuing loans and setting interest rates. The spending of funds from the special loan account of the client who took out the loan is strictly controlled. Disinterested employees are appointed to verify the obligations of each borrower.

The structure of most banks has departments (departments) for working with free financial resources and with securities (bonds, shares) for profitable investment of both their own funds and the free financial resources of clients. Typically, the same department also carries out trust operations. In small banks, such operations are usually carried out by one of the managers, and accounting documents are kept by an ordinary executive, who also exercises control over securities.

The structure of most banks has departments (departments) for working with free financial resources and with securities (bonds, shares) for profitable investment of both their own funds and the free financial resources of clients. Typically, the same department also carries out trust operations. In small banks, such operations are usually carried out by one of the managers, and accounting documents are kept by an ordinary executive, who also exercises control over securities.

The most common types of fraud are: “Selling” clients to another bank. It is a common practice for low- and mid-level bank employees to provide information about their clients to competing banks. At the same time, clients who wish to deposit significant amounts of money are specifically informed of reduced deposit rates. a) With a “brazen” approach to the client, the latter is informed that the namerek bank’s rate is much higher. The client thanks and takes the money to the specified bank. A bank employee regularly visits the name bank and lists clients whom he has “discouraged” from his bank and receives a commission from a competitor’s bank. If the management of a bank that has lost a client finds out about the tricks of its employee, he responds to the deposit that he was only fighting to reduce bank interest costs.

The most common types of fraud are: “Selling” clients to another bank. It is a common practice for low- and mid-level bank employees to provide information about their clients to competing banks. At the same time, clients who wish to deposit significant amounts of money are specifically informed of reduced deposit rates. a) With a “brazen” approach to the client, the latter is informed that the namerek bank’s rate is much higher. The client thanks and takes the money to the specified bank. A bank employee regularly visits the name bank and lists clients whom he has “discouraged” from his bank and receives a commission from a competitor’s bank. If the management of a bank that has lost a client finds out about the tricks of its employee, he responds to the deposit that he was only fighting to reduce bank interest costs.

b) With a more subtle approach, when it comes to a client who is a legal entity, the client is “discouraged” from his bank without saying anything extra, and then the potential client is reported to a competing bank. The latter processes the client himself and, if successful, pays a commission to the employee who provided the information. c) This option consists of creating a personal financial company of a bank employee, the founder of which is a figurehead. The scheme for raising funds is standard: the client is convinced that the bank’s deposit rates are low, while the financial company’s are high. The client gives the money to the financial company, which the fraudulent employee immediately deposits in a deposit account at his bank at a significantly higher interest rate.

b) With a more subtle approach, when it comes to a client who is a legal entity, the client is “discouraged” from his bank without saying anything extra, and then the potential client is reported to a competing bank. The latter processes the client himself and, if successful, pays a commission to the employee who provided the information. c) This option consists of creating a personal financial company of a bank employee, the founder of which is a figurehead. The scheme for raising funds is standard: the client is convinced that the bank’s deposit rates are low, while the financial company’s are high. The client gives the money to the financial company, which the fraudulent employee immediately deposits in a deposit account at his bank at a significantly higher interest rate.

Lowering rates when selling resources on the interbank market An employee confidentially negotiates with another bank to sell resources at a reduced interest rate. Then the difference (or part of the difference) in income at the real and reduced rate is given to the employee who ensured the sale of cheaper resources.

Lowering rates when selling resources on the interbank market An employee confidentially negotiates with another bank to sell resources at a reduced interest rate. Then the difference (or part of the difference) in income at the real and reduced rate is given to the employee who ensured the sale of cheaper resources.

Withholding Part of the Proceeds from the Sale of Client Securities Clients who sell their securities through a bank broker often do not compare the interest income reported on the securities sale report received from the bank broker with the market price of the securities on the date of sale. This makes it possible to understate the real price in the report on the sale of securities and thereby provide personal income, often registered to a third company as a commission for intermediary.

Withholding Part of the Proceeds from the Sale of Client Securities Clients who sell their securities through a bank broker often do not compare the interest income reported on the securities sale report received from the bank broker with the market price of the securities on the date of sale. This makes it possible to understate the real price in the report on the sale of securities and thereby provide personal income, often registered to a third company as a commission for intermediary.

In practice, such activities have little control and a specialist in such operations has practically no problems until the client becomes indignant at the constant unsuccessful transactions of the bank broker with his securities. Since complaints about a broker are primarily made to the broker himself, the latter has the opportunity to re-register the results of transactions and peacefully resolve the conflict without informing the bank’s management about it.

In practice, such activities have little control and a specialist in such operations has practically no problems until the client becomes indignant at the constant unsuccessful transactions of the bank broker with his securities. Since complaints about a broker are primarily made to the broker himself, the latter has the opportunity to re-register the results of transactions and peacefully resolve the conflict without informing the bank’s management about it.

He will work more carefully with a corrosive client, taking it out on other clients. As a result, bank managers will be “ignorant” of these thefts and will not take measures to stop them. This type of fraud occurs not only when selling client securities, but also when purchasing them, when the report on the purchase of securities shows a price higher than the actual exchange rate.

He will work more carefully with a corrosive client, taking it out on other clients. As a result, bank managers will be “ignorant” of these thefts and will not take measures to stop them. This type of fraud occurs not only when selling client securities, but also when purchasing them, when the report on the purchase of securities shows a price higher than the actual exchange rate.

Concealment of funds intended for the purchase of securities A bank broker usually requires that when a client submits an application for the purchase of securities, funds sufficient to cover the cost of the securities applied for purchase at the time of delivery are also transferred. In foreign practice, there are cases when a broker, accepting a client’s order, forces him to write a check for an amount approximately equal to the value of the securities. The bank employee then cashes the check and steals the proceeds from the securities sale using

Concealment of funds intended for the purchase of securities A bank broker usually requires that when a client submits an application for the purchase of securities, funds sufficient to cover the cost of the securities applied for purchase at the time of delivery are also transferred. In foreign practice, there are cases when a broker, accepting a client’s order, forces him to write a check for an amount approximately equal to the value of the securities. The bank employee then cashes the check and steals the proceeds from the securities sale using

In small banks, it is extremely difficult to prevent this type of fraud. Typically, securities transactions are completely supervised by one employee, and in rare cases, some part of the transaction is reviewed by another officer or employee. If the broker is smart enough to hide his illegal actions, the shortage can be endless.

In small banks, it is extremely difficult to prevent this type of fraud. Typically, securities transactions are completely supervised by one employee, and in rare cases, some part of the transaction is reviewed by another officer or employee. If the broker is smart enough to hide his illegal actions, the shortage can be endless.