Organizational and economic characteristics of the enterprise

The private trade unitary enterprise ChTUP "Stolinopttorg" of the Stolin District Consumer Society was created in accordance with decision No. 1038 of November 9, 1999. Location: 225520 r.p. Rechitsa, Stolin district, Brest region, st. Polevaya, 1.

The authorized capital of the enterprise ChTUP "Stolinopttorg" is 270,000,000 rubles. The authorized capital is formed by the Owner by depositing funds into the account. In order to carry out the economic activities of the enterprise, the owner transfers to economic management the property, which consists of fixed and working capital, as well as other valuables, the value of which is reflected in the balance sheet. The property of the Enterprise is the property of the Stolin District Consumer Society, belongs to the enterprise with the right of full economic management, is indivisible and cannot be distributed among contributions (shares, shares), including among employees.

Property is formed due to:

1. authorized capital;

2. income received from the sale of products, works, services, as well as from other types of economic activities;

3. bank loans;

4. gratuitous and charitable contributions, donations from enterprises, institutions, organizations and citizens;

5. income from securities;

6. other sources not prohibited by legislative acts of the Republic of Belarus.

The enterprise operates on the principles of economic accounting and is a legal entity under the legislation of the Republic of Belarus.

It has separate property, an independent balance sheet, settlement (No. 3012000001203) and other accounts in banking institutions, a round seal with its name and with the image of the State Emblem of the Republic of Belarus, stamps with its name and other details of a legal entity.

The main goal of the enterprise is economic activity aimed at generating profit to satisfy the social, economic and cultural interests of the Owner and members of the workforce

The enterprise carries out the following types of economic activities:

Retail trade of food products, drinks and tobacco products in specialized stores;

Retail trade in tents and markets;

Wholesale trade in household electrical goods, radio and television equipment;

Wholesale trade in ceramics and glass products, wallpaper, cleaning products and;

Wholesale trade of fruits and vegetables;

Other retail trade in stores;

Wholesale trade of textile goods;

Wholesale trade of clothing and footwear;

Wholesale trade in perfumes and cosmetics.

Activities that require special permits (licenses) are carried out if the enterprise has the appropriate permits in the prescribed manner.

The total number of employees of ChTUP “Stolinopttorg” is 128 people, including:

management team 35 people

employees 8 people

Workers 85 people

The enterprise is managed in accordance with current legislation and this Charter on the basis of a combination of the rights and interests of the Owner.

The management body of the enterprise is the director, who is hired by the Owner under a contract from among persons with the necessary qualifications.

The director independently resolves all issues related to the activities of the enterprise, with the exception of legislation or the Charter within the competence of the Owner.

The director of an enterprise acts without a power of attorney on behalf of the enterprise, represents its interests, disposes of the property and funds of the enterprise within the limits of the rights established by the Owner, enters into contracts (including labor, credit, collateral), issues powers of attorney, opens current and other accounts in banks, approves fines, issues orders and gives instructions, which are mandatory for all employees of the enterprise. The conclusion of lease agreements with the right to buy, guarantees, sureties, pledges, and joint activities is carried out by the Director after receiving the consent of the Stolin Regional Pool.

The director bears, within the limits of his powers, full responsibility for the activities of the enterprise, ensuring the safety of inventory, cash and other property of the enterprise.

The director's responsibility to the Owner is established in the contract.

At this enterprise, a linear management structure predominates. (Appendix No. 2). It is characterized by the fact that at the head of each structural unit is the head of the enterprise, Vabishchevich N.G., who supervises the employees subordinate to him. The structure can be chosen and understood only with a broad, integrated approach to changes in the enterprise and its environment. Experience shows that the process of making adjustments to the organizational management structure should include:

· Systematic analysis of the functioning of the organization and its environment in order to identify problem areas. The analysis may be based on a comparison of competing or related organizations representing other areas of economic activity;

· Development of a master plan for improving the organizational structure;

· Guarantee that the innovation program contains the simplest and most specific proposals for change;

· Consistent implementation of planned changes. Introducing minor changes has a greater chance of success than major changes;

· Encouraging employees to become more aware, which will enable them to better appreciate their ownership and therefore increase their ownership of the intended changes.

Characteristics of the material and technical base of the enterprise ChTUP "Stolinopttorg".

The fixed assets of the trading enterprise ChTUP "Stolinopttorg" are a set of tangible assets created by social labor, long-term participating in the production process in an unchanged natural form and transferring their value to manufactured products in parts as they wear out.

Despite the fact that non-production fixed assets do not have any direct impact on the volume of production or the growth of labor productivity, a constant increase in these funds is associated with an improvement in the well-being of the enterprise’s employees, an increase in the material and cultural standard of their lives, which ultimately affects the results of activities enterprises.

Fixed funds are the most important and predominant part of all funds in trading. They determine the production capacity of enterprises, characterize their technical equipment, and are directly related to labor productivity, mechanization, production automation, production costs, profits and profitability levels.

The ratio of individual groups of fixed assets in their total volume represents the type (production) structure of fixed assets. Depending on their direct participation in the production process, production fixed assets are divided into: active (serve critical areas of production and characterize the production capabilities of the enterprise) and passive (buildings, structures, equipment that ensure the normal functioning of the active elements of fixed assets).

Basically, the mass of production fixed assets at ChTUP "Stolinopttorg" is concentrated in the passive part. The type structure of fixed assets is different in trading enterprises. (Appendix No. 3)

The composition and structure of fixed assets depend on the characteristics of the industry's specialization, technology and organization of production, and technical equipment. The structure of fixed assets may vary among trading enterprises. As can be seen from table No. 2, the structure of the private unitary enterprise “Stolinopttorg” has changed in one year. Buildings decreased by 6.14%, structures by 0.87%, transmission equipment by 0.18%, machinery and equipment increased by 7.27%, etc.

Fixed assets of the enterprises of ChTUP "Stolinopttorg", accounted for in monetary terms, represent fixed assets. The monetary value of fixed assets is reflected in accounting at initial and residual values.

1. In everyday practice, PFs are accounted for and planned at their original cost. It represents the cost of acquiring or creating a PF. Machinery and equipment are accepted onto the balance sheet of the enterprise at the price of their acquisition, including the wholesale price of this type of labor, delivery costs and other procurement costs, installation and installation costs. The initial cost of buildings, structures and transmission devices is the estimated cost of their creation, including the cost of construction and installation work and all other costs associated with the work to put this facility into operation. All expenses associated with the creation of a PF are carried out in current prices.

Over time, PF on the enterprise’s balance sheet are accounted for using a mixed estimate, i.e. at current prices and tariffs of the year of their creation or acquisition, the validity of the PF.

Valuation of fixed assets at historical cost is needed to determine the amount of fixed assets assigned to a given enterprise. Based on the original cost, depreciation is calculated, as well as indicators of the use of funds.

2. Replacement cost expresses the cost of reproduction of PF at the time of their revaluation, that is, it reflects the costs of acquiring and creating means of labor in prices, tariffs, etc., valid during the period of their revaluation of their reproduction, taking into account

To determine replacement cost, fixed assets are regularly revalued using two main methods: 1) by indexing their book value, 2) by direct recalculation of book value in relation to prices prevailing on January 1 of the next year. With their help, it is possible to achieve a uniform assessment of industrial fixed assets in accordance with the modern cost of their restoration, which makes it possible to more accurately establish wholesale prices for means of production and lending for capital investments.

3. The full cost of fixed assets (book value) is calculated without taking into account the cost that is transferred in parts to finished products.

4. Residual value is the difference between the original cost and accrued depreciation (the cost of the fixed assets is not transferred to the finished product). It allows you to judge the degree of wear and tear of labor equipment and plan the renewal and repair of the equipment. There are two types of residual value: 1) it is determined by the original cost, determined as depreciation is calculated, 2) by the replacement cost, determined by expert means in the process of revaluation of the means of labor.

Fixed production assets, participating in the production process, transfer their value in parts to the manufactured products sold or services provided. The monetary expression of the transferred part of the cost of fixed assets is called depreciation. It is carried out to accumulate the necessary funds for the subsequent restoration and reproduction of fixed assets. Depreciation charges are included in the cost of products and are realized when they are sold. The amount of depreciation charges (as a percentage of the book value of fixed assets) represents the depreciation rate (set on the basis of cost recovery and accumulation of funds for their subsequent full or partial restoration). The depreciation rate represents the ratio of the annual depreciation amount to the original cost of any instrument of labor, expressed as a percentage and calculated using the formula:

Na = (Fb – Fl)/ (Fb * Tn)*100

where Fb is the book value,

Fl - liquidation value,

Tn - standard service life of labor equipment.

The level of depreciation depends on each component of this formula, but the main value is the standard service life of the means of labor. The lower limit Na is the period of wear and tear of labor tools, at which subsequent major repairs become unnecessary. The upper limit Na is determined by the shortest service life of the asset, at which the economic effect of replacing existing assets with new ones exceeds the efficiency of their modernization and repair.

Labor resources of the enterprise ChTUP "Stolinopttorg" and their characteristics.

Labor resources include that part of the population that has the necessary physical data, knowledge and labor skills in the relevant industry. A sufficient supply of enterprises with the necessary labor resources, their rational use, and a high level of labor productivity are of great importance for increasing production volumes and increasing production efficiency. In particular, the volume and timeliness of all work, the efficiency of using equipment, machines, mechanisms, and, as a result, the volume of production, its cost, profit and a number of other economic indicators depend on the enterprise’s supply of labor resources and the efficiency of their use.

The analysis of economic activity plays an important role in improving the organization of wages, ensuring its direct dependence on the quantity and quality of labor, and final production results. In the process of analysis, reserves are identified to create the necessary resources for growth and improvement of wages, the introduction of progressive forms of remuneration for workers, and systematic control over the level of labor and consumption is ensured.

The main objectives of personnel dynamics are the following:

study and assessment of the provision of the enterprise and its structural divisions with labor resources as a whole;

determination and study of staff turnover indicators;

The provision of an enterprise with labor resources is determined by comparing the actual number of workers by category and profession with the planned need. Particular attention is paid to the analysis of the enterprise's supply of personnel in the most important professions. It is also necessary to analyze the qualitative composition of labor resources by qualification. (Appendix No. 4)

After calculating the structure of the enterprise, ChTUP Stolinopttorg, it is clear that the number of the enterprise changed over three years from 2004 to 2005 by 1 person (due to an increase in the staff of loaders), and from 2005 to 2006 it decreased by three people (due to the decrease of two specialists and one worker).

All leading specialists have higher education (mostly the Gomel Cooperative Institute), but some commodity experts have secondary specialized education. (Appendix No. 5)

First of all, what is striking is that throughout the analyzed years the company operated with a personnel shortage of about 1.5%. This was the result of an ill-conceived personnel policy of the enterprise, and was often caused artificially by the staff themselves, since the ability to perform a larger volume of work made it possible to earn more. This fact suggests that the planned number of personnel is overestimated due to erroneous standardization of production indicators for workers and employees.

Since the enterprise ChTUP “Stolinopttorg” is quite young, it is pleasant to note the emerging trend towards stabilization of personnel and screening out random people, this is evidenced by the coefficient of permanence of the enterprise’s personnel, which has increased by 0.015. After 2005, which was marked by strong personnel changes, in 2006 stabilization was achieved in all indicators: the turnover ratio for retirement decreased by 0.015, and the staff turnover rate by 0.012.

It is also important to note that the management of the enterprise drew conclusions from the wave of layoffs that swept in 2006 (and the bulk of those who left were experienced specialists who had been working since the founding of the enterprise and were tired of empty promises and work based on sheer enthusiasm).

Incentives for labor remuneration at the enterprise ChTUP "Stolinopttorg" are regulated by the "Regulations on the remuneration of workers of the private unitary enterprise "Stolinopttorg" for 2005." The regulations were developed on the basis of the labor code and normative legislative acts, approved by the director of the enterprise Vabishchevich N.G. The regulation includes six sections.

Monthly tariff rates and official salaries of employees are calculated on the basis of tariff coefficients of a unified tariff schedule, multiples of the tariff schedule of category I, taking into account specific professional qualification categories and categories of employees. The size of the first category tariff rate is established by the Board of the Belkoopsoyuz together with the Republic of Kazakhstan of the Belarusian Trade Union of Consumer Cooperation Workers.

Remuneration of engineers, specialists, employees:

Directors, deputy director, ch. accountant, deputy Ch. accountant, accountants, ch. CPR specialist, Ch. economist, economist, price economists, commodity experts, mechanics, dispatcher, human resources specialist, forwarders, secretary-driver, expedition storekeeper;

Workers: loaders, computer operators, machinery drivers, car drivers, salespeople, storekeepers - are paid according to a piece-rate wage system.

Payment for commodity experts and materially responsible persons of warehouses is made at piece rates for the actual gross turnover of the warehouse (without a commodity expert for construction goods and retail).

Payment to commodity experts and materially responsible persons of the container warehouse is made at piece rates for the actual turnover of the warehouse. Payment for the merchandiser for construction goods and retail is made at piece rates for the total gross volume of trade turnover (retail trade turnover of the stores of the private unitary enterprise “Stolinopttorg” and gross wholesale warehouse turnover of warehouse No. 4 “construction goods”).

Payment to sellers is made at piece rates for the actual turnover (retail and wholesale) of the store.

Loaders are paid at piece rates for loading and unloading operations. Piece prices are adjusted for increases in tariff rates.

Payment for all other specialists, engineering and technical personnel, and workers is made at piece rates for the actual total volume of turnover of PUE "Stolinopttorg" (gross wholesale and warehouse turnover and retail turnover of 3 retail enterprises of PUE "Stolinopttorg").

Payment for the driver of a car during routine repairs of a car is made from the current rate (salary) of a third-class mechanic.

In order to strengthen the role of tariff rates and official salaries in stimulating highly productive and high-quality work, the director has the right to increase the official salaries of engineers, specialists and employees by up to 7%.

In order to be interested in increasing the volume of activity, gross income, increasing labor productivity, improving the economic efficiency of the organization of engineering and technical personnel, specialists, computer operators, forwarders, secretary-typist and market controller should pay according to standards based on gross income in the sectors of activity with subsequent adjustment to the level of costs accepted for calculating taxable profit.

In case of temporary substitution, a replacement employee, including a full-time deputy head of an organization, structural unit (department, section, service), is paid according to the approved piece rate for the replaced employee. The replacement employee's payment cannot be lower than the earnings from the previous job.

In case of failure to meet production standards, defects, downtime through no fault of the employee, wages (excluding additional payments, allowances, bonuses, indexation amounts) cannot be lower than 2/3 of the tariff rate (salary) established for him. If production standards are not met due to the fault of the employee, payment is made for the actual work performed.

The accrued wages for a month for an employee who has fully worked the standard working time during this period and fulfilled the standard of work (labor duties) cannot be lower than the established minimum wage. The minimum wage takes into account all additional incentive payments, and does not take into account additional compensatory payments for special working conditions.

During the initial vocational training of persons admitted to the organization for blue-collar professions, their wages are paid in the amount of the first category tariff rate in force in the organization.

In order to increase the material interest of workers in achieving high work results based on professional excellence, performing work with a smaller number of workers, ensuring proper compensation for work in unfavorable working conditions, securing personnel in the consumer cooperation system, the following types of additional payments and allowances are established: Additional payments for combining professions ( positions), expansion of service areas (increase in the volume of work performed). Additional payments for combining professions (positions), expanding service areas, increasing the volume of work performed are established for employees belonging to the same or different categories of personnel in the amount of no more than 50% per employee.

Additional payment for night work is set at 40% of the hourly tariff rate for each hour of night work from 10 pm to 6 am for the following categories of workers:

Refrigeration unit operator;

Boiler room operator (stoker);

To the watchmen.

Additional payment for performing, along with his main job, the duties of a temporarily absent employee. Additional payments are established for workers, specialists and employees within the tariff rate (salary) of the absent employee, based on the actual volume of work performed for him. The additional payment per employee should not exceed 50% of the official salary (tariff rate) for the main job.

Additional payments to employees engaged in work with unfavorable working conditions are established based on the first category tariff rate in force in the organization for each hour of work in these conditions, taking into account the degree of severity and harmfulness of the work:

Refrigeration unit operator – 0.25

Boiler room operator (stoker) – 0.20

Electric car driver – 0.14

Secretary-typist – 0.20

Accountant – 0.20

Commodity specialist – 0.14

Economist – 0.14

Computer operator – 0.20

Allowances for high creative and production achievements in work, complexity and intensity of work, as well as for performing particularly important (urgent) work during the period of their implementation are established for engineers, specialists and employees in the amount of up to 50% of the employee’s official salary.

Bonuses for production achievements, complexity and intensity of work are paid monthly, upon achieving an optimal level of profitability as a whole for the base of not less than 1% and a growth rate of trade turnover in comparable prices compared to the corresponding period of the last year of not less than 100%.

Supplements to official salaries (rates) for length of service in the consumer cooperation system are established for all categories of employees in the following amounts:

from 1 to 5 years – 5%

from 5 to 10 years – 10%

from 10 to 15 years – 15%

over 15 years – 20% of the official salary (tariff rate) for the time actually worked. The allowance is calculated based on the official salary (tariff rate) without taking into account other additional payments, allowances, as well as bonuses and other incentive payments.

The main indicators of bonuses in the organization are:

· providing forecast parameters for the growth of volume indicators (wholesale, warehouse, retail turnover) for the month compared to the corresponding period of last year in comparable prices;

· profitable operation of the organization per month.

Bonuses for engineers, workers, employees (deputy director, chief accountant, deputy chief accountant, accountants, chief economist, chief CPR specialist, economist, price economists, HR specialist, commodity expert-economist, commodity expert-organizer , mechanic, computer operator, forwarder, machine driver, vehicle driver, dispatcher, secretary-typist, expedition storekeeper, market controller, refrigeration unit operators), commodity experts, financially responsible persons, loaders of warehouse No. 6 (packaging) is made for fulfilling the following indicators :

Ensuring the growth rate of gross wholesale and warehouse turnover in the reporting month compared to the corresponding month of the previous year in comparable prices:

from 100 to PTR (111.5%) in wholesale – 5%

from PTR and above - 10%

Ensuring the growth rate of retail trade turnover in the reporting month compared to the corresponding month of the previous year in comparable prices:

from 100 to PTR (111.5%) in retail – 5%

from PTR and above - 10%

Profitability level for the entire database:

from 0.1 to 0.5 - 2.5%

from 0.5 to 1.0 - 5%

from 1 and above - 10%.

Materially responsible persons of warehouses, commodity experts of these warehouses:

· ensuring the growth rate of gross turnover of the warehouse in comparable prices compared to the corresponding month of last year

from 100 to PTR (111.5%) in wholesale – 10%

from PTR and above - 20%

· profitable warehouse operation

from 0.1 to 0.5 - 2.5%

from 0.5 to 1.0 - 5%

from 1 and above - 10%.

For store sellers:

· ensuring the growth rate of retail trade turnover in the reporting month compared to the corresponding month of the previous year in comparable prices.

From 100 to PTR (111.5%) – 10%

from PTR and above - 20%

· profitable store operation

from 0.1 to 0.5 - 2.5%

from 0.5 to 1.0 - 5%

from 1 and above - 10%.

Commodity expert for construction goods and retail:

· ensuring the growth rate in comparable prices of wholesale warehouse turnover of warehouse No. 4 (store goods) compared to the corresponding month of last year

from 100 to PTR (111.5%) – 5%

from PTR and above - 10%

· ensuring the growth rate of retail turnover in comparable prices compared to the corresponding month of last year by three stores of the private unitary enterprise “Stolinopttorg”.

From 100 to PTR (111.5%) in retail – 5%

· from PTR and above - 10%

· profitable operation of three stores and warehouse No. 4 (construction goods).

From 0.1 to 0.5 - 2.5%

from 0.5 to 1.0 - 5%

Faculty of Economics

Department of Accounting and Auditing

Department of Informatics and Computer Engineering

REPORT

About the industrial practice of a fifth-year student (group No. B-51)

Faculty of Economics

Roslyakova L. A.

Passed industrial practice

In the private enterprise “Askon”, Akimovsky district, Zaporozhye region

Head of Production Practice,

Chief accountant of PE "Askon"________ Shevchenko E. G.

Heads of practice from the university,

The report was submitted to the department “__”____________2010.

The report was verified and approved for defense “__”____________2010.

The defense took place “__”____________2010.

Simferopol, 2010

Diary of internship at PE "Askon"

Feedback on student activities

Student feedback on internship

1 Brief description of the private enterprise “Askon” of the Akimovsky district of the Zaporozhye region……………………………………………………………………………….....3

2 State of the computer base of the Askon private enterprise………………………...…..8

3 Organization of the accounting system in the private enterprise “Askon”…………12

4 Internal regulatory support for accounting of PE “Askon”…………………………………………………………………………………15

5 Features of the organization of management and tax accounting of private enterprise "Askon"…………………………………………………………………………………......17

6 Technology for processing and storing documents PE “Askon”.........20

7 Organization of remuneration in the private enterprise “Askon”………………………….....22

8 Assessing the performance of accounting employees, the qualifications of accountants and its assessment in the private enterprise “Askon”………………………………….…..…23

9 Organization and conduct of annual inventory in the private enterprise "Askon"...24

10 Organization and procedure for closing accounting accounts in the private enterprise “Askon”………………………………………………………………………………………......29

11 Organization of preparation and submission of annual accounting, statistical and tax reporting in the private enterprise “Askon”…………………..….32

12 Proposals for improving automated accounting technology………………………………….…………..35

Applications……………………………………………………………..…………..36

1 Brief description of the private enterprise “Askon”, Akimovsky district, Zaporozhye region

The private enterprise Askon was created in 1994 on an area of 950 hectares. The enterprise has excellent conditions for infrastructure development (transport, communications, energy and water supply). The location of the railway (2 km), the city of Melitopol (25 km), the presence of motor transport, paved roads to all production departments ensures the timely supply of raw materials and dispatch of finished products for storage in our own warehouses.

The main indicators of the size of the Askon private enterprise are: the cost of gross output, marketable products and area of farmland. Indirect indicators include: the average annual cost of fixed assets, the average annual number of employees and the number of animals. In order to consider these indicators of the Askon private enterprise, let us turn to the following table.

Table 1.1 – Dynamics of indicators of the size of the private enterprise “Askon” of the Akimovsky district of the Zaporozhye region

After the analysis carried out during 2007-2009, we see that the greatest changes occurred in the animal population indicator - it decreased by 88.3% by 2009, because the Askon private enterprise decided to fully implement them by the end of 2009 (Calculations of conversion to conditional heads are given in Appendix 2). Consequently, by 2009, significant changes had occurred in the average annual number of workers employed in agricultural production - it decreased by 54.2%. And the average annual cost of fixed assets increased by 114.2% or UAH 4851.7 thousand. due to the political situation in Ukraine.

When comparing the cost of gross output and commercial output, we see that commercial output is greater. For example, in 2009 by 4640.1 thousand UAH, because they began to sell products at higher prices than in 2005. This happened under the influence of many factors, such as: increased gas prices, increased taxes, etc.

Specialization is the concentration of an enterprise’s activities on relatively narrow areas or types of products. Let's study the specialization of the Askon private enterprise.

Table 1.2 – Composition, size and structure of commercial products of private enterprise "Askon" Akimovsky district, Zaporozhye region

|

Types of products or industries |

Average over 3 years |

||||||

|

Crop production |

|||||||

|

Winter wheat |

|||||||

|

Corn for grain |

|||||||

|

Spring barley |

|||||||

|

Winter barley |

|||||||

|

Other grains |

|||||||

|

Sunflower |

|||||||

|

Winter rapeseed |

|||||||

|

Spring rape |

|||||||

|

Vegetables open |

|||||||

|

Melons |

|||||||

|

Other crop products |

|||||||

|

Total for crop production |

|||||||

|

Livestock |

|||||||

|

Pig meat |

|||||||

|

Other livestock products |

|||||||

|

Total livestock |

|||||||

|

Industrial products |

|||||||

|

Sales of other products, works and services |

|||||||

|

Household total |

Analyzing the data in Table 2.2, it is possible to identify the main industry of this enterprise - crop production, since in 2009 it occupied 65.7% of total revenue or 10260.1 thousand UAH. An additional industry is industrial products, its share in total revenue is 17.0%. The largest share of revenue in crop production is winter wheat (36.60% in 2009). Consequently, the intra-industry specialization of the Askon private enterprise is grain.

Let's consider the organizational structure of the Askon private enterprise.

|

Figure 1.1 - Organizational structure of PE "Askon" as of 01/01/09.

Therefore, this enterprise is medium in size. This is evidenced by the fact that it includes the following divisions: a crop production department, a garage, a power plant, a mechanical workshop and a warehouse. Until 2007, there was also a livestock department, but since keeping animals was not profitable, they were sold.

2 State of the computer base of the Askon private enterprise

Computer support is an integral part of effective work at Askon Private Enterprise. Computers in an enterprise provide invaluable assistance. They appeared in the Askon private enterprise in 2002. Currently, the accounting department of this enterprise has 7 computers, 5 of which are Pentium III models, and the remaining 2 are Pentium IV models.

The Pentium III processor handles today's workloads with the versatility and compatibility to support a wide range of applications. Researching data dependencies between commands allows you to organize the execution of commands in the optimal sequence. Ensures that the processor's superscalar computation blocks are always loaded in an optimal order and improves overall performance. In this processor The thermal sensor allows the system to actively manage thermal conditions, error monitoring and correction helps protect mission-critical data, functional redundancy control serves to confirm the integrity of calculations, the system control bus is used for efficient communication between the thermal sensor, P.I. ROM of the processor, and the rest of the system components, accessible at the software level The processor serial number function is used for identification and registration purposes.

Pentium IV allows you to simultaneously execute two streams of commands (two parts of the program), which improves the efficiency of running individual applications and working in multitasking environments, provides significant performance gains, accelerating access to frequently used data and commands, when used in personal computing systems and for providing any computing needs. Floating point acceleration enhances 3D display capabilities and graphics-intensive scientific calculations.

The Askon private enterprise has a local network that connects 7 computers. It is convenient in that computers can exchange various information and data necessary for the formation of any accounting registers, as well as for monitoring the activities of each employee. Computers are connected to each other using copper conductors - twisted pair. Twisted pair consists of “pairs” of wires twisted around each other and at the same time twisted around other pairs, within the same shell.

Also, employees of the Askon private enterprise have access to the global Internet. The provider is Ukrtelecom, which provides the user with a huge range of services. The service is promoted under the OGO brand.

Connection to the Internet is carried out using radio access - Radio Ethernet. The advantages of this connection method are: high speed of information transfer - up to 11 Mbit/sec; high noise immunity due to data redundancy in the radio channel; communication quality that is practically independent of weather conditions; high confidentiality of data transfer. The company has its own WEB site: askon. org. ua

From application software, the enterprise uses Microsoft Office Word (for creating letters, reports, web pages), Microsoft Office Excel (allows you to perform calculations, analyze data and work with lists in tables). Specialized software is 1C: Accounting 7.7, which is a universal program for automating accounting and tax accounting, including the preparation of mandatory reporting. A comprehensive configuration, preserving all the capabilities of the 1C:Enterprise system programs (1C: Accounting, 1C: Trade and Warehouse, 1C: Salary and Personnel), provides integrated accounting, which implies:

· a unified system for maintaining regulatory and reference information;

· automatic reflection of trade and warehouse operations and payroll calculations in accounting;

· financial accounting for several legal entities;

· consolidated management accounting.

In the Askon private enterprise, one person holds the position of software engineer - Anatoly Vladimirovich Dedushev. As a rule, the programmer is the central link in the information system. His responsibilities include:

1. Develop a technology for solving a problem at all stages of information processing.

2. Select a programming language to describe algorithms and data structures.

3. Determine information to be processed by computer technology, its volume, structure, layouts and schemes for input, processing, storage and output, methods of its control.

4. Perform work on preparing programs for debugging and carry out their debugging.

5. Launch debugged programs and enter initial data determined by the conditions of the assigned tasks.

6. Carry out adjustments to the developed program based on analysis of the output data.

7. Determine the possibility of using ready-made software products.

8. Develop and implement systems for automatically checking the correctness of programs.

9. Take part in the creation of catalogs and file cabinets of standard programs, in the development of forms of documents in electronic form that are subject to computer processing, in the design of programs that allow expanding the scope of application of computer technology.

10. Ensure proper technical operation and uninterrupted operation of computers and individual devices.

11. Participate in the development of equipment maintenance and repair, measures to improve its operation, prevent downtime, improve the quality of work, and effectively use computer technology.

12. Take measures to ensure timely and high-quality repairs of computers and individual devices on your own or by third parties.

13. Protect the property of the enterprise, do not disclose information and information that is a commercial secret of the enterprise.

14. Inform management about existing shortcomings in the operation of the enterprise and measures taken to eliminate them.

In 2002, the Askon private enterprise purchased computers. In the same year, work was organized to train accounting employees in the basics of using information and communication technologies. Every 2 years, employees undergo advanced training courses in the field of information technology. And currently they are confident PC users and are proficient in such programs as: Microsoft Office Word, Microsoft Office Excel, 1C: Accounting 7.7, 1C: “Client-Bank”, “Best-Zvit”, “League Law”.

3 Organization of an accounting system in the private enterprise "Askon"

The structure of the accounting apparatus and its number depends on the volume of production, the complexity of technological processes, regulations relating to taxation, preparation and submission of reports, the state of accounts receivable and payable, the use of computers, the choice of accounting form, etc. The basis for accepting an employee in a state of emergency “ Askon" is an Employment Agreement (Appendix D). Before starting work, the employee and this enterprise draw up an Agreement on full financial liability (Appendix D).

The structure of the accounting apparatus of the Askon private enterprise is a centralized system. The advantage of centralizing accounting is that it ensures the efficient use of accounting personnel and also promotes the introduction of advanced accounting techniques. Let's look at the organizational structure of the Askon private enterprise in the following diagram.

|

Figure 3.1 – Scheme of the organizational structure of PE “Askon”

In order to regulate the activities of accounting employees, PE Askon uses job descriptions for accountants (Appendix E).

The distribution of official duties of accounting employees was carried out by the Chief Accountant - Elena Grigorievna Shevchenko. Let's consider the distribution of job responsibilities of accounting employees:

Table 3.1 – Distribution of job responsibilities between employees of the accounting apparatus of the Askon private enterprise

|

Job title |

Responsibilities |

|

Accounts receivable and payable accountant |

Execution of all salary calculations and deductions from it. Control over the use of the wage fund, settlements with other creditors. |

|

Accounting for transactions on accounts 30,31,37. |

|

|

Accountant of the material department |

Accounting for the acquisition of material assets, settlements with suppliers of materials, etc. |

|

Accountant of the production and costing department |

Cost accounting for all types of production, calculation of actual production costs, and reporting. |

|

Accountant of the financial department |

Accounting for settlements with creditors, legal entities and individuals. |

The distribution of responsibilities in the accounting department of the Askon private enterprise was carried out on a functional basis, that is, each individual employee is assigned a specific area.

Accounting at this enterprise is carried out in an automated form, which is carried out by entering correspondence accounts directly into the business transactions journal or by filling out primary accounting documents. When posting completed primary accounting documents, correspondence accounts are automatically generated. A specialized program in the accounting department of the Askon private enterprise is 1C: Accounting 7.7, which contains a large amount of regulatory and reference information, which includes documents on the organization of accounting, tax payment schemes and calendars and other data, allows you to organize multi-level analytical and synthetic accounting, work with multiple charts of accounts and multiple databases. The advantages of this form of accounting are:

1. One-time introduction of primary information.

2. Quickly providing the user with information.

3. Automatic creation of synthetic and analytical accounting registers and accounting and tax reporting forms.

4. Automatic receipt of information about deviations from established standards and norms.

5. Possibility of carrying out a large number of operations.

6. Ability to create registers for any period of time.

The quantitative composition of personnel in the Askon private enterprise is determined by the organizational and staffing structures and the charter of the enterprise. Number standards are developed depending on the labor intensity of the typical composition of the work performed and are calculated depending on the factors that have the greatest influence on their value. Total standard number ( But) accounting employees is determined by the formula:

But = N * K k.u.v.,

Where N- standard number of accounting employees, To k.u.v.- correction factor. To determine indicators N AND Kk. u.v. Standards for the number of accounting employees are used (Appendix G).

Let's calculate the total standard number for the accounting department of PE "Askon":

But= 1 * 3,8 = 3,8

A well-chosen accounting staff of a given enterprise promotes mutual understanding between employees and a favorable working atmosphere in the team.

4 Internal regulatory support for accounting of private enterprise "Askon"

The internal regulatory support for accounting in the Askon private enterprise is the regulatory documents developed by the enterprise itself.

The order on accounting policy is the main document for the accounting department of the Askon private enterprise, which establishes the rules for maintaining accounting records and, from the many options allowed by national accounting standards, clearly prescribes those that the enterprise follows in its activities (Appendix A).

The success of this enterprise is based on a well-established accounting mechanism (accounting, tax, management) of ongoing business processes.

The order on the accounting policy of PE "Askon" defines:

Materiality thresholds regarding individual accounting objects;

Granting a division of the enterprise (Kiev region, Fastovsky district, Trilisy village) the right to maintain a separate balance sheet;

Articles and rules for calculating production costs of products (works, services);

Methods of depreciation of non-current assets;

Cost characteristics of items related to low-value non-current tangible assets (MNMA);

Methods for estimating inventory loss;

Frequency of checking and adjusting the value of inventories;

List of created security for future expenses and payments;

The procedure for determining the degree of completion of work under a construction contract;

Rules for conducting inventories;

Deadline for submitting reports.

This document is a guide for accounting employees when reflecting business transactions.

The Askon private enterprise has also developed a working chart of accounts (Appendix B). A working chart of accounts is a systematized list of accounts created on the basis of the current chart of accounts approved by the Ministry of Finance of Ukraine, on which accounting is maintained in the Askon private enterprise. It contains synthetic and Analytical accounts necessary for maintaining Accounting in accordance with the requirements of timeliness and completeness of accounting and reporting, as well as a list of off-balance sheet Accounts for which there are actually accounting objects and the accounting of these objects is really necessary for Ascon Private Enterprise. Each account in the plan has a code (cipher), that is, a conventional digital value, and a name. The use of account codes makes accounting work easier and is a prerequisite for using computers. Askon PE independently approved the working chart of accounts, establishing the procedure for its application in its accounting policies.

The document flow schedule is also an internal regulatory document of the enterprise under study (Appendix B), this is the movement of documents of the Askon private enterprise in the process of their operational use and accounting processing from the moment of drawing up or receiving the document from other enterprises until transfer to storage in the archive.

5 Features of the organization of management and tax accounting of private enterprise "Askon"

Tax accounting in the Askon private enterprise is carried out for the purpose of operational control over the state of settlements with the budget and extra-budgetary funds for the tax obligations of the enterprise. It is carried out on the basis of the Law of Ukraine “On Taxation of Enterprise Profits” dated May 22, 1997 No. 283/97-BP, the Law of Ukraine “On Value Added Tax” dated April 3, 1997 No. 168/97-BP, Decree of the Cabinet of Ministers dated May 20 .93 No. 56-93 “On local taxes and fees”, Law of Ukraine “On the procedure for repaying taxpayers’ obligations to the budget and state trust funds” dated December 21, 2000 No. 2181.

The organization of tax accounting at this enterprise is carried out by the chief accountant Elena Grigorievna Shevchenko. Tax accounting in the Askon private enterprise is also automated. It is maintained using a tax chart of accounts. This chart of accounts uses letter codes, which makes it easy to visually distinguish accounting entries from tax entries. Changing them is prohibited. Accounts are clearly stated in tax accounting algorithms. Data from all tax accounts and registers is ultimately reflected in the gross income and expense accounts. Tax profit is determined based on the turnover of these tax accounts. When necessary, balance data is used to estimate tax assets and liabilities. Analytical accounting of data is organized in such a way that it reveals the procedure for forming the tax base (the procedure for forming the amounts of income and expenses, the procedure for determining the share of expenses taken into account for tax purposes in the current tax (reporting) period, the amount of the balance of expenses (losses) to be attributed to expenses in the next tax periods, the amount of debt for settlements with the budget for income tax, the procedure for forming the amounts of created reserves). Tax accounting data in the Askon private enterprise are: primary documents (Accounting statements, Accounts), analytical tax accounting registers (developed by the enterprise independently) and calculation of the tax base. Correction of errors in tax accounting registers is confirmed by the signature of the chief accountant making the correction, indicating the date and justification for the correction made, making appropriate adjustments to the accounting records. A screen form has been implemented for the Register of issued and received tax invoices, the VAT Declaration and its annexes.

Unlike financial and tax accounting, which are strictly regulated by standards and legislation, Management accounting is conducted in accordance with the information needs of the management of the Askon private enterprise. The management accounting system at the enterprise under study was introduced in order to provide the enterprise management with the most complete information necessary for effective work.

To achieve positive results, management accounting in the Askon private enterprise was established in several stages:

1. Determination of the financial structure of the enterprise by identifying centers of financial responsibility

The financial structure was created to determine which units were able to provide the necessary data. PE "Askon" has identified the following centers of responsibility in areas of activity: Administration, Information Technology, Warehouse activities, Purchasing, Sales.

2. Development of management reporting

For each responsibility center, a set of indicators must be developed that characterize the effectiveness of its activities, as well as regulations for the processing and storage of received information. To do this, the company created management reporting forms in which all data is entered (managerial balance sheet, management profit and loss report, management cash flow report).

3. Development of methods for management accounting of costs and calculation of production costs (since most of management accounting is focused on detailed accounting of production costs and calculation of production costs, to find reserves for reducing costs per unit of production).

4. Development of a management chart of accounts and a procedure for reflecting standard business transactions

5. Development of internal regulations and instructions regulating the maintenance of management accounting. (Regulations for management accounting are specified in the Order on Accounting Policies.)

The enterprise has an institution of trade secrets. Information about the activities of the private enterprise Askon, which has a certain value for the head of the enterprise, Gennady Vasilyevich Novikov, is created in the accounting system, where its protection is ensured. The list of information that is a trade secret is determined by the head of the enterprise. The trade secret of the Askon private enterprise concerns information of a financial and economic nature. An employee who allows the disclosure of this secret of the enterprise bears disciplinary liability in accordance with labor legislation.

6 Technology for processing and storing documents PE "Askon"

Documenting business transactions in the Askon private enterprise is primary accounting, which includes the processing and movement of primary documents before submitting them to the archive. The basis for any entry in the accounting registers is correctly executed supporting primary accounting documents that record the facts of business transactions at a given enterprise. Primary documents are drawn up at the time of business transactions or immediately after their completion and contain all the required details, signatures of persons responsible for the content of business transactions, and the Seal of the Askon Private Enterprise. Documents are divided into internal and external. Internal documents document business transactions carried out within the enterprise. External documents come from outside and reflect business transactions that characterize relations with other organizations.

The main element of document flow is the document flow plan of the private enterprise "Askon", which establishes the rational movement of documents of the enterprise (Appendix B). All documents serving as the basis for entries in accounting are submitted to the accounting department of the enterprise in the prescribed manner by a certain date for verification in terms of the legality of the transactions reflected in them, the correctness of execution and for subsequent processing. When processing in the accounting department of the Askon private enterprise, taxation is carried out, that is, the calculation of total amounts, account assignment, that is, the affixing of correspondence accounts and their grouping. All documents received for processing are processed within one business day and after it, each document contains a note about the transfer of information to any register (Cash Book, Journal Order, Turnover Statement, General Ledger) or to an account. Information from accounting registers is transferred in grouped form to the financial statements of the given enterprise.

Primary documents, accounting registers and accounting reports must be stored in accordance with the established procedure and deadlines, that is, they are transferred to the archive of the Askon private enterprise. First, the documents are transferred to the current archive, which is organized within the accounting department, and then to the permanent archive. The current archive of this enterprise contains documentation from 2009 and the current year 2010, which is stored in locked cabinets under the responsibility of the accounts payable accountant (archivist). It is formed according to the correspondent principle, that is, according to the organizations and persons for whom they were compiled. The safety of accounting documents and their transfer to the permanent archive is ensured by Elena Grigorievna Shevchenko, chief accountant. The right of access to the archive has the head of the Askon private enterprise, the chief accountant, the archivist and the investigative authorities on the basis of the relevant resolution. The nomenclature of cases stored in the permanent archive is a systematized order of the names of cases created in the office work of a given enterprise, drawn up in the appropriate order indicating the storage periods for cases, which is compiled by the chief accountant. In the permanent archive, the files are bound, the thickness of the folder does not exceed 2 cm. The title page indicates the name of the file, the nomenclature number, and the period for which the documents are stored. And on the 2nd page the number of documents in the case, the numbers of the first and last document and the number of pages are indicated. If files are released from the archive, the archivist records this in the journal. When the period for storing a document in the archive has expired, it is written off based on the act.

7 Organization of remuneration in private enterprise "Askon"

Wages are a very important issue for the Askon private enterprise, since the effectiveness of labor management depends on its size, principles of its organization, bonuses for employees and other components. An employee’s earnings are an incentive to work and the desire to increase it forces a person to conscientiously fulfill his job duties and make efforts to achieve high performance indicators.

The company has a five-day work week from Monday to Friday and an eight-hour working day from 8-00 to 17-00 and a one-hour lunch break from 12-00 to 13-00.

The organization of remuneration for accountants is carried out according to the official salary, which was established by the head of the Askon private enterprise, Gennady Vasilyevich Novikov. The official salary of the chief accountant is set, as a rule, at the level of the salary of the deputy head of the organization and in this enterprise is 1,700 UAH. As for the accountant of the material department and the accountant of the production and costing department, their monthly tariff rate is 1100 UAH. And the official salary of an accountant for accounts receivable and payable, a cashier and an accountant in the financial department is 1,300 UAH. At the end of the year, accounting employees are paid their thirteenth salary - an excellent means of motivating staff. It takes into account the contribution of each employee to the overall result of the enterprise and helps reduce staff turnover. This is a bonus payment, the amount of which depends on the size of the employee’s salary and the duration of his continuous work at the enterprise. This bonus is paid based on the results of the calendar year (which lasts from January 1 to December 31).

8 Assessing the performance of accounting employees, the qualifications of accountants and its assessment in the Askon private enterprise

The qualitative characteristics of the personnel officers of the Askon private enterprise present a completely positive picture.

1. First of all, a high level of education: each employee has a higher education diploma.

2. An extremely high level of professional training, which is explained by the presence of specialists in the field of accounting and auditing at the enterprise.

3. Favorable age composition of accounting employees: from 27 to 45 years old, no pensioners.

4. This enterprise has low staff turnover: each accounting employee has been assigned to a specific workplace for more than 5 years, values and is proud of his work, treats it responsibly, thus, he has a long history of work at the Askon private enterprise.

5. All accountants have mastered computer software.

But there is one drawback - some accounting employees (accountant in the material department, accountant in the production and costing department and cashier) mastered accounting automation on their own.

All these factors result in the effective operation of Askon Private Enterprise.

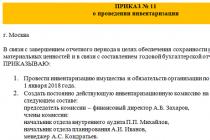

9 Organization and conduct of annual inventory in the private enterprise "Askon"

In the Askon private enterprise, as in all other enterprises, an annual inventory must be carried out once a year. Over time, even with the most careful accounting, there may be a discrepancy between accounting data and the actual presence of assets and liabilities of the enterprise. The reasons for the occurrence of such a discrepancy can be both natural processes and those artificially created due to negligence or criminal intentions of materially responsible persons and accounting employees. Only after an inventory of assets and liabilities can one say with confidence that the accounting data of the Askon private enterprise are reliable. This enterprise must carry out an inventory before drawing up annual financial statements in the period from October 1 to December 31 of the reporting year.

Before preparing the annual inventory, the Askon private enterprise determines the number of workers of the inventory commission and their composition. This issue is resolved in accordance with the number of financially responsible persons (one working commission per one financially responsible person). All materials of the enterprise are subject to inventory, regardless of its location, as well as materials in the responsible storage of the enterprise, rented tools, and materials received for processing. The minimum number of members of one working inventory commission is not defined by law, but in practice the Askon private enterprise has at least 3 people. Members of the working inventory commission can be representatives of the enterprise administration (chief accountant - Elena Grigorievna Shevchenko), accounting service employees, and other specialists (engineers, economists, agronomists, etc.). To avoid misunderstandings, the vacation schedule of the proposed members of the working inventory commissions is checked, since the absence of at least one member of the working inventory commission during the inventory serves as a basis for declaring the inventory results invalid.

Based on the order on accounting policy, the head of the enterprise, Gennady Vasilyevich Novikov, issues an order to conduct an annual inventory, indicating the start date of the inventory, its timing and the composition of the members of the commission for its implementation. In accordance with the “Instructions for the inventory of fixed assets, intangible assets, inventories, cash and documents and settlements” approved by order of the Ministry of Finance of Ukraine dated August 11, 1994 No. 69, it is the head of the Askon private enterprise who is responsible for organizing and conducting the inventory . The order is approved by the head of the enterprise and registered in the journal for recording and monitoring the implementation of orders for inventory and it reflects the following points:

The personal composition of the permanent commission, indicating its chairman and members;

The personal composition of the working inventory commissions, indicating their chairmen and members and the objects being inspected;

Composition of property subject to inventory;

The procedure and timing of inventory;

Deadlines for submitting inventory results;

Responsible persons for conducting the annual inventory.

All persons included in the order to conduct an annual inventory sign on the order familiarization sheet. The order at this enterprise is issued two weeks before the start of the inventory.

Members of the working inventory commissions of the Askon private enterprise are instructed by the chief accountant. During the briefing the following is discussed:

Methods for filling out inventory lists, the procedure for making corrections;

Legal consequences of the actions of members of working inventory commissions;

Working hours and inventory schedule;

The procedure for opening and closing facilities where inventory is carried out;

The procedure for the functioning of a temporary warehouse, the procedure for issuing and receiving materials, if necessary, for the period of inventory.

The Askon private enterprise carries out physical and documentary inventory. Physical verification is directly related to the observation of inventory objects, determining their quantity by counting, weighing, and measuring. It is used when taking inventory of fixed assets, inventories, cash, strict reporting forms, etc. To document the results of a physical inspection, inventory forms are used (Appendices I, K, L). During a documentary check, the presence of an accounting object is confirmed directly by documents. Therefore, it is used when taking inventory of accrued depreciation, intangible assets, deferred expenses, estimated reserves, financial liabilities, etc. To document the results of a documentary check, forms of inventory acts are used.

To carry out an annual inventory of the assets and liabilities of the Askon private enterprise, accounting data on their balances is required, with which their actual availability is compared. Most often, a given enterprise begins an annual inventory of certain assets and liabilities on the first day of the month (for example, October 1 or November 1). This eliminates the need for additional determination of balances based on accounting data. During the inventory process, not only the actual balances of the inventory asset are taken into account, but also its movement (issue, receipt, movement) on the basis of primary documents reflecting operations on the movement of such assets. Verification of the actual availability of inventory is carried out by mandatory recalculation, reweighing or re-measuring with the obligatory participation of financially responsible persons. For this purpose, the management of the Askon private enterprise provides the inventory commission with the necessary measuring containers, equipment for measuring, weighing, measuring, control and other instruments. Financially responsible persons transfer to Inventory commission report with all documents confirming the movement of inventory and cash. In the inventory records, with a receipt, they confirm that by the beginning of the inventory, all expenditure and receipt documents were transferred to the accounting department, the inventories received under their responsibility were capitalized, and those disposed of were written off as expenses. The accounting and actual balances of property, as well as quantitative and total discrepancies identified during the inventory between the actual availability of property and accounting data, are entered into inventory lists or standard form inventory reports, which are filled out in at least two copies. Inventory lists are signed by all members of the commission and financially responsible persons, who record that the inspection was carried out in their presence, there are no complaints against the members of the commission, and they accept the property listed in the inventory for safekeeping. If deviations from the accounting data were identified during the inventory, then matching statements are also compiled for such property. Filling out inventory lists, inventory acts and matching sheets is automated.

At the closing meeting Inventory the commission of the Askon private enterprise summarizes the results of the work carried out, the result of which is the final inventory act. The act reflects proposals for regulating those identified during Inventory discrepancies between the actual availability of valuables and accounting data.

10 Organization and procedure for closing accounting accounts in PE "Askon"

Before preparing the annual financial statements, the accounting department of the Askon private enterprise closes the accounting accounts, that is, they make entries on the accounts, as a result of which the accounting accounts have a zero balance, that is, they are closed.

In the accounting department of this enterprise, income and expense accounts are closed for the financial result, based on the working chart of accounts.

The generation of information on income and expenses received by PE "Askon" in the course of ordinary activities is carried out in the context of groups of operations included in ordinary activities: trade and production operations for the performance of work and provision of services, as well as ordinary operations not related to the main activities of the enterprise and financial transactions.

PE "Askon" is engaged in the sale of products, works and services - which are business transactions that involve the transfer of ownership rights to individual objects to another business entity in exchange for an equivalent amount or debt obligations. Synthetic accounting of the results of product sales is carried out on accounts of class 7 (income and operating results) and 9 (activity costs). In the accounting department of this enterprise, the debit of subaccount 901 “Cost of sold finished products” includes the planned cost of sold agricultural products and the costs of their sale throughout the year, and at the end of the year - the difference between the planned and actual cost of sold products. Revenue from the sale of these products (together with VAT) is reflected in the credit of subaccount 701 “Income from the sale of finished products.” The actual cost of sold work and services is included in the debit of subaccount 903 “Cost of sold work and services”, and the proceeds from their sale (together with VAT) are credited to subaccount 703 “Income from the sale of work and services”. The actual cost of other sold working capital (except for finished products) is credited to subaccount 943 “Cost of sold inventory”, and their selling price (including VAT) is credited to account 712 “Income from the sale of other current assets”. Then, at the end of the year, the account data in the Askon private enterprise is written off to account 791 “Result of operating activities” (on the debit of the income account, on the credit of account 791; on the debit of account 791, on the credit of the expenses account), and an accounting certificate is drawn up (Appendix 3 ).

Other operating income, namely: 715 “Received fines, penalties, penalties”, 717 “Income from writing off accounts payable”, 719 “Other income from operating activities”, are written off at the end of the year to account 791 “Result of operating activities” (debit income account, and the loan account is 791). Administrative expenses (account 92), sales expenses (account 93) and other operating expenses are written off to this account: 944 “Doubtful and bad debts”, 946 “Losses from depreciation of inventories”, 947 “Shortages and losses from damage to valuables”, 948 “Recognized fines, penalties, penalties”, 949 “Other operating expenses” (on the debit of the expense account, and on the credit account 791).

Other financial expenses (732 “Interest received”) and financial expenses (952 “Other financial expenses”) are written off to subaccount 792 “Result of financial transactions”. D-t 73 K-t 792; D-t 792 K-t 95.

And to subaccount 793 “Result of other ordinary activities” the following accounts are written off from other income: 742 “Income from restoration of the usefulness of assets”, 745 “Income from assets received free of charge” and 746 “Other income from ordinary activities” (D-t 74 K-t 792), and from other expenses the following accounts are written off: 972 “Losses from decrease in the usefulness of assets”, 976 “Write-off of non-current assets”, 977 “Other expenses of ordinary activities” (Dt 792 Kt 97).

Based on accounting data, the financial result of the activities of the Askon private enterprise is determined, which is an increase or decrease in the Value of Equity Capital and formed in the process of its business activities for the Reporting period. The financial result is composed of financial results from various types of activities of the enterprise and is formed on account 79 “Financial results”. Consequently, at the end of the year, account 79 is closed. The account balance is written off to account 44 (depending on the result obtained, to subaccount 441 “Retained earnings” or 442 “Uncovered loss”):

79,441 – profit as a result of activities;

442 79 – loss as a result of activities.

Profit is the excess in monetary terms of Income (revenue from goods and services) over the Costs of production and sale of these goods and services, and loss is the opposite.

Profit is one of the most important indicators of the financial results of the business activities of the Askon private enterprise, for the sake of which entrepreneurial activity is carried out.

11 Organization of the preparation and provision of annual accounting, statistical and tax reporting in the private enterprise "Askon"

In the accounting department, PE Askon prepares and submits annual accounting, statistical and tax reports to the relevant authorities.

Accounting statements – This is a unified system of data on the property and financial position of the Askon private enterprise and on the results of its economic activities, compiled on the basis of accounting data in established forms. The enterprise compiles the following forms of financial statements: balance sheet f. No. 1, financial results report f. No. 2, cash flow statement f. No. 3, statement of equity f. No. 4 and notes to the annual financial statements f. No. 5, signed by the director and chief accountant of the enterprise.

The balance sheet is compiled in order to provide users with complete, truthful and unbiased information about the financial condition of Askon Private Enterprise as of the reporting date. It reflects the assets, liabilities and equity capital of the enterprise in thousands of hryvnia (Appendix H). The purpose of drawing up a statement of financial results is to provide users with complete information about income, expenses, profits and losses from the activities of the Askon private enterprise for the reporting period (Appendix O). The cash flow statement is compiled to provide users with information about changes that have occurred in the cash resources of the enterprise being studied and their equivalents during the reporting period as a result of operating and financial activities (Appendix P). The purpose of compiling a statement of equity is to disclose information about changes in the composition of the enterprise's equity during the reporting period (Appendix P). For a comparative analysis of the information of a given enterprise, a statement of equity capital for the previous year is attached to the annual report. Notes to the financial statements are a set of indicators and explanations that provide detail and validity of the items in the financial statements, they disclose the accounting policies of the enterprise, information not provided directly in the financial statements, but which is mandatory in accordance with the relevant provisions (standards), information containing additional analysis of the items in the statements necessary for ensuring its understandability (Appendix C). These forms are submitted by the enterprise to the Department of Agriculture by February 20 after the end of the reporting period.

Statistical reporting of enterprises makes it possible to establish statistical indicators of the economic activity of the sectors of the Askon private enterprise. This enterprise produces the following forms of statistical reporting: Report on the sale of agricultural products f. No. 21-zag. (Appendix T), Information on harvesting agricultural crops f. No. 29 agricultural and Main economic indicators of agricultural enterprises f. No. 50 agricultural (Appendix U).

The basis for filling out form No. 21-zag. (annual) are warehouse receipts, invoices from the Askon private enterprise and other primary accounting documents that were received by the enterprise at the time of their preparation and confirm the sale of agricultural products of its own production. As for the statistical reporting of form No. 29 of agriculture, it reflects data on the size of the sown area, the size of the harvested area, the actual harvest in the initially recorded weight and the amount of grain and crop seeds in weight after processing. Main economic indicators of agricultural enterprises f. No. 50 agricultural reflect information on both production of products (size of harvested area, actual harvest in centners, production cost) and its sales (physical weight, production cost, total cost, revenue), costs of main production, as well as state support for agriculture (average annual number of employees and land use). These statistical reporting forms are submitted by PE Askon to the Statistics Committee before February 20 after the reporting period.

Tax reporting of private enterprise "Askon" consists of approved tax returns. Tax return is a written statement from the Askon private enterprise about income received and expenses incurred, sources of income, tax benefits and the calculated amount of tax and other data related to the calculation and payment of tax. This company provides the Tax Inspectorate with a VAT Declaration and Tax Calculation in Form 1DF.

Private enterprise "Askon", as a taxpayer, is obliged to keep separate records of transactions for the supply and purchase of goods (services), which are subject to VAT, which is reflected in the VAT Declaration. Tax calculation in form 1DF is intended for the formation and submission to the tax authorities of the calculation of the amounts of income accrued (paid) in favor of the Askon private enterprise.

Tax returns are accepted by the regulatory authority through the office until March 1 after the reporting period.

12 Proposals for improving automated accounting technology

Modern information systems are designed to improve management efficiency using information technologies for preparing and making decisions. Automation of accounting improves not only the quality of accounting, but also the quality of the business of the Askon private enterprise. The transition to automated accounting at the enterprise occurred in 2008, that is, easier processing and data preparation have been in place for 2 years. This enterprise uses the popular software product “1:C Accounting 7.7”. The main advantages of this program:

Maintaining synthetic and analytical records regarding the needs of the enterprise and drawing up all necessary reports;

The ability to maintain quantitative multivariate accounting;

Ability to supplement the Chart of Accounts and posting systems.

All employees of the Askon private enterprise work in the environment of this program, but there is a drawback - not all accounting employees are professionally trained, that is, 3 employees mastered accounting automation on their own. Therefore, it is necessary to eliminate this shortcoming. Training accountants in automation requires certain funds from the Askon private enterprise, which currently amounts to 1200 UAH.

1200 UAH * 3 employees = 3600 UAH.

Consequently, in order for the entire accounting department to work and master the “1:C Accounting 7.7” program professionally and perfectly, the private enterprise “Askon” needs to invest 3,600 UAH, which is an acceptable amount for this enterprise.

APPLICATIONS

Appendix 1

The cost of gross output in comparable prices in 2005.

|

Culture |

Comparable price 2005, UAH |

||||||

|

Crop production |

|||||||

|

Winter and spring wheat |

|||||||

|

Corn for grain |

|||||||

|

Winter and spring barley |

|||||||

|

Sunflower |

|||||||

|

Winter rapeseed |

|||||||

|

Spring rape |

|||||||

|