The property tax is measured in monetary equivalent and is charged for the use of individuals by the property of other individuals or entities of entrepreneurial activities. It is a direct way to receive a state tax service a certain percentage of owners of all categories of property.

Payers of the duty are the owners of a specific property for which the duty should pay for possession. The main criterion for determining the object, the use of which implies the payment of the duty, is the fact of the availability of a certain ownership of it.

Tax Objects

Calculation of property of the property of individuals is carried out on taxation facilities, which, according to current legislation, are considered:

- residential premises presented in the form of an apartment, or a separate room;

- residential buildings, which contain elements of residential premises;

- vehicle parking place or garage establishment;

- construction complexes of real estate;

- construction objects in unfinished status;

- facilities without targeted purposes;

- premises that do not have a targeted purpose;

- houses for accommodation located in the land plots related to the category intended for the management of personal purpose.

If the objects for which according to regulatory acts, the fees are assumed throughout the year are not used for any purpose, this fact is not the basis for non-payment of the payment.

Not taxed property that is a component of general ownership.

Privileges

The legislation provides for benefits for citizens living and registered in the country, on the basis of which they are exempt from paying duty in full or in partial amount of payment. Such benefits enjoy the citizens of the states who took part in the events to preserve the integrity of the border of the state, as well as disabled people who have received injuries in the process of fulfilling military obligations.

The owners of the premises, owners of buildings and structures are fully exempted from payment, provided that they refer to the category of pensioners or servicemen during the fulfillment of military obligations.

Decisions on the decrease in interest rates, as well as the introduction of additional benefits are made by state authorities and local self-government.

It should be noted that in the villages of the urban type and in villages there is a restriction on the provision of benefits, since in these areas and the method of truncated calculation of the size of the duty is used.

Separate payers of the duty after considering the documentation package by municipal authorities may apply individual benefits.

Tax value determination

It is convenient to calculate property tax on inventory value. The basis for calculating the duty is the tax base, which is formed in the form of a total value of an inventory type of object at the beginning of the beginning of the month of each year. It is determined by summing the cost of the components of the elements of the property recognized as the object of taxation. The definition of the indicator is carried out taking into account the requirements of the region, where the object is located and where the rate is set for the work of the calculations.

Calculation of the cost of inventory type is carried out taking into account the wear and dynamics of price changes for building materials from which property object is made.

How to calculate the inventory cost of the object

The value is determined on the basis of the value criteria relating to the reducing category in relation to the object. Physical wear is taken into account in accordance with the operation time.

All indicators must be correct at the time of evaluation.

Data for determining the replacement cost is in special collections of enlarged values. It should be calculated taking into account current indexes and coefficients operating at the time of the calculation, which are approved by the executive authorities of the constituent entities of the Russian Federation.

In some regions, the bodies of the municipal entity class the coefficients of the recalculation of duty by the type of property and its components on the principle of "residential and non-residential". In such a situation, the total value of an inventory type should be determined separately for each element, followed by summing values.

In a situation of establishing tax rates without taking into account the criterion of the property, the total cost of inventory can be determined by the object as a whole.

It should be noted that the regulatory documents provide rates that cannot be exceeded by the indication of the competent authorities.

Tax rates

Tax rates are determined at the legislative level through the approval of the regulatory documentation. The size of the indicator is in direct dependence on the inventory value of the property obtained by summing the corresponding values \u200b\u200bof the components of the elements. In determining the coefficient, the competent authorities have the right to adjust the value of the tax amount obtained, based on the characteristics of the object:

- appointment;

- cost;

- location.

The legislation of the Russian Federation provides limitations of the indicator depending on the value of the property with which you can find in the table.

At the legislative level, municipalities allowed to review the differentiation of rates depending on the cost of inventory and other criteria.

When calculating the indicator regarding buildings, structures and premises, which are in possession of shared property rights in several individuals, the calculation, accrual and payment of the tax is carried out on the basis of these owners, commensurate with its share of ownership in the total unit of property. In this case, the share inventory value is determined by means of an indicator calculated per unit of property to the share of ownership in percentage.

How tax on property of individuals is calculated

Calculation of property of individuals can be carried out in two schemes that depend on the type of property that may be:

- commonly owned;

- owned by ownership of a certain part.

The formula for calculating the tax on property of individuals owning equity property consists of a product of indicators:

- the cost of the object of ownership in the inventory perspective at the beginning of the calendar year;

- applied tax rate;

- property share.

It should be noted that in such a situation, each owner brings to the state equal responsibility for the execution of tax liabilities. For this reason, each entity is reported on the part of its possession and pays for her a duty on his own, without taking into account the data of co-owners.

When calculating the indicator characteristic of the total ownership, the tax is calculated based on the product of the values:

- inventory value of property at the beginning of the year;

- tax rate;

- number of owners.

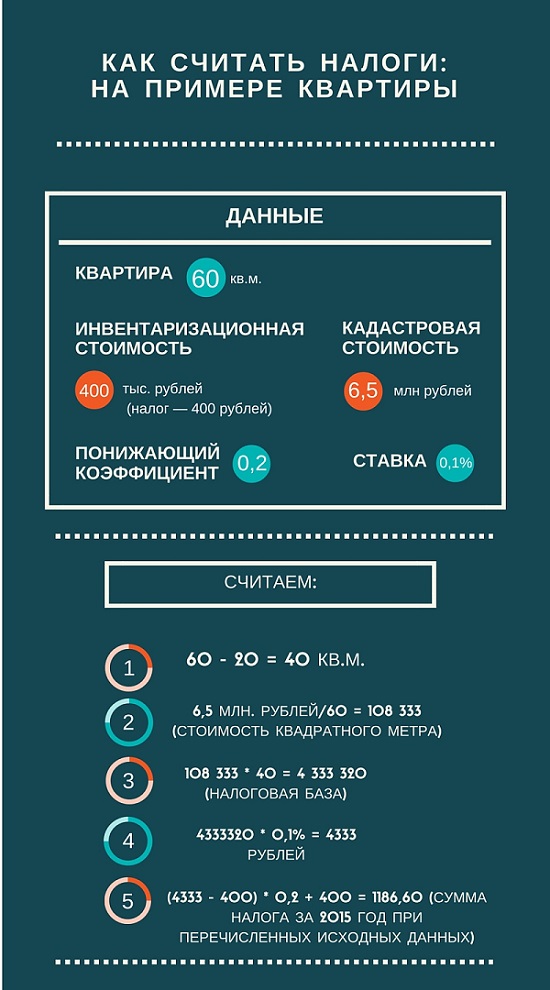

An example of calculating the property of individuals of individuals

For example, consider the calculation of the tax subject to payment for possession one-room apartment, the area of \u200b\u200b35 square meters. The apartment is in the use of one owner who no longer has real estate.

The cadastral value of the object is 180,000 rubles. Calculation of tax produces from accounting difference area of \u200b\u200bhousing and tax deductions of 20 square meters. The obtained 15 square meters have the cost corresponding to the product of cadastral value per residual area, which corresponds to 2,700 000 rubles.

Applying a bid 0.1 percent in accordance with regulatory acts, the amount of tax will correspond to 2700 rubles each yearuntil there is a change in the rate.

Calculation of property tax on cadastral value

To calculate property tax on cadastral value, you need to know this value that is revised once every five years. The definition of the value of the criterion is carried out by independent appraisers in the process of implementing the state assessment program. This information is contained in the state real estate cadastre. Currently, state executive authorities seek to equate the value of the magnitude of market indicators.

When calculating property tax on real estate, you must multiply the cadastral value of the object (based on the price per square meter) to the value of the area to be taxed. Multiplying the value to the tax coefficient, the amount relying on the payment for special details of the tax service. This value corresponds to the difference in the total area of \u200b\u200bthe object under consideration and tax deduction.

Applying information to the tax service and payment procedure

Calculation and accrual of duty is made according to the results of ownership of the year, expressed in the calendar dimension. There are no reporting periods characteristic of other types of taxes in this area.

Calculation of tax is carried out by the tax authorities on the basis of the data provided by the taxpayer. This takes into account:

- state registration of rights to real estate property;

- implemented transactions for the calendar year;

- conducted technical inventory work.

All the necessary information to determine the amount of tax must be submitted to the tax service until March 1. Payment must be made on a settlement account to the local budget at the place of registration of the tax object. Notifications of the amount led to payment are carried out by tax authorities in accordance with the Tax Code of the Russian Federation.

Payment must be carried out by taxpayers until November 1, following the estimated period.

In the case of ownership of new buildings, premises and structures, the tax should be paid at the beginning of the yearfollowing the calendar year in which work was carried out on the construction and construction of objects.

When making an inheritance, the duty is paid at the time of entry into the possession of inheritance.

If, throughout the calendar year, the tax object was destroyed or destroyed for various reasons, the payment of the duty ceases from the moment the event on the monthly calculus. The fact of what happened should be documented, as you should notify the tax service.

When carrying out operations with real estate in the field of purchase / sale, as a result of which the rights of ownership move from one owner to another, during the calendar year the tax is charged at the initial owner before the start of the month of the transaction. The new property owner pays the duty from the month of entry into possession of property.

For any person living in the country and has any property presented in the form of immovable or movable property, it is important to be able to independently determine the amount of tax subject to payment in order to competently plan your budget, distributing the receipt of funds in a timely manner.