Any organization, regardless of the nature of its activities, can create separate divisions. There can be as many of them as you like. The most common are representative offices and branches. But there are other structures. For example, stationary work positions can also have the status of “separate”. After receiving notification of the opening, the tax office assigns a checkpoint. Let's look at how to get and generally find out.

Peculiarities

Companies, in accordance with the Civil Code of the Russian Federation, can be created to conduct business activities in general or perform certain tasks. In this they are no different from other entities engaged in economic activities.

A legal entity has the opportunity to open its own separate divisions (hereinafter also referred to as OP). This right is enshrined in Art. 55 of the Civil Code. Let us clarify that merchants are formally deprived of this opportunity.

Opening an OP does not entail the creation of a separate legal entity. It is part of an already registered organization, which means it does not have the same scope of legal rights and obligations.

The Tax Code contains clear features that must necessarily be inherent in “separateness”:

- availability of stationary workplaces;

- different addresses for the head office and the OP.

The absence of at least one of these signs means that there are insufficient grounds for opening a new structure in the OP status. The creation of a “separateness” in this case will contradict Article 11 of the Tax Code. This means a separate Checkpoint of a separate unit there won't be.

The Civil Code mentions only two forms of OP:

- branch;

- representation.

At the same time, Art. 55 of the Tax Code of the Russian Federation provides another type of separate unit - equipped working positions.

The opening of branches and representative offices implies the appearance of data about them in the Unified State Register of Legal Entities (in the case of equipped workplaces with the status of EP, this does not happen). To do this, you must first fill out an application (there are approved forms) and send it to the tax authorities.

Basic codes

When the registration of an OP has occurred, it may be assigned special codes. But the parent organization and all its divisions will still have the same TIN. This is due to the fact that the OP is not a legal entity.

Thus, find out the checkpoint of a separate subdivision by TIN of the main enterprise by applying for an extract from the Unified State Register of Legal Entities.

The judgment that there is no need to obtain a separate TIN is based on an analysis of the regulatory document regulating the procedure for obtaining, using and changing the TIN (approved by order of the Ministry of Taxes of Russia dated 03.03.2004 No. BG-3-09/178). And it is valid only when registering or deregistering legal entities and individuals.

A TIN can only be assigned to the organization itself. None of its divisions, including separate ones, have the right to receive their own TIN. Only upon initial registration with the Federal Tax Service does the organization receive its TIN at the place of registration.

Right to a reason code

Absolutely any business entity receives certain codes, as stated in the law. They are needed for the following purposes:

- identification in classification systems according to various criteria (territory, industry, etc.);

- maintaining records of subjects (for the purposes of taxes and insurance premiums, statistics, etc.).

And if for the main organization codes are an integral attribute, then separate divisions may have their own or coincide with the codes of the main organization.

Any organization must register with the tax service before starting its activities. This is enshrined in paragraph 1 of Article 83 of the Tax Code of the Russian Federation. But not everyone understands which inspectorate they need to contact in order to register. Belonging to the Federal Tax Service can be determined:

- the address of the organization itself (for an individual entrepreneur - the address of his permanent registration);

- the location of its real estate;

- OP's address.

The organization is required to register with the tax office at the address not only of the head office, but also of all separate divisions.

The company must inform the tax authorities about the opening of a separate division. After this, it is registered.

Despite the fact that the parent organization and all its separate divisions have one TIN, KPP is assigned to each of them. This will happen even if the organization does not submit application to the checkpoint of a separate unit.

Then information about Checkpoint of a separate unit from the local tax office they are sent to the one where the parent company is registered.

According to the rules on TIN (approved by order of the Federal Tax Service dated June 29, 2012 No. ММВ-7-6/435), when creating any form of a separate unit, it must be assigned a checkpoint.

Why is it needed?

Regarding Checkpoint of a separate unit, then it is always different from the checkpoint of the parent enterprise. The bottom line is that the reasons for tax registration are initially different.

So why does every department need a checkpoint? So: if you decipher the set of numbers assigned to a separate structure - checkpoint, you can immediately determine:

- in which subject of the Russian Federation the OP is registered;

- for what reason was it created?

How to find out

Before you understand the decoding of the assigned checkpoints in order to obtain information about the OP, you need to understand how you can find out Checkpoint of a separate unit (according to TIN including).

Information about such structural divisions as branches and representative offices is displayed in the Unified State Register of Legal Entities (other types of EP do not appear in it). Tax officers transmit all checkpoint numbers of existing separate divisions to the inspectorate at the head office address.

Many people believe that in order to obtain information about Checkpoint of a separate unit Just go to the official website of the Federal Tax Service of Russia and request an extract from the Unified State Register of Legal Entities. The exact link is www.egrul.nalog.ru.

However, this won't help. The fact is that by order of the Ministry of Finance dated December 5, 2013 No. 115n, the exact composition of the information in the extract from the Unified State Register of Legal Entities was approved. And the checkpoint of the separate unit is not mentioned in it. Therefore, such an extract will not help to find out Checkpoint of a separate unit according to TIN.

Therefore, there are two options left:

- send a request to the tax office (or to the counterparty you are interested in);

- use various databases (but no one is responsible for their reliability).

How to decrypt

To decipher the checkpoint, you need to know what each number means (see table).

Where does it appear?

The checkpoint must be indicated as part of the details of the legal entity in all official papers and forms of the organization. It must be reflected in the texts of contracts, various letters and powers of attorney.

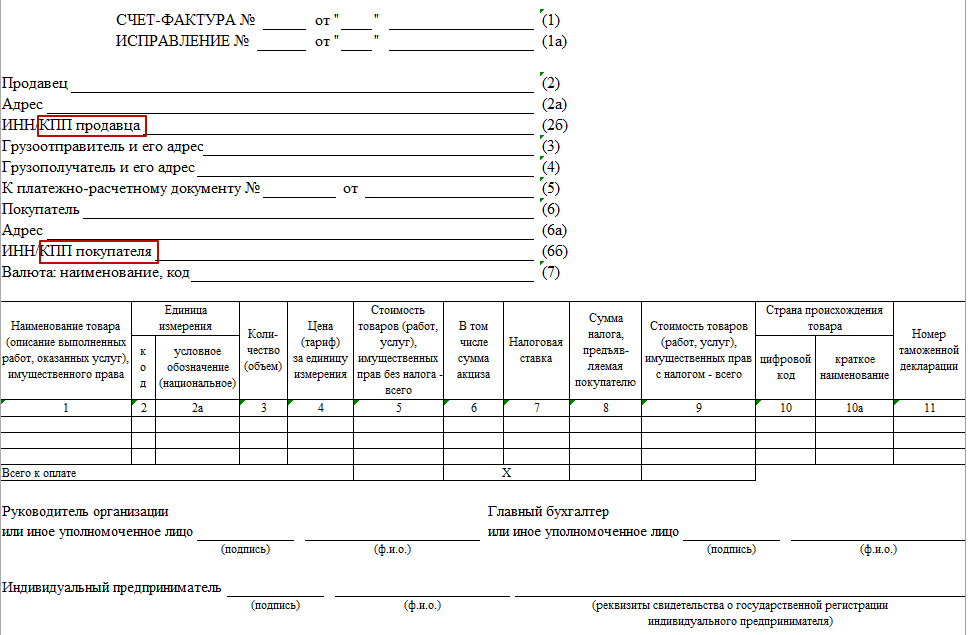

There are a number of forms in which checkpoints are a mandatory element. For example, Checkpoint in the invoice of a separate division. It is indicated when the OP sells something through himself.

EXAMPLE

The sale of goods produced by the parent organization is carried out by its separate division. Then in the invoice the checkpoint is written not of the main office, but of the OP that makes the transaction. The same rule applies if goods are purchased by a separate division.

But the TIN is indicated to the parent organization, since the OP does not have its own.

Tax authorities constantly require us to be careful when choosing suppliers, and it is accountants who are forced to carefully check all documents and pay attention to all kinds of details. We have long been accustomed to these abbreviations - INN and KPP. And it seems that no questions can arise here. Meanwhile, if many people have an idea about the TIN and know where it is check, then, besides how the checkpoint is deciphered, as a rule, no one else knows anything about it. These are the questions we are asked.

The checkpoint will help determine who you are dealing with: an organization or its branch

E.N. Dorofeeva, Orenburg

For all our counterparties, the checkpoint ends with 01001. But recently, while filling out a payment form, I discovered some strange checkpoint from a new supplier - the last numbers are 43001. How do you understand what this means?

: This checkpoint means that you are transferring money to a branch of your counterparty A.

The gearbox is a 9-digit digital code (hereinafter referred to as the Procedure).

1Art. 65 of the Constitution of the Russian Federation

For example, KPP 770601001 means that the organization is located in Moscow and the Federal Tax Service of Russia No. 6 for Moscow registered it as a taxpayer at its location (code 01).

The classifier “Tax Authority Designation System” (SONO) can be found: website of the Federal Tax Service of RussiaIf the 5th and 6th digits of the checkpoint (ZZ) are not 01 (for example, like your counterparty - 43), then this means that the organization was registered on other grounds.

A complete list of reason codes for registration is given in the departmental directory (SPPUNO) approved 10/11/99. But this guide is an internal document. And if previously it was posted for public viewing on the official website of the Federal Tax Service, now it is problematic to find it in the public domain. But we will tell you what some codes mean.

* These codes are not currently assigned I Letter of the Federal Tax Service of Russia dated 02.06.2008 No. CHD-6-6/396@. But checkpoints with these codes assigned earlier remain valid.

Gearbox may change

A.L. Zimina, Moscow

Our counterparty's checkpoint has changed. OGRN and TIN remain the same. What does this mean? Moving? Or could there be other options?

: The organization may have a new checkpoint, in particular And clause 2.1.4 of the Procedure:

Most often, the checkpoint changes if an organization moves and has to register with another tax office. And clause 2.1.4 of the Procedure; subp. “c” clause 1, clause 5 art. 5 of the Federal Law of 08.08.2001 No. 129-FZ “On state registration of legal entities and individual entrepreneurs”. For example, if the checkpoint used to be 77 07 01001, and then became 77 19 01001, this means that your counterparty was registered with the Federal Tax Service Inspectorate No. 7 for Moscow, and now with the Federal Tax Service Inspectorate No. 19 for Moscow.

If other numbers have changed in the checkpoint, for example, the reason code for the statement, then it is better to check with your counterparty to see if it is correct.

Different organizations may have the same checkpoint

V.S. Terentyeva, Moscow

Three of our counterparties have the same checkpoint. Is there something wrong with them? Or is this possible?

: Yes, it's possible. Unlike the TIN (a unique number that is assigned to an organization once at the time of registration and does not change I clause 7 art. 84 Tax Code of the Russian Federation; clause 3.1 of the Procedure), the checkpoint determines whether an organization belongs to a particular tax authority, as well as the reason for registration. Therefore, it may be the same for organizations registered with the same tax office on the same basis. m clause 1 of the Order.

The branch, when issuing an invoice, indicates its checkpoint in it

A.T. Seliverstova, Ekaterinburg

We purchased goods from a branch of our counterparty. He issued us an invoice on behalf of the parent organization, and indicated his own (branch) checkpoint. Is this correct? Can we be denied a deduction if the wrong checkpoint is indicated?

: Your counterparty did everything correctly. The regulatory authorities believe that when selling goods through separate divisions, the invoice must be issued on behalf of the parent organization, that is, in lines 2, 2a, 2b the name, tax identification number, location of the organization itself must be indicated, and in lines 2b and 3 - KPP and address of a separate division (branch )Letters of the Ministry of Finance of Russia dated May 23, 2011 No. 03-07-09/12, dated April 1, 2009 No. 03-07-09/15, dated October 22, 2008 No. 03-07-09/33; Letter of the Federal Tax Service of Russia for Moscow dated 07/07/2010 No. 16-15/071188.

As for the VAT deduction, previously tax authorities quite often refused it in the absence of a checkpoint or its incorrect indication, but the courts never supported them And Resolution of the Federal Antimonopoly Service of the Moscow Region dated December 17, 2008 No. KA-A40/11795-08; FAS NWO dated October 23, 2008 No. A56-39361/2007; FAS North Caucasus Region dated June 4, 2008 No. F08-3055/2008, dated October 28, 2008 No. F08-6493/2008. And after amendments were made to the Tax Code of the Russian Federation And clause 2 art. 169 Tax Code of the Russian Federation, according to which errors in invoices that do not interfere with the identification of the seller are not grounds for refusal of a deduction, there should be no problems at all. After all, the checkpoint does not interfere with such identification.

Entrepreneurs are not assigned a checkpoint

T.V. Makarova, Samara

Our buyer, an entrepreneur, sent us the details where the checkpoint is indicated and stated that he really has the code, but he cannot find a document confirming this. Do individual entrepreneurs have checkpoints?

: No, KPP is not assigned to entrepreneurs. It is assigned only to legal entities m clause 1 of the Order; forms No. 1-1-Accounting, No. 2-3-Accounting, approved. By Order of the Federal Tax Service of Russia dated December 1, 2006 No. SAE-3-09/826@.

When issuing a payment order in which the payee is an entrepreneur, the “Checkpoint (103)” field is not filled in I clause 2.10 of the Regulations on non-cash payments in the Russian Federation, approved. Bank of Russia 03.10.2002 No. 2-P. However, if your bank asks you to fill in this detail, you can enter 0.

The largest taxpayers are assigned an additional checkpoint

A.G. Efimova, Moscow

We noticed that in the invoices issued by our counterparty, the checkpoint has changed - it used to start at 7701, and now at 9971. But it indicates the same address as before. What could this mean? Will this cause us to have problems with deducting input VAT on such invoices?

: The new checkpoint means that your counterparty has acquired the status of the largest taxpayer. And such taxpayers are registered with one of the Interregional Inspectorates for the largest taxpayers and are assigned an additional CP P clause 1 art. 83 Tax Code of the Russian Federation; Order of the Ministry of Finance of Russia dated July 11, 2005 No. 85n; clause 5 of the Criteria... approved. By Order of the Federal Tax Service of Russia dated May 16, 2007 No. MM-3-06/308@. Thus, they have two checkpoints: at the place of registration as the largest taxpayer and at the location.

Interregional inspectorates for the largest taxpayers have a code in which the first two digits are 99, and the next two digits indicate the inspection number (for example, 9971, as in your case, - Interregional Inspectorate of the Federal Tax Service for the largest taxpayers No. 1, 9972 - Interregional Inspectorate of the Federal Tax Service for the largest taxpayers taxpayers No. 2, etc. )Classifier “Tax Authorities Designation System” (SONO).

The Ministry of Finance recommends that invoices indicate the checkpoint assigned to the taxpayer as the largest. True, if your supplier indicates in the documents the checkpoint assigned to him at his location, this will not be considered a violation m Letter of the Ministry of Finance of Russia dated May 14, 2007 No. 03-01-10/4-96. And you shouldn’t have any problems with VAT deduction anyway. O clause 2 art. 169 Tax Code of the Russian Federation.

This situation often arises in practice. The company has a separate division in the region. And the tax office claims that there can be two checkpoints for separate divisions. Is this possible? The answer is in the article.

- From this article you will learn:

- A separate unit may have two checkpoints. For example, one for UTII, the second for personal income tax. This does not contradict the Tax Code

- How to report on different taxes and which checkpoint to indicate in different declarations

What does checkpoint mean for separate units

When registering simultaneously with the TIN, the organization is assigned a checkpoint.

KPP is the reason code for registration. It reflects the grounds for registration. It consists of nine characters and has the following structure:

The first four characters (NNNN) are the inspection code:

- or by location of the organization;

- or at the location of its separate division;

- or by location of the organization’s real estate and transport;

- or on other grounds provided for by the Tax Code.

For example, code 7726 means that the company was registered with the Federal Tax Service No. 26 for Moscow.

PP (two characters) - reason for registration (recording of information). This can be a capital letter of the Latin alphabet from A to Z. Or a number:

- for a Russian organization from 01 to 50;

- for a foreign organization from 51 to 99.

Thus, a Russian organization is assigned the code:

- 01 - when registering an organization at its location;

- 43 - according to the location of the branch.

- 44 - by location of the representative office;

- 45 - at the location of a separate unit;

- 50 - for the largest taxpayers.

XXX (three characters) - serial number of registration on the appropriate basis.

The checkpoint, unlike the tax identification number, may change. Let’s say that if an organization moves and the new address is in the territory of another inspection, the organization will be assigned a new checkpoint. The same applies to a separate unit.

The inspection reflects the checkpoint for separate divisions in the Unified State Register of Legal Entities (Unified State Register of Legal Entities). And also in the certificate and in the notice of registration.

The organization is obliged to indicate the checkpoint:

- in tax returns and calculations;

- in payment orders;

- in invoices;

- in other documents where this detail is provided.

Please note: the checkpoint indicated in the declaration must match the code specified in the documents for payment of the corresponding tax. Attention was drawn to this in the letter of the Federal Tax Service dated November 11, 2014 No. BS-4-11/23216.

- Important article:

- Tax and accounting changes since 2017

Checkpoint for separate units on UTII

An organization that has the types of activities falling under the imputation is obliged to register as a UTII taxpayer. This must be done at the appropriate inspection, depending on where the company conducts such activities (clause 2 of Article 346.28 of the Tax Code of the Russian Federation).

The Federal Tax Service draws attention to the fact that an organization is registered, and not a separate division. In this case, the company submits the UTII declaration to the inspectorate where it was registered as a UTII taxpayer. And indicates the corresponding checkpoint for separate divisions - according to the location of the organization (taken from the registration certificate). Or at the place of activity (taken from the notification).

An organization may conduct imputed activities not where it is located, but in other territories under the jurisdiction of other inspections. Then she must register as a UTII taxpayer with each of these Federal Tax Service Inspectors. And submit a UTII declaration to each of them quarterly. At the same time, in categories 5 and 6 of the checkpoint, code 35 is indicated - registration of the organization as a UTII taxpayer.

This position is reflected in letters of the Federal Tax Service dated February 5, 2014 No. GD-4-3/1895, dated June 24, 2013 No. ED-4-3/11413, Ministry of Finance dated June 19, 2013 No. 03-11-09/ 23096. It is based on the provisions of the Procedure for filling out a tax return for UTII, approved by order of the Federal Tax Service dated July 4, 2014 No. ММВ-7-3/353 (see clause 3.2. Section III of the Procedure).

Checkpoint for separate divisions: personal income tax

Russian organizations - tax agents are required to transfer withheld personal income tax amounts both at their location and at the location of each separate division (clause 7 of Article 226 of the Tax Code of the Russian Federation).

A company that includes separate divisions must register with the Federal Tax Service at the location of each of its separate divisions. This is directly stated in paragraph 1 of Article 83 of the Tax Code of the Russian Federation.

The company must submit information about the income of individuals that they received from separate divisions to the inspectorate at the place of registration of these divisions. In this case, the documents must indicate the checkpoint of such a unit.

That is, information regarding the income of employees of the parent organization is submitted to the Federal Tax Service at the place of its registration. Separate divisions - to the Federal Tax Service at the place of registration of the separate division, to which personal income tax is transferred from the income of employees of separate divisions.

This position is based on the provisions of paragraph 2 of Article 230 of the Tax Code of the Russian Federation. It has been repeatedly expressed by the Federal Tax Service and the Ministry of Finance in their explanations (letters from the Federal Tax Service dated January 28, 2015 No. BS-4-11/1208, dated March 12, 2014 No. BS-4-11/4431, dated February 7, 2012 No. ED- 4-3/1838, Ministry of Finance dated April 19, 2013 No. 03-04-06/13549, dated November 22, 2012 No. 03-04-06/3-327, dated September 21, 2011 No. 03-04- 06/3-230).

Thus, a company that has a separate division and is at the same time a UTII taxpayer is registered on two different grounds. And, therefore, the fact that this unit was assigned two checkpoints does not contradict the Tax Code. The company pays personal income tax for the division according to the segregation checkpoint, and UTII - according to the imputation checkpoint.

How to find out the checkpoint of a separate division of an organization , using his TIN or an existing invoice, is useful to know for any specialist working with documents from contractors and other contractors. In our article you will find information about the decoding of this abbreviation, its meaning, the main ways in which you can find out the checkpoint of a separate unit, and what you can do with this information in the future.

Separate division - what is it? Separate division code

In paragraph 2 of Art. 11 of the Tax Code of the Russian Federation defines the concept of “separate divisions”: these are additional organizations or stationary workplaces, formed for a period exceeding 1 month, registered at an address different from the address of the parent organization.

According to Art. 55 of the Civil Code of the Russian Federation, such units may include:

- representative offices - used to represent and protect the interests of the organization;

- branches - are created for the purpose of performing the functions of a legal entity (for example, manufacturing products in a neighboring region).

Separate divisions are not registered as independent legal entities, but are considered part of a single holding or corporation. This means that the TIN and some of their other details will match. However, the checkpoints of the branches, despite the fact that all documents of the parent enterprise and its subsidiary separate divisions will indicate the same TIN, will be different.

This is indicated by the provisions of sub-clause. 3 clause 7 of the appendix to the order of the Federal Tax Service of the Russian Federation “On approval...” dated 06/29/2012 No. MMB-7-6/

The abbreviation CAT stands for “reason code”. This code is assigned only to legal entities; individual entrepreneurs who work as legal entities do not have such a code.

A checkpoint is required in the following situations:

- when participating in tenders and concluding contracts with state and municipal customers - the presence of a code in this case is a prerequisite for approval of the potential contractor’s application by the competition commission;

- when preparing tax and accounting documentation - many forms of accounting and reporting are unified, so the presence of a checkpoint, among other details, is also mandatory.

The use of gearbox allows:

- identify an enterprise in several classification systems at once, formed according to various criteria (i.e., simultaneously determine both the region in which it operates and the scope of its activities);

- simplify the procedure for maintaining accounting and tax records.

Deciphering the checkpoint of a separate unit

Knowledge of the checkpoint allows you to obtain a number of information confirming the integrity of the supplier and protect the organization from concluding a contract with a fly-by-night company. This code, in accordance with clause 5 of the appendix to order No. MMB-7-6/, consists of 9 numeric characters, which are a combination of 3 combinations, each of which carries certain information:

- the first four numbers indicate the code of the tax service that registered the legal entity and registered it (the first 2 digits in it correspond to the code assigned to the region in which the inspectorate is located, and the next 2 to the number of the specified government body);

- the following 2-digit combination indicates the reason why the taxpayer was registered;

- the last 3 digits are the number assigned to the unit when it was registered.

It is obvious that the checkpoints of separate divisions will not coincide even if they are located in the territory under the jurisdiction of one tax authority: due to the inclusion of the serial number of the registered division in the code, it becomes unique and simply cannot be assigned to another organization.

Assigning a checkpoint to a separate unit

The basis for assigning a code to a separate division is its tax registration at its location. After registering the division, its head will be issued a corresponding paper certificate, which, in addition to the TIN, which matches the number of the parent organization, will indicate the checkpoint assigned to this particular branch or representative office. There is no need to submit an application for the formation of a checkpoint for a new unit - the code will be generated automatically.

After the registration procedure for the unit is completed, the inspector of the territorial branch of the Federal Tax Service transfers all the necessary information (including checkpoints) to the tax service with which the parent organization is registered.

IMPORTANT! The checkpoint of a unit can be changed if it changes its legal address and moves to the territory under the jurisdiction of another inspection.

All banking organizations that provide services to the unit, as well as counterparties, must be notified of such changes.

How to find out the checkpoint of a separate division by TIN?

The division's checkpoint differs from the code assigned to the parent organization - which means that most methods for determining the checkpoint by the organization's TIN cannot be used in this case. So how to find out the checkpoint of a branch of an organization, having his TIN?

To do this you need to do the following:

- Determine the exact name of the organization using the tax service located at: egrul.nalog.ru. To obtain the necessary information, simply enter the TIN of the legal entity in the window that opens.

- Create a request for an extract from the Unified State Register of Legal Entities using one of the following methods:

- using the service offered by the Federal Tax Service, for which you need to go to the address: service.nalog.ru/vyp and order an extract from the Unified State Register of Legal Entities in electronic form absolutely free of charge (the document is generated within a day from the moment the request is submitted and is available for downloading for 5 days).

- by personally visiting the territorial office of the Federal Tax Service and leaving a request for the preparation of a document.

In addition, on the Internet you can find a considerable number of services that provide services for online determination of checkpoints by TIN for a fee. At the same time, free and demo versions, as a rule, allow you to find out the checkpoint only of the parent organization (such information can also be obtained on the official website of the tax service).

Only some versions of specialized commercial software have the option to determine the checkpoint of a separate unit.

Another way to determine the checkpoint is to create a query in a search engine indicating the organization’s TIN. As a rule, the pages that appear in the results contain the required information, but it is worth remembering that the information on them is not updated with the same frequency as the tax service databases, so the information found may not be current.

How to find a checkpoint in documents (for example, an invoice) of a separate division

An invoice is one of the most important tax documents, which certifies the fact of shipment of goods (provision of services), and also contains information about its cost. It contains information about the name and details of both parties to the concluded agreement, so it will not be difficult to find the checkpoint of a separate unit in this document.

In accordance with the explanations given by the Ministry of Finance of the Russian Federation in the letter “On the preparation of invoices...” dated 04/03/2012 No. 03-07-09/32, when forming this document by separate divisions, the checkpoint of the division, and not the parent organization, is indicated in line 26. This means that you can obtain the most relevant and factual information by reading the invoice issued by the department of interest.

How to find out the OKPO of a separate division (representative office, branch)

The OKPO code, like the KPP, is unique for each separate division of the enterprise. In order to find out this code, you can use the service offered by Rosstat at the address: statreg.gks.ru. In the window that opens, you will need to enter the TIN of the parent company and click the “Search” button.

As a result, the system will generate a table that will indicate the names of all representative offices and branches, as well as the OKPO codes assigned to each of them.

So, the registration code is one of the details of any organization that has the status of a legal entity. If a company has separate divisions, the checkpoint of each of them (as opposed to the Taxpayer Identification Number) will be different.

It is quite difficult to find out the code of such a division if you have a TIN, since the service developed by the tax service for determining the details of a legal entity provides information related to the parent organization, and not to its branches and representative offices. Nevertheless, it is still possible to independently find out such a checkpoint by ordering an extract from the Unified State Register of Legal Entities or by studying the information reflected in the invoice issued by a separate division.

Any legal entity has its own registration data necessary to determine the place of registration with the tax office and display other individual data. Each number has its own meaning, which will help you understand many issues. The company has the right to open many additional offices and each division is registered with the tax authority and assigned a checkpoint. However, there may be many reasons for this, as well as the procedure for changing the code, its determination and identification in other tax offices.

What is a checkpoint?

checkpoint– reason code for registration. This number is assigned automatically when registering an organization in Inspectorate of the Federal Tax Service and issuing her a taxpayer identification number (TIN).

Dear reader! Our articles talk about typical ways to resolve legal issues, but each case is unique.

If you want to know how to solve exactly your problem - contact the online consultant form on the right or call by phone.

It's fast and free!

The company can register with the tax inspectorates at the place of its main activities, as well as where separate divisions and owners of vehicles and property operate. A company has the right to register for a variety of reasons, as well as choose any tax authority. All these actions are confirmed by a specific checkpoint, which means there may be several of them, but they will all be tied to one TIN.

The registration reason code is a mandatory requisite when filling out all kinds of documents, but individual entrepreneurs do not have it. This allows individual entrepreneurs to simply indicate 0 or a dash in the checkpoint column when filling out declarations.

It shows the main reason for registration with the Federal Tax Service, as well as the legal entity’s affiliation with a specific registration authority.

Why do you need to know the gearbox code?

Any large company may have several branches (separate divisions), which have different territorial affiliations, but this does not exempt them from registering with the tax office at their location.

Thus, each subsidiary will be assigned its own code, which can tell about a specific company and officially confirm the following data:

- recognize the identification of a legal entity based on a specific feature;

- determination of the fact of carrying out activities or the presence of own property on the territory;

- indicate the main place of activity of the organization and its branches in other regions.

However, to determine all these signs, you must be able to decipher the checkpoint.

Structure

- The first four digits indicate the tax authority to which the organization is a member.

- The remaining two numbers state the reason for tax registration.

- The last three numbers show how many times the organization was registered with a specific tax authority.

The main reasons for registering using a checkpoint code

Also, specific data in the checkpoint indicate the following signs:

- state the fact that the organization has its main place of accounting;

- 05 and 31-32 - indicates the presence of structural divisions and their legal form;

- availability of property in a specific territory;

- 10-29 – registered vehicles;

- 30 – the organization was not registered as an existing taxpayer;

- over 51 are large companies, including foreign ones.

Thus, the reasons that allow the organization to register are confirmed by the corresponding code.

We can summarize the following reasons for obtaining a code when registering:

- Confirmation of registration of a legal entity and its location.

- Due to a change in tax authority and registration address.

- Opening of other divisions of the company.

- Finding the office or real estate of the organization with its documentary evidence.

These are the most common reasons, but they are not the only ones. A full list of reasons for obtaining a checkpoint is discussed in the Tax Code of the Russian Federation.

How and where is it possible to find out the checkpoint of an organization by TIN

You can find out your reason code for registration, including separate divisions, in different ways:

- Using online servers and the taxpayer’s personal account, access to which can be granted by the tax office upon presentation of a passport and TIN.

- Use of the registering authority's database, but only after sending a corresponding request through an authorized representative.

- , in some cases, paid.

- Official websites of the Federal Tax Service.

You can find out for free; TIN, KPP, name of the organization, legal address and main OKVED and a number of other records.

Information is requested for a fee on all available OKVED, contact information of the director, arbitration cases, documentation, including the balance sheet.

This also includes the presence of documents confirming registration, certificates and extracts. The checkpoint is usually indicated immediately after the TIN, separated by a fraction. It is indicated in all declarations and when carrying out any financial transactions.

How to find out the checkpoint of a foreign organization?

The work of foreign companies on the territory of the Russian Federation is not prohibited. Moreover, their activities must be officially registered with the tax authority at their location. Since foreign organizations have an unofficial legal address in Russia, the tax authority can only issue them a checkpoint or KIO.

This activity accounting system allows you to maintain a single directory. When paying taxes to the state treasury, such organizations are required to use the reason for registration code.

Using this code you can determine:

- The reason for registering the foreign organization, as well as its separate divisions. The formation of the Unified Directory is carried out by the Federal Tax Service. This document contains information about the checkpoint and tax identification number, and you can only find it out here by sending the appropriate request. Other information about foreign companies is contained in the tax office at the place of registration, including: Open and closed current accounts indicating bank details and other data.

- The name of the department indicating the first four digits of the KIO.

To obtain all the necessary information about a foreign organization, including the reason code for registration, you should order an extract from the Unified State Register of Legal Entities, which can be provided by tax authorities or authorized representatives with access to the all-Russian unified directory.

The KIO directory is maintained by the Migration Service. With this code, foreign organizations can open bank accounts in the Russian Federation, work through a branch, and purchase real estate and vehicles. Also, obtaining all the necessary registration data allows you to engage in activities in Russia for more than a month.

How to find out the code of a separate division of an organization

Any large company with impressive financial turnover needs to register additional working branches in other regions. It is these subsidiaries that should be called separate divisions.

Any registration authority must accept “isolated organizations” as full-fledged organizations and assign them the appropriate checkpoint, regardless of their reflection in various organizational and administrative documents and assigned job responsibilities.

Registration of separate divisions carried out by the Federal Tax Service at its location. This type of taxpayer can register itself as a company or division.

A representative office can be registered at the most remote points from the main place of work of the parent organization, and a branch, as a rule, operates at a short distance, performing the main functions of its company. It is the first four digits of the checkpoint that will indicate the location of the registration authority, namely, a specific tax office.

All additional companies have an identical TIN, but different checkpoints depending on the code of the region of registration, determining their affiliation with a specific tax authority.

To find out the checkpoint of a specific separate unit, you must make a request to the tax authority. This information is entered into a special notice no later than five working days from the date of registration of the branch, and this document is issued to the authorized representative.

If the parent organization decides to close its branch or representative office, this must be reported in writing to the tax authority at the location of the closing company. No more than one month must pass from the date of closure.

It must be taken into account that separate divisions do not belong to independent taxpayers. All documents indicate the TIN of the main organization, but with the checkpoint of a specific representative office.

Main cases of code changes

The procedure for changing one checkpoint to another occurs if the company changes its main place of business. In this case, the TIN will remain unchanged, but the code will correspond to the new region at the location of the tax authority.

When changing the main legal address, in order to officially and correctly change the checkpoint code, you should perform a series of sequential actions:

- submit the necessary documents to the registration authority at the location of the company;

- notarize documents containing signatures of the manager;

- pick up a copy of the company's Articles of Association with the appropriate marks from the tax office, as well as a certificate of relevant changes.

- notice from the Statistical Register of the Federal State Statistics Service or view the new OKTMO code on their official website;

- notification of deregistration with the Pension Fund and the Social Insurance Fund.

Then all banks and counterparties are sent a corresponding notification about the change of legal address. The tax service must promptly notify other registration authorities of a change in the company's legal address, but it would be useful to monitor this process independently.

Is it possible for one company to have several checkpoint codes?

Companies can expand their business by opening an unlimited number of separate divisions, including branches, subsidiaries and other representative offices around the world. However, each new organization must be officially registered with the tax authority at the place of its activities.

Thus, the parent company can have as many checkpoints as it has registered the corresponding divisions.

The registration reason code data will depend on several factors:

- depending on location;

- registration of property or transport;

- specific legal form.

Thus, taxpayers who are large can register with different tax authorities at the location of the tax authority, as well as at the place of registration with the same Federal Tax Service, but as the largest taxpayer with the assignment of a second checkpoint.

The possibility of assigning each separate division or foreign organization the appropriate checkpoint allows the Federal Tax Service to monitor the activities of such companies and check the timeliness of filing tax and accounting reports. Information about the presence of a corresponding checkpoint of an organization is, as a rule, requested by the tax authority, which is required to carry out appropriate investigative measures for all or a specific separate division of the main company, to confirm the presence or absence of other branches, real estate or transport. It can show publicly available information, the structure of the company of interest, financial statements and a number of other important indicators.

Organizations, in turn, can fully conduct their activities in different regions, quite legally, receiving systematic profits and competently controlling their business.