Russia is one of the countries where NDFL is speaking one of the most common "sources" of the budget filling. The size and volume of NFFL depend on the economic situation and the well-being of people. Let's look at how to calculate NDFL and give a few examples.

What is this tax and the area of \u200b\u200bits application?

Ndfl or taxes on the income of individuals relate to the fees that each person pays. His main feature is that the tax is closely related to the income of the individual. And it should be remembered - under the saline, they understand any person, even a child who received income taxable.

In this case, the citizenship of the NDFL payer does not matter, because the obligation to pay it applies to the residents of the Russian Federation, and on non-residents. The tax object is the income that the physically received, including entrepreneurs for a certain period. What kind of income should pay this tax? These include:

- The salary.

- Revenues received after selling property, rental properties.

- Various payouts for Stress Policy, Dividend.

- Income obtained by the saline for operations with securities.

- Pension.

- Social payments.

- Various rewards, premiums.

- Other types of income.

It is worth noting that tax residents should pay this tax from all revenues that are obtained not only in Russia, but also in other countries.

But if faces are not residents of the Russian Federation, the tax must be paid from those income that was obtained in Russia.

True, there are exceptions from everything - also here. There are income that do not belong to NDFL objects:

- The benefits received from the state are excluding temporary disability.

- Labor pension, compensation payments.

- Alimony for a child.

- Grants from organizations - True, their list should be approved by the Government of the Russian Federation.

- Received premium for achievements.

- Mature, which is paid at emergency (natural disasters, paying to those who have suffered from terrorist attacks, charity).

- Salary in the currency that state-owned employees receive - at the same time they should be aimed at paying the work of those who work abroad.

- Revenues received by farms during the first five years of their activities after registration.

- Obtained when implementing fungus, berries, etc. profit.

- Gifts, excluding real estate and cars. However, if a gift from a close relative (spouses, parents, children), any gift will not be taxed.

- Monetary prizes for sports events, contests.

- Help from non-commercial organizations to orphans or low-income families.

NDFL rates - Consider all options

As we have already said, the NDFL rate depends on whether the citizen is a resident of the Russian Federation. But its size depends on the type of income received. In the following tables, we will study more detail which tax rates should be applied in calculations.

Rate size for residents

Non-resident bet size

How to calculate ndfl from wages?

The law imposes on the organization and company all functions on the calculation of NDFL and payment to its budget. And the collection, as many think, does not go to the hands of an employee, and immediately listed in the tax. To calculate the size of the collection, you need to accrue an employee not only wages, but all incomes premium to which it claims, as NDFL will be paid with the full amount. It is also worth identifying if any income not taxed by the collection. And finally, determine the status of an employee, since the tax rate depends on it. For example, if we are talking about the tax resident, it is 13%, if about non-resident, then 30%.

The form for calculating the tax is as follows: all accrued earnings minus calculations, not taxable taxes, and multiplied by 13%.

For non-residents, the calculation scheme will be almost the same, but it is worth remembering - they have almost no benefits. Therefore, all the earnings are taxed in the amount of 30%. If we are talking about vacations, then the NDFL from these payments will also be accrued from the entire amount and will be made at the time of payment of funds.

And then many managers make a mistake, believing that tax deductions from vacation pays are carried out by analogy with payroll, that is, two payments. This is usually due to the fact that they do not take into account that vacation payments are not included in earnings - their calculation and accrual takes place on the last day before the employee leaves on vacation. But the salary must be accrued to a minimum twice a month, with which the confusion is connected. Thus, the leadership does not have any legal grounds for the payment of NDFL from vacation taxes twice a month - this can lead to a fine.

If the individual has a child under 18, he has the right to claim a tax deduction that is 1,400 rubles, while the employee's income should not exceed 350 thousand rubles. If earnings are higher, it automatically loses the right to receive deduction. If the physical is raising from demand and more children, when calculating the inclination, it will be deducted in the amount of 3 thousand rubles.

Examples for tax calculation - Consider 4 options

So that you understand better, how is Ndfl's calculation, let's consider a few simple examples.

Example 1. NDFL for wages without deductions

Citizen Ivanchuk earns 42 thousand rubles. To find out the size of NDFL, it is necessary, first of all, to determine the interest rate - it is 13%. Consequently, the calculation will be as follows - 42000 * 13% \u003d 5460 rubles, it is so much to list the budget monthly. On the hands of Ivanchuk will get 36540 rubles. (42000 - 5460).

Example 2. NDFL with the use of deductions for wages

Citizen Kozlova earns 56 thousand rubles per month, while she has two children under 18. To carry out the calculation, you first need to decide on the size of the deduction - for two children it will be 2800 rubles. (2 * 1400). Next, we take the amount received from the salary of Kozlova, receiving 53200 rubles. It is from this amount that we will consider deduction - 53200 * 13%, we get 6916 rubles. To compare benefits, it suffices to find NDFL for a gantry without deductions that will be 7280 rubles.

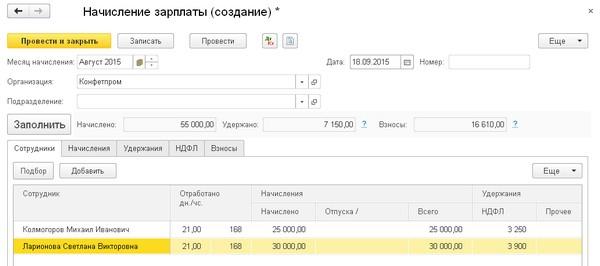

Example 3. NDFL from vacation

As we said, with holidays should also pay tax - the calculation is similar. For example, a Jverchuk citizen received holidays in the amount of 25 thousand rubles. You need to multiply this amount by 13%, as a result of which we obtain the amount of the tax, which will be 3250 rubles.

Example 4. Payments from dividends

Citizen Overchenko in 2014 received dividends in the amount of 30 thousand rubles. It is necessary to determine the interest rate, which is 13%. Accordingly, the amount of NDFL will be 3900 rubles (30000 * 13%).

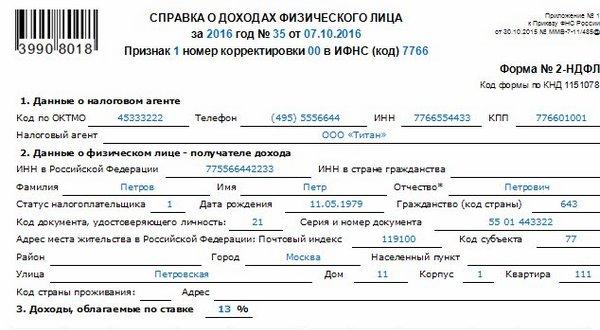

How to make a reference of 2 NDFL and 3 NDFL?

Until April 1, after the reporting period of the year, each company must submit an income document that accrued employees. It has a form of 2-ndfl. It is also used when issuing loans, tax deductions in the design of real estate, study, etc. At the same time, this certificate is drawn up not only to workers, but also for individuals who received payments from the company in the reporting year.

In the event that the employee received payments at different rates, the company is required to provide a tax appropriate number of references. This usually happens if the employee worked immediately in several branches of the company. However, there are cases where the registration of a certificate 2-NDFL is not required:

- If payments are not subject to taxation.

- When issuing material assistance (if their total amount for the year did not exceed 4 thousand rubles).

If a person won the winning casino or lottery, he must fill out and send a certificate.

How to fill it correctly? Carefully read our instructions:

- Fill the "Sign" field. Here we put "2", if you can't hold taxes from income. In all other cases, we put one block.

- Fill out the "Correction number" field.

- We indicate the IFTS (code), OCTMO.

- Fill out the field "Tax Agent" where you enjoy information about the company.

- The field "The Status of the Taxpayer", where we indicate whether it is a non-resident or resident.

- Fill out information about the document - employee passport, etc.

- Fill in a table with income.

If the declaration is filling the IP or individuals, which, in addition to their main wages, receive additional income, should be issued a 3-NDFL certificate. In addition, it should be fill in those who received income from the sale of an apartment or other real estate, who provided civil-legal contracts, in case of profit, but did not pay taxes from it. If the physically claims to receive a tax deduction, they should also fill out this document.

At the same time, with errors in the declaration or incorrect information, liability falls on taxpayers. In case of detection of errors, the tax payer must pay off debt, fine and penalty that can be charged. Such a declaration must be submitted no later than April 30, following the reporting period of the year.

The process of its filling is simple: fill out all the necessary graphs, make amounts and calculations, after which you send a document to the tax at the place of registration.

How is the penalty?

If you do not give a certificate on time and not pay NDFL, for each day the delay taxpayer will accrue a penalty. The amount will depend on the refinancing rate of the Central Bank of the Russian Federation - the higher it is, the more you have to pay.

The formula is as follows:

Penya \u003d tax amount * Number of days of delay * rate of the Central Bank of the Russian Federation: 100 * 1/300. The calculation will be simple, if for the entire period the rate of the Central Bank of the Russian Federation has not changed, in the opposite it will have to be calculated separately to achieve accurate calculations.

In addition, the current legislation provides other sanctions against taxpayers if they are:

- Submit to the declaration later than the set time. In this case, it will have to pay at least 5% of the tax amount for the entire month of delay. The main thing - the amount of the fine cannot be less than 100 rubles and no more than 30% of the total tax.

- If the declaration is submitted on time, but the flow procedure was broken, you need to pay a fine of 200 rubles.

- If the company has violated the rules for conducting primary accounting documents, then the penalty will be 25% of the amount of unpaid tax. At the same time, the size of the fine should not exceed 40 thousand rubles.

In contact with